There's been a ton of debate over chip giant Intel (INTC) recently, and I know that I've been very vocal in regards to this name. While Intel is starting to make a heavy push into tablets, the company's late arrival to the party (which it has admitted multiple times) has pushed back the growth story a couple of years. Intel recently announced it would have flat revenues in 2014, a very disappointing announcement. The Intel bulls will tell you that no growth compared to expectations for 2.1% growth (when Intel guided for 2014) isn't a very big difference, and that it has more to do with analysts being wrong. Well, these Intel bulls are missing the big picture, which is a company that continues to disappoint. Today, I'm going to explain why flat revenues in 2014 are a problem, how one issue can snowball into many.

Intel's plans for 2014:

By now, most investors know Intel's plans for 2014, and I covered them a bit in my latest Intel article. As the PC industry continues to decline and tablets surge, Intel is looking to break into the tablet space. Intel has admitted that it was late to the party, and the company is planning on quadrupling tablet CPU shipments to 40 million in 2014. How will the company do that? Well, it will require a potential $1 billion in tablet CPU marketing subsidies.

The current Intel plan is one that analysts are divided over. I covered a few analyst comments in my latest article, but RBC downgraded Intel this past week and reduced its price target by a dollar to $26. A couple of the analyst's statements are below.

"Doug Freedman - noted that his firm's thesis has changed as we were looking for more ROI focus and better ultra mobile execution than was displayed at the recent analyst day. The only offset is low expectations with visible headwinds allowing guided and Street earnings forecast to be priced in.

"In the past, Intel has entered new markets with subsidies that offset less attractive solutions and, once again, that is the plan for the tablet market. Our issue is that the ROI has not been supported by the opportunity."

"Intel does not have a large analog IP library on leading-edge process nodes. This is the major hurdle to foundry revenues and success in ultra mobile markets. PC refresh issues remain unanswered: Win8 appears to be having a major impact on the consumer PC market and no actions (other than OS free hardware) are targeted at solving consumer PC usability."

Intel needs to get into the tablet space quickly, and this will certainly be a way to do it. But will the costs outweigh the benefits? That remains to be seen. One thing is clear. Intel's 2014 guidance was disappointing, which makes us believe 2014 will be the third straight disappointing year for the chip giant. Revenues won't be the only problem, and I'll explain how this problem snowballs in the next few sections.

First, the income statement:

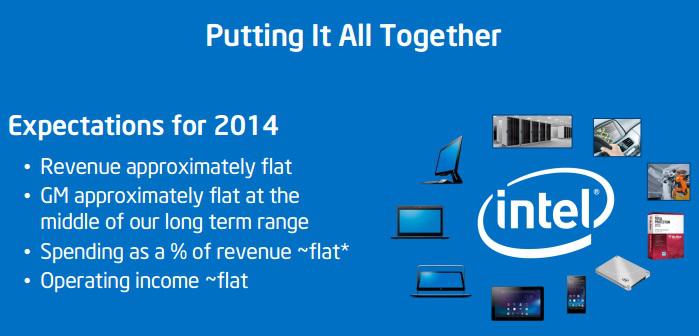

I was told by an Intel bull, one who writes for this site, that Intel coming in with guidance for flat revenues is basically meaningless when expectations called for 2.1% growth, as that difference is not big and shows that analysts are just off. Well, I beg to differ. First, that difference is about $1.1 billion in revenues. But it just isn't revenues that is the issue. Here's Intel's slide from the Investor Day Presentation in regards to the 2014 forecast.

(click to enlarge)

Revenues are only the first line in the income statement, but a more than $1 billion miss from expectations will have severe repercussions as we go down the income statement. You can see how Intel guided for operating income to be roughly flat as well. Now, there will be other items further down the income statement, but since we can't predict items like "other income" and tax rates, we can only assume that net income will be roughly flat as well.

So what's the big deal here? Well, let's revisit my Intel bull/bear case for 2014 from a few months ago. Although I had a wider revenue spread between my bull and bear case ($1.6 billion), the spread I had in net income was roughly $2 billion. My bear case did assume a higher revenue rate, but also some added expenses. While Intel's expenses may not be as much as I thought, revenues probably won't be as high either. The key takeaway here is that Intel's net income could be $2 billion less than hoped, and that is a big deal.

Current estimates call for flat earnings per share in 2014, but that could easily mean a further decline in net income, offset by a lower share count from the buyback. Intel's 2014 earnings estimates have come down by nearly a dime in the past three months, and three pennies since Intel gave 2014 guidance. Don't forget, there are still a number of analysts who still have optimistic forecasts. The high estimate on the street for 2014 assumes roughly 5% revenue growth for Intel. I doubt that will happen, so it is probable that more estimate cuts are coming on both a revenue and earnings per share front.

Second, the cash flow statement:

After the income statement, net income flows to the cash flow statement. Net income is the first line in the operating cash flow statement. Now, not all of that net income hit will be felt if some of it is due to items like depreciation and share-based compensation. Those are add-backs that help cash flow.

In the first 9 months of 2013, Intel's cash generated from operating activities actually rose by $1.88 billion, despite a $1.54 billion drop in net income, as seen in the 10-Q filing. There were more than $3.4 billion in post-net income adjustments, helping improve cash flow. Now, some of these items will eventually reverse, which will pressure cash flow. For instance, inventories swung from a negative $1.2 billion (buying inventories, less cash flow) to a positive $200 million (selling inventories, more cash flow). When Intel replenishes its inventories, cash flow will be pressured. Other working capital changes helped with another billion plus in operating cash flow.

So in 2014, while net income may be flat, some of these other items may reverse, and that could easily pressure operating cash flow. The next item to consider is capital spending, or capital expenditures. Intel guided to $10.8 billion in capex for 2013 and $11 billion for 2014. So if operating cash flow stays the same, free cash flow could be down slightly thanks to more capital expenditures.

The final item to consider in terms of cash flow is domestic versus international cash. Intel will generate a decent amount of cash, but like most large cap technology names, not all of it is generated inside the United States. Only cash inside the US can be used for dividends and buybacks. Other names like Apple (AAPL) and Microsoft (MSFT) have sizable cash positions outside the US. To be used for dividends and buybacks, a company must either repatriate these funds (and pay taxes) or borrow against these funds (and pay interest). I covered this issue in detail in my dividend raise reduction article, stating that Intel has about $10 billion of its $19 billion cash pile available for use in the US.

Third, capital returns:

Less cash available means less capital returns for shareholders. As an investor, you want more buybacks and more dividends, right? I would certainly hope so. I mentioned in my article above that I don't expect as much of a dividend raise anymore. That assumes of course that Intel actually raises the dividend this month or in 2014, and that may not happen now.

Intel's 22.5 cent quarterly dividend ($0.90 per year) yields 3.78% as of Friday's close. But if Intel's results had been better the past couple of years, maybe the dividend would have been at 25 cents per quarter ($1.00 per year) by now. Wouldn't a 4.19% yield, roughly 40 basis points more, make Intel a lot more attractive investment? Also, let's not argue the fact of Intel getting back to a 4.00% yield because of share price declines. Sure, at $22.50, Intel will have a 4.00% annual yield, but as a current investor, would you want Intel's stock to drop another $1.34, or 5.62%?

Intel also has slowed down the buyback dramatically from $4.09 billion in the first nine months of 2012 to just $1.9 billion in the first nine months of this year. Intel was using a bit of debt in past years to fund the buyback, and the company really hasn't added too much more since. Will the company take out debt now to buy back stock? I've argued that with expectations low, this could be the perfect time to do it. However, if Intel cuts its forecast again, the stock could go even lower, meaning the company should wait to buy back shares.

A less compelling investment?

So after all the numbers are calculated, it just isn't depressed revenues and earnings as cash flow and capital returns are lower. Does that make Intel a less compelling investment? It sure does. Here's how Intel's fiscal 2014 stacks up against some other large cap tech names, including Google (GOOG) and Cisco Systems (CSCO).

*EPS Growth and P/E numbers are non-GAAP.

As everyone knows by now, Intel's growth story will be in fourth place of these five names. Intel would be last if it wasn't for Cisco's warning from a few weeks ago. Just this past week, Intel's valuation passed below that of Apple. For the longest time, Apple traded at a discount to Intel, despite Apple having a lot more going for it. Remember, the current analyst average estimate for Intel's 2014 revenues still implies 1.2% growth, a bit above the flat revenue figure Intel guided to. In my last article, I stated a fair value for Intel was 12 times expected 2014 earnings. With estimates at $1.89, that gives a fair value of $22.68, almost 5% lower than where we are now.

Final thoughts:

While the Intel bulls might tell you that flat revenues are no big deal, it's a bigger problem than most realize. For a quick recap, here is how this all breaks down:

- Flat (lower than expected) revenues lead to flat operating income and presumably flat (lower than expected) net income.

- Lower than expected net income leads to lower than expected operating cash flow, which could be pressured by reverses in working capital items.

- Lower than expected operating cash flow combined with higher capital expenditures leads to lower free cash flow.

- Lower free cash flow, especially cash flow in the US, means lower dividends and buybacks.

- Lower dividends and buybacks makes Intel a less compelling investment going forward.

Like a snowball building as it goes down a slope, this is not a small problem. Intel investors need to readjust their expectations, something analysts have started to do. I do believe Intel goes lower from here, at which point another evaluation is needed. But until Intel gets a bit lower, I think this remains a short opportunity.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1870191-intel-how-one-problem-snowballs-into-many?source=feed

Aucun commentaire:

Enregistrer un commentaire