Geopolitical, Liquidity Issues Dominate

The following is a partial summary of conclusions from our weekly fxempire.com analysts' meeting in which we share thoughts and conclusions about the weekly outlook for global equities, currencies, and commodity markets.

Here's a rundown of what's most likely to move markets in the coming week and beyond. These fall into 2 broad categories:

1. Geopolitical

· US and Asian allies vs. China: This is the more imminent threat, given China's recent assertion of control over the disputed islands' airspace, and the risky game of chicken between opposing air forces that played out last week. The risks of a miscalculation by either are obviously enormous, so we wouldn't be shocked if both sides get a bit quieter in the coming weeks. US Vice-President Biden will be visiting China and South Korea. Typically such visits are used to ease tensions, so any belligerent words would weigh on markets, which have thus far mostly ignored the posturing by both sides.

· US and Mideast allies vs. Iran and its "frenemies:" Although Iran has potential conflicts with both Russia and China, these nations tend to use support for Iran as leverage against the US. They did so successfully in the recent UN Security Council deal, undercutting US strength in the region, as we discussed in some depth, along with its short and long term market implications here.

We refer to Russia and China as Iran's "frenemies" because the extent of their alliance is limited. Both Russia and China host potentially restive Moslem populations, so it's hard to see either nation genuinely thrilled about a neighboring Iran that combines nuclear weapons with Messianic Islam.

In any case Biden's visit more likely than not means things cool a bit with China and Japan, and Iran has gotten what it wanted. Therefore this article will focus on the second category.

2. Liquidity Or Credit Risk Related

These include:

· Liquidity fears from the coming next round of the ongoing US budget and debt ceiling, which could theoretically bring another shutdown and rising bond rates on default fears. This is not likely to be a real concern until early 2014, but it's worth mentioning as it could come into focus if there is little other economic news towards year end.

· Events that influence speculation on the timing and pace of the Fed's QE taper plans: Taper sentiment in turn influences bond prices and thus interest rates in the US and abroad. If mishandled as in the past, expectations about "the taper" could send rates higher worldwide and endanger the shaky economic recoveries (?) in the EU and Japan as rising rates undo the easing measures of the ECB and BoJ. Other emerging market nations with significant foreign bond ownership would also see their rates rise and their economies pressured, as we saw last May. Both central banks are expected to take further easing measures even if the Fed can somehow avoid causing another interest rate spike.

This category includes the likely big market moving events this week. Indeed next week will arguably set the tone for the rest of the year and decide the fate of the current rally for the rest of 2013. The week is packed with events that could influence taper timing sentiment, as the Fed itself admits it is just following the data.

Important related data and events this week include:

1. Any preliminary data on post-Thanksgiving sales: These are hardly indicative of how the holiday season turns out, but if news is otherwise quiet and the news is positive markets could use it as an excuse to go higher, as markets tend to pay more attention to news that fits the prevailing technical picture, which is firmly bullish. Black Friday, Cyber-Monday and the like tend to produce high volume. The question is, after all of the sales and discounting can retailers actually improve earnings? Interpreting retail sales may not be a simple matter of comparing them to prior years:

a. This year's shopping season is one of the briefest in years, under 30 days

b. Retail stocks have underperformed the S&P 500 during the Thanksgiving to Christmas period for the past three years, per data from Bespoke Investment Group, which shows that from 2000 to 2012, the S&P 500 has averaged a gain of 1.7% during that time frame, with positive returns in 9 of the 13 years. Retail stocks, in contrast, have averaged a gain of only 0.8% in the same period, with positive returns during 6 of the 13 years (via Reuters here).

2. A Bernanke speech Monday: Would matter only if he says something that surprises markets about the pace and timing of the taper.

3. ISM manufacturing (and its jobs component) report Monday: Manufacturing has been improving, but it's the jobs component of the report that will be in focus as a leading indicator for Friday's official BLS monthly jobs report.

4. ISM non-manufacturing PMI report Wednesday: As with the manufacturing PMI, the jobs component of the report is the focus, but even more so because it covers far more jobs in the US, and is considered one of the more accurate leading indicators of the official report. New home sales figures are also out, but it will be overshadowed by the PMI report unless it packs a much bigger surprise.

5. US Preliminary GDP Thursday. We already had advanced Q3 GDP, but this could still be market moving if it helps clarify whether that big bullish surprise based on inventory buildup was due to a bullish restocking in anticipation of rising demand or bearish buildup of old goods due to weak consumer spending.

6. US monthly jobs reports Friday: The big ones are of course non-farms payrolls change and the unemployment rate (inaccurate but nonetheless gets attention). This is likely the most influential data of the week, if not the month. Its ultimate influence depends on whether it surprises to the upside or downside. Beware that the market's final reaction to the headline figures can be heavily influenced by revisions to prior months, as well as by surprises from the second tier reports that come out Friday, such as average hourly earnings, personal spending, and perhaps the core PCE price index. Economists expect about 185k new jobs on the NFP report, down a bit from last month's 204k. Given the significance of big round numbers, anything decisively over 200k raises the odds of an earlier taper. Preliminary UoM consumer sentiment also comes out Friday but should only be market moving if it provides a surprise.

3. Other Calendar Events

1. For the EU there's a raft of PMIs and an ECB rate statement. This could move market consensus on the pace and timing of the next ECB easing moves. Last month the ECB made a surprise rate cut, much to the displeasure of Germany and its ECB allies. The EURUSD continues to move higher even while most traders are short the pair.

2. For traders of the AUD or investors in Australian assets, it's a big week, with an RBA rate statement, building approvals, retails sales, GDP, and more.

3. China has its official manufacturing PMI report out Sunday, and the HSBC final manufacturing PMI out Monday ( it differs from the official report Sunday in that it focuses on smaller private firms instead of big state owned monopolies)

4. Other Tail Risk

We continue to watch for signs of progress on the EU bank stabilization plans for dealing with banks that fail next year's ECB stress tests. There is plenty of risk below the surface, as we discussed in some detail here. The next round of EU angst may well originate from struggles with these negotiations. If not, a possible new bailout deal for Portugal, and a first one for Slovenia could be the source of trouble for the EU.

5.Technical Picture

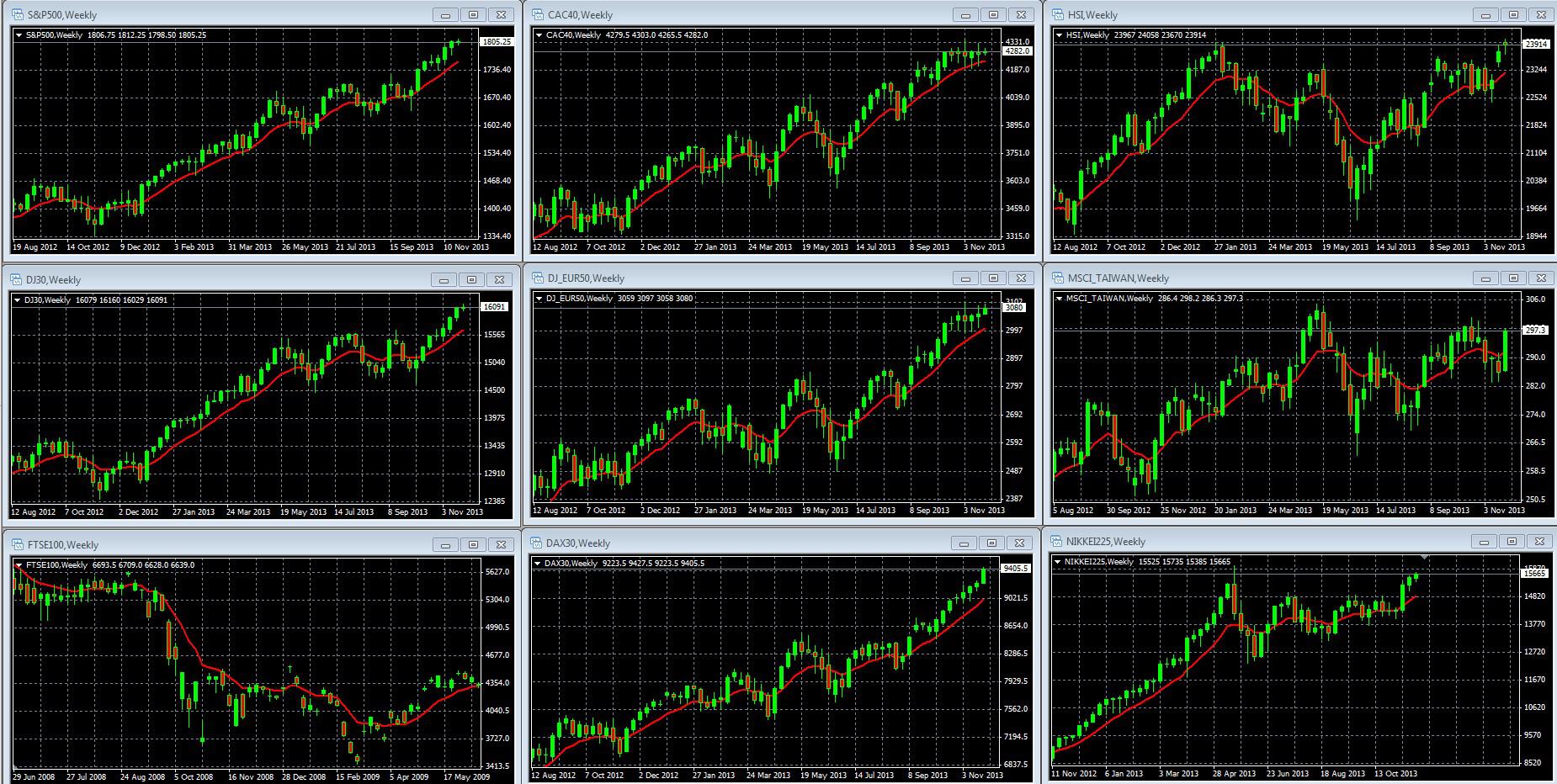

As the sample of leading global stock index weekly charts below show, the risk asset rally remains intact and firmly entrenched in multi-month uptrends.

(click to enlarge)

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day Ema: Left Column Top To Bottom: S&p 500, Dj 30, Ftse 100, Middle: Cac 40, Dj Eur 50, Dax 30, Right: Hang Seng, Msci Taiwan, Nikkei 225

Source: MetaQuotes Software Corp, thesensibleguidetoforex.com

01 NOV 30 20 07

For details on what's likely to sustain and threaten this rally see both:

· 2013 Outlook Year-End & Beyond: Summary, Conclusions, Must-Watch Developments

· The Latest Threat To The Risk Currency Rally

Implications

As long as these uptrends persist, we remain long risk assets and currencies, and avoid shorting them as a general rule. Markets will tend to heed bullish news more than bearish news.

A Reminder

We noted above how both the ECB and BoJ are expected to ease further and thus weaken the EUR and JPY. Australia has not ruled out further easing. The Federal Reserve is expected to taper its QE, but at the same time do all it can to keep rates down (and thus suppress USD demand).

It's a dangerous time for anyone to have all their wealth tied to the health of only one currency. See here for full guide to safer, simpler ways to diversify your portfolio's currency exposure, even if you never trade currencies. Inflation isn't a threat at this time because most economies are still recovering, the world is awash in excess capacity and labor, and so wages and interest rates remain low. Now is the time to prepare for inflation threats that will come with a recovery.

Disclosure/disclaimer: No positions. The above is for informational purposes only. All trade decisions are solely the responsibility of the reader.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1870201-the-coming-weeks-top-market-movers-the-things-you-must-monitor?source=feed

Aucun commentaire:

Enregistrer un commentaire