Technology sector stocks have been investor favorites in 2013, pushing the tech-heavy Nasdaq Composite Index to its highest level since 1999 and drawing comparisons to the "dot com" bubble which burst soon thereafter. Will we see a redux of the tech bust in 2014? John P. Scandalios, vice president and portfolio manager, Franklin Equity Group®, doesn't think so. Investor fever for anything "dot com" in the late 1990s was built more on promise than actual results. Today, he says, generally, tech companies are not just trading on hope; his team's research finds they are delivering results in the form of revenue and earnings growth. Scandalios notes that certain tech companies today are a powerful force of change and innovation, rather than just bubble bait. That said, he emphasizes the importance of being picky about stock selection in the sector in order to find quality names that he believes have the potential to stand the test of time.![]() ___________________________________________________________

___________________________________________________________

John P. Scandalios

Vice President and Portfolio Manager

Franklin Equity Group®

The technology sector is currently experiencing a series of secular waves of change and innovation. So much so, in fact, that in the 17 years I have been at Franklin Templeton, I believe there's never been a more interesting time to consider investing in the sector.

As we approach the New Year, the market outlook appears to us to be broadly positive. I feel optimistic about the stability of the underlying global economy, while domestic US economic data appear to be gradually improving, although it is still far from being robust.

In this context, and while interest rates remain low, we should continue to see a decent environment for well-positioned technology companies to generate both revenue and earnings growth. In particular, overall revenue and earnings estimates for technology companies next year seem reasonable and achievable, which should bode well for technology stocks, especially given that valuations in many stocks in the sector still look attractive to us at this time.

There is uncertainty among some investors and commentators over the possibility of a bubble forming in the tech sector. Having been an analyst and portfolio manager during prior bubbles, I believe some of the market fundamentals and investor behavior seem to have matured since 1999.

As is often the case, there are areas and individual stocks within the sector where valuations and growth expectations are looking increasingly overvalued, and we are diligently reviewing our estimates and expectations to make appropriate decisions on those specific stocks or pockets of stocks. But when you deconstruct the S&P 500 by sector, the information technology sub-segment is still the least expensive on a forward Price/Earnings (P/E) basis, based on 2014 earnings estimates1. And, more technology companies are returning meaningful amounts of cash in the form of dividends to shareholders. To me, this reflects not only their strong business models, but also a more shareholder-friendly mindset among management and boards of directors.

We believe the main market risks in early 2014 are linked primarily to the US government's fiscal decisions and its dysfunctional behavior, which could thwart the gradual economic recovery that's taking place both in the US and internationally. After a government shutdown in October 2013, we now hear rumblings related to the National Security Agency and privacy issues. These external factors may add a level of uncertainty that is rarely favorable for equities.

Tech Trends Worth Watching: Security, Medical Technology and More

There are many reasons to be positive about the technology sector right now. Innovation in the technology sector is alive and well, and is manifesting itself across many industries and companies. One of the major secular trends is the adoption of SAS, or software-as-a-service, within the software industry. Another is the continued proliferation of e-commerce, which is in the midst of transitioning to a more mobile, local and personal functionality. A third is the adoption of both public and private cloud IT services, which is having a dramatic impact on many companies. Now that we have a greater number of mobile workers using connected mobile devices or the cloud, there has also been a growing number of cyber attacks, causing a dramatic increase in demand for network security. Wireless carriers around the globe are starting to deploy LTE or 4G functionality for the communication of high-speed data, which bodes well for several mobile phone and wireless infrastructure-related companies. And, finally, another powerful secular trend is that NAND flash solid state drives are taking meaningful share on both the client side and enterprise side from hard disk drives.

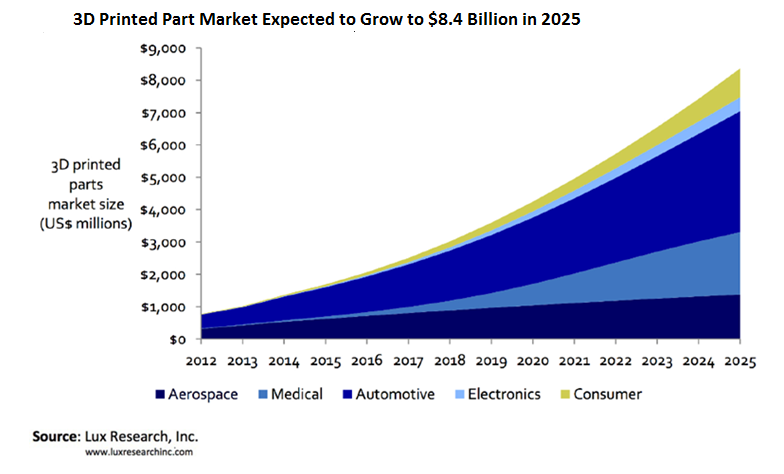

In the less traditional, emerging technology sectors, we are seeing some interesting trends, including gene sequencing and constant glucose monitors in the medical technology field, as well as areas such as 3-D printing and LED light bulbs. There's also a big discussion around the "Internet of Things" which refers to the uniquely identifiable objects and their virtual representations in an Internet-like structure. Simply, this means data can be automatically transferred over a network without human-to-human interaction. Already, doctors are using pill-shaped micro-cameras swallowed by patients to take thousands of images from inside the human digestive tract to search for possible sources of illness.

(click to enlarge)

The Importance of Stock Picking and Risk Management

Even in a supportive environment, stock selection is extremely important, as is risk management. Our investment strategy is a growth approach that employs intensive, bottom-up, fundamental research to identify companies we believe possess quality management, robust growth prospects, strong market positioning, high or rising profit margins and good return on capital investment.

Our stock selection process, or funnel, starts once our analysts have identified what we deem to be powerful secular themes within each technology industry. We then identify which company or companies we believe are best positioned to drive or benefit from that secular theme. We patiently wait for the inevitable market volatility, which provides us with the opportunity to purchase shares opportunistically at more attractive valuations than other investors who may be more short-term focused.

Our risk management process is based on the scrupulous research that our analysts perform before even recommending a specific stock, followed by a second-stage analysis focusing on growth, quality and valuation. This presents quite a high hurdle, which we think helps us avoid many pitfalls. It also means that we have a clear understanding of why we own each stock and what milestones we are looking for from that company. We are quick to react if we see a company's fortunes deviating meaningfully from our roadmap. We also believe that the quality of our analysts, most of whom have a long tenure at Franklin Templeton and experience in the sector, offers us an advantage.

We believe select, well-positioned technology companies remain fundamentally sound with attractive secular growth prospects. At the same time, we think M&A activity within the technology sector remains robust. All of these conditions contribute to our positive long-term outlook for the sector.

What are the Risks?

All investments involve risk, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

The technology sector has historically been volatile due to the rapid pace of product change and development within the sector. Technology companies can be small and/or relatively new and unseasoned. Smaller companies can be particularly sensitive to changes in economic conditions and have less certain growth prospects than larger, more established companies.

1. Source: Bloomberg LP, as of December 2013

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire