Another year is about to become history, and we're no better off than we were twelve months ago, apart from stock market records and promises that monetary maneuvering and band-aids will cure the wounds. I continue to read plenty of opinions on how deflation is a crushing force on debtor nations, and while that is true, the real destructive burden of debt is felt by creditors, because debtors can walk away from their obligations and creditors see their savings and investments disappear into a bottomless pit. If it wasn't so, central banks wouldn't be so focused on containing the disease.

The American landscape is still dominated by the expanding conversation about the housing recovery, and while at times the data appears sweet on the surface, the bitterness that will follow will bring us back to square one. Beyond the supporting hand that the investment community has lent to the housing industry -- only because they've discovered REO to Rental -- the influence has run its course. In addition, new developments paint a different future, as highlighted by the article "A new wave of U.S. mortgage trouble threatens."

U.S. borrowers are increasingly missing payments on home equity lines of credit they took out during the housing bubble, a trend that could deal another blow to the country's biggest banks. The loans are a problem now because an increasing number are hitting their 10-year anniversary, at which point borrowers usually must start paying down the principal on the loans as well as the interest they had been paying all along.

Home equity loans are second mortgages, and default will add to the foreclosure pile. "Déjà vu all over again," and a reminder that the core economic weakness never left. Along come central banks and their magic wands, and like single women at a wedding, frantically fighting to catch the bouquet, the Fed continues to wave its hands uncontrollably, hoping to catch a break and the credit that will come with it. Speeches and interviews that deliver conflicting assessments are dispensed on a daily basis, adding to market volatility when in fact the institution's key objective is to stabilize prices. Go figure! Truth is that monetary policy may temporarily patch, but it cannot fix, otherwise we would be on our way to Wonderland, and we're not.

An article by Dr. John P. Hussman brings forth two important points, and despite its density at times, the piece is a good read, especially for those seeking an added macro perspective on the stock market. The first point is about how the "Financial Accounting Standards Board abandoned FAS 157 'mark-to-market' accounting" in 2009, a rule that "requires companies to set values on most securities every quarter based on market prices."

Wells Fargo & Co. and other companies argue the rule doesn't make sense when trading has dried up because it forces banks to write down assets to fire-sale prices.

Well, don't banks require that borrowers "mark-to-market" their assets before they lend a single penny? In other words, that 1950s tin can that I bought for $100 at an auction and cannot sell because there's no market for it, is, in fact, worthless.

In case anyone has hopes that revolve around the installation of a new Fed chief, Hussman's second point is made by reviving a speech by Janet Yellen.

My strong disagreement should not be confused with disrespect, and none is intended, but wasn't it Janet Yellen who in October 2005, at the height of the housing bubble, delivered a speech effectively proposing that monetary policy could mitigate any negative economic consequences of a housing collapse, and arguing that the Fed had no role in preventing further housing distortions? Given the lack of concern with the present elevation of the equity markets, these remarks from 2005 have a rather ominous ring in hindsight.

Exactly! What we have is monetary policy driven by the self-indulging notion that the Fed is far more powerful and influential than it actually is, building a false sense of control and safety, as proven time and again.

The European Central Bank faces the emergence of a deflationary threat that never left, which is now fueling talk of negative rates. But as the ongoing "Euro zone loans contraction increases pressure on ECB," some continue to view pretty pink skies where darker clouds dominate and tornadoes are forming.

France's finance minister Pierre Moscovici has said his country's economy "is getting better". The eurozone's second biggest economy has been hit by 60 billion euros in additional taxes since 2011 and an 11% unemployment rate. Public debt is expected to top 95% of GDP next year but Mr. Moscovici told economics correspondent Andrew Walker, "This country is changing... we are reducing our deficits, we are reforming our pension system."

To fully comprehend the European mindset, one needs only to point to the fact that "France's parliament has passed a law aimed squarely at US online retailer Amazon (AMZN) that will prevent internet booksellers from offering free delivery to customers, in a bid to protect the country's struggling traditional bookshops." Disrupting disruptive technologies to protect stodgy business models is their idea of a free market and prosperity!

In general, ECB members are no different than their Fed counterparts, and excel at delivering rosy scenarios, and without boring you with a limitless parade of quotes, the following serves as a prime example, while the "official" unemployment rate is 12.1%.

There is no risk of deflation visible in the euro zone economy but its recovery is fragile with inflation low and credit subdued, ECB Executive Board member Peter Praet said on Tuesday.

But let's recall the first part of this conversation, where deflation will play havoc with servicing debt, and debt in the eurozone continues to expand despite austerity and reform. Spain's debt, as an example, "has more than doubled since 2008," and the IMF envisions that "the debt-to-GDP ratio will top 100 percent in 2015." It's a vicious cycle that can only be broken through default, although everyone wants a fix without paying the price for past mistakes. In case one hasn't noticed, "frustration grows over Greece's failure to complete the reforms it has promised in return for aid," as if the conversation never changed. At times we read about Greece's primary budget surpluses, but here's a simple example: You earn $50,000, spend $48,000 and have a primary surplus of $2,000. Interest on your debt is $4,000, and suddenly the primary surplus is meaningless.

With the last rate cut, the ECB admits that Europe is well entrenched into the weeds and will not get out anytime soon. That's the disruptive message the market received and then ignored, especially as ECB rates approach zero and QE, Fed style, is illegal from a treaty perspective. Then again, when did treaties, constitutions or any silly piece of paper stopped politicians and bureaucrats from instituting policy, especially when their skins are on the line?

On the Japanese side, they're as confused as everybody else, as highlighted by "Bank of Japan Foiled by 'Scroogenomics'."

Takehiro Sato wanted to add a line to the final statement declaring that consumer prices "are somewhat tilted to the downside" rather than that risks were "being largely balanced." Takahide Kiuchi proposed making the BOJ's 2 percent target more flexible. Sayuri Shirai wanted to highlight upside and downside risks to economic activity and price changes, which seems like code for what happens with inflation is, really, anyone's guess.

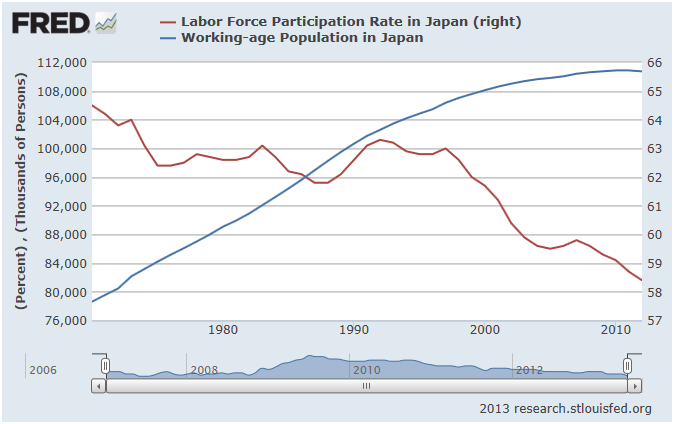

Sure, inflation in Japan improved a bit, but it's all about energy, something Japan does not have much of. Unemployment is an enviable 4%, but as the chart below demonstrates, that shrinking labor force participation rate is a thorn on everybody's side. Is America's labor force participation rate's trajectory eerily similar to Japan's own? Yes, it is.

Since QE is now the global economic law of the land, the Bank of Japan appears ready to take the process a step further and "beyond its $70 billion-a-month bond-buying operation," mirroring the quest for the "wealth effect" championed by the Fed.

In Japan, the central bank's options include major purchases of stock market-linked funds or other assets riskier than Japanese government bonds, according to officials briefed on the process.

While central banks play musical chairs with themselves, everyone understands by now that the Fed's mandate established by Congress is to seek "maximum employment, stable prices, and moderate long-term interest rates." But as if somebody understands the Fed's limitations -- just because it's a mandate doesn't mean it can be done -- Charles Plosser, president of the Federal Reserve Bank of Philadelphia, offered the following suggestions, what I see as a preemptive defense strategy.

- First, limit the Fed's monetary policy goals to a narrow mandate in which price stability is the sole, or at least the primary, objective;

- Second, limit the types of assets that the Fed can hold on its balance sheet to Treasury securities;

- Third, limit the Fed's discretion in monetary policymaking by requiring a systematic, rule-like approach;

- And fourth, limit the boundaries of its lender-of-last-resort credit extension.

Mr. Plosser delivered another speech over 18 months ago that covered a broader topic as it applies to central banks on a global scale, while highlighting solvency as a pre-condition for central bank assistance.

In some circles, it has become fashionable to invoke "lender of last resort" arguments as a reason for central banks to engage in fiscal actions. This is a strained argument at best. The basic role of a lender of last resort is to provide liquidity to financial institutions that are solvent but facing temporary liquidity problems. Yet recently, some have used the concept to argue that the central bank should be the lender of last resort to governments. This is a perversion of one of central banking's core concepts. It is a fig leaf to conceal the process of monetizing the sovereign debt of those countries that are insolvent due to their inability to manage their fiscal affairs. Monetary policy should not be used to solve a fiscal crisis.

Plosser's statement is an indictment of the monetary establishment as we know it, and goes as far as effectively calling for the withdrawal of support for selective economic segments by the Fed, such as housing. "Central banks and monetary policy are not and cannot be real solutions to the unsustainable fiscal paths many countries currently face."

What central banks have accomplished is an unrelenting interference with markets that will have uncalculated consequences, one of which is the elevation of one's economic hopes that will be met by devastating disappointment, which would be prevented if markets were allowed to adjust on their own. To a large degree, centrals banks are like third rate magicians that can't pull a flea out of a hat, much less a rabbit, and their incessant flyovers are reminiscent of Hitchcock's "The Birds." Once in a while I like to revisit my splendid literacy works (in my mind, that is) and in November of 2010 I included the following in the last chapter of my book:

The three fundamental requirements for the economic engine to propel us forward are simple, unmistakable, and do not require a lot of debate - be it academic, political, economic, or otherwise - and they exist in an unbroken order. We will call the requirements the "C Chain," whether the words "consumer" or "citizen" are used - and no, China is not a link.

1. Citizen Confidence.

2. Citizen Credit.

3. Citizen Consumption.

And the last "C" refers to the group above as a unit, which is termed the Core of the Global Economic Engine and starts right here in the U.S.A. All else is just noise!"Is this a new, revolutionary, economic model?" Hardly! And I call it common sense, which is not an abundant commodity, especially among bureaucrats and the academia. The Federal Reserve, and politicians and policy makers - they're one and the same - of all colors and stripes must understand that they cannot break the sequence, by starting in the middle of the chain and addressing item number two, when the first and most important factor, is not budging!

Confidence activates credit, and credit triggers consumption. How elastic is confidence? Not much. It's either there or it's not! That's Economics in three words. Zero interest rates and quantitative easing will fail simply because the consumer doesn't trust the economic environment, and no one can be forced into borrowing and consuming against their will.

Certainly we have a credit problem as pointed out in my previous post "1959: The Year Economics Changed And Nobody Noticed," which complicates the process.

From a market perspective, don't be too quick on taking short positions, while Europe will become the catalyst once again sometime next year. On the short subject, the Credit Suisse Hedge Fund Index shows that the "Dedicated Short Bias" strategy was down 23.21% for the year as of September, and I never understood why anyone would embrace shorting stocks as a full time strategy, which is no different than slapping one's own face 50 times every morning because it feels right. In closing, I want to point out that there's a chasm between being a pessimist and a realist, and I am not the former.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1876841-note-to-central-banks-your-theatrics-are-exhausting?source=feed

Aucun commentaire:

Enregistrer un commentaire