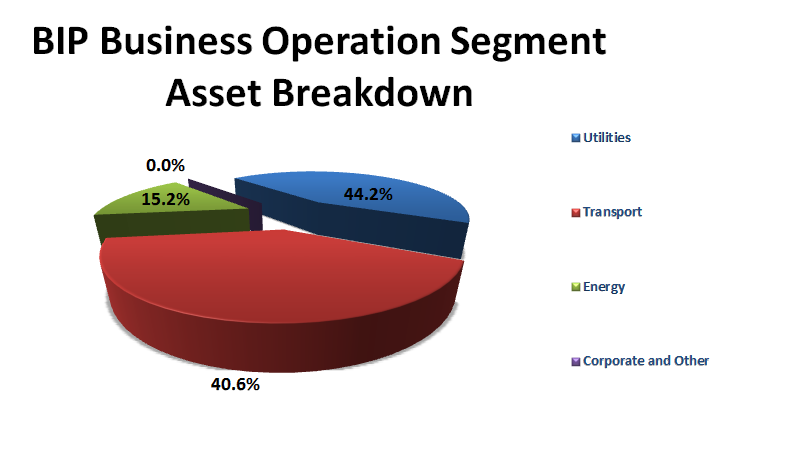

This investor normally frowns on companies issuing secondary offerings in order to finance "growth". However, this investor views Brookfield Asset Management's (BAM) infrastructure asset management affiliate Brookfield Infrastructure Partners (BIP) as a diversification away from traditional stocks and bonds and being able to utilize a high-quality asset manager for investing in unique, hard-to-duplicate infrastructure assets. BIP grows through prudently acquiring high-quality infrastructure assets much as a private equity firm grows through the acquisition of desirable investment targets. BIP's Utilities segment accounts for 44.2% of its assets, its Transport segment has 40.6% and its Energy segment checks in with 15.2% of its assets.

Source: BIP's Q3 2013 Earnings Supplement

BIP's Q4 2012 FFOs were $.65/unit and this solidly exceeded the $.58/unit that the average analyst expected as well as the $.54/unit achieved in Q4 2011. BIP's Q1 2013 FFOs/unit was $.80, which met consensus analyst expectations and increased from $.58 in Q1 2012. BIP's Q2 2013 FFOs/unit was $.88, which beat consensus analyst expectations by $.07 and increased from $.60 in Q2 2012. BIP's Q3 2013 FFOs/unit was $.80, which beat consensus analyst expectations by $.04 and increased from $.58 in Q3 2012. The prime drivers of this growth were due to acquisitions in its Utilities business (a regulated UK utility distribution business and its Chilean electricity transmission system) and acquisitions of Brazilian and Chilean toll roads in its Transport business.

Source: FactSet Marquee

For the 14th time in the last 15 quarters, BIP's Fund Flows from Operations exceeded consensus estimates published by sell-side analysts. BIP's total FFOs increased by 48% in Q3 2013 versus Q3 2012 and reached $167M due primarily to the additional capital employed by BIP pursuant to its acquisitions.

Source: BIP's Q3 2013 Earnings Supplement

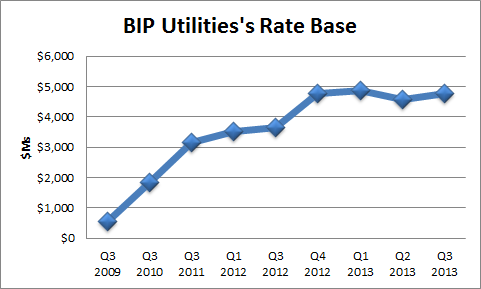

BIP Utilities saw a 21.25% increase in its Q3 2013 FFOs versus prior year levels. The increase in FFO was primarily attributable to the Q4 2012 acquisition of Inexus. BIP Utilities merged Inexus into its UK regulated distribution business. A secondary cause of BIP Utilities' FFO growth was due to an increased ownership stake in its Chilean electricity transmission system. Excluding these acquisitions and investments, the division's FFOs increased due to inflation indexation and additions to rate base of existing operations. BIP's maintenance capital expenditures in Q3 2013 were $6M and equaled the prior year's comparable quarter. For the first nine months of 2013, its maintenance capital expenditures increased by $2M in versus YTD 2012. BIP Utilities' AFFO yield was 15% on average invested capital, which slightly below Q3 2012 levels. BIP Utilities grew its revenue by 3.8% year-over-year in Q3 2013 and operating costs actually decreased by 15%. BIP Utilities three business units are as follows:

- Regulated Coal Export Terminal: BIP Utilities owns one of the world's largest coal exports terminals in Australia, with 85M TPA of capacity

- Electricity transmission: BIP Utilities owns approximately 9,900 km of transmission lines in North and South America

- Regulated distribution: BIP Utilities has almost 2.5M electricity and natural gas connections primarily in the United Kingdom and Australasia

Source: BIP's Financial Supplement and our estimates

BIP reorganized its BIP Transport and Energy segment into BIP Transport and BIP Energy. BIP Transport saw a 105% increase in its FFO's for Q3 versus the prior year's period due to the commissioning of its Australian railroad's expansion program and contribution from South American toll roads acquired in Q4 2012. BIP's Transport operations generated a 49% revenue increase and the division saw positive operating leverage as its operating costs increased by 17.4%. Non-Cash expenses for BIP Transport were $42M for Depreciation and Amortization (up 56% versus last year) while deferred taxes and charges were $17M and were attributable to the result of recognition of deferred tax assets. BIP Transport is comprised of these three operations:

- Railroad: BIP Transport is the sole provider of rail service in Southwestern Western Australia with approximately 5,100 kilometers of track

- Ports: BIP Transport has 28 terminals in the United Kingdom and across Europe

- Toll Roads: BIP Transport operates ~3,200 kilometers of motorways in Brazil and Chile

BIP Transport invested $495M in its Brazilian toll road subsidiary Arteris S.A. and this would increase its ownership stake in Arteris to 31%. In BIP Transport's first year of ownership, Arteris' performance has exceeded management's expectations, with toll revenues increasing by over 10% compared with the prior year. In addition, Arteris has invested over R$500 million of growth capital to widen its roads, which is expected to increase throughput going forward. BIP's management sees this as an attractive opportunity to invest more capital in assets that it knows well, with long-term, risk-adjusted returns within its target range of 12-15%.

BIP Energy's FFOs were flat year-over-year ($14M in Q3 2013 and Q3 2012) despite a challenging natural gas market that continues to negatively impact results at its North American gas transmission business. This investor can see that BIP Energy is one of the few companies that is not benefiting from hydraulic fracturing serving as the supply and demand game changer in the natural gas industry. BIP Energy's Adjusted EBITDA was $31M in Q3 2013 and $30M in Q3 2012 due to the aforementioned natural gas market headwinds. BIP Energy's maintenance capital expenditures decreased from $14M in Q3 2012 to $11M in Q3 2013 due to the timing of maintenance projects. This investor was not surprised that BIP Energy's AFFO Yield of 1% trailed BIP's other divisions. BIP Energy's operations comprise the following units:

- Energy Transmission, Distribution: BIP Energy has 15,500 kilometers of transmission pipelines, over 50,000 gas distribution customers and 300 billion cubic feet of natural gas storage capacity in the U.S. and Canada

- District Energy: BIP Energy operates a 522 Megawatt thermal district heating system and 82,300 ton deep lake water cooling system

BIP's Corporate and Administrative segment's net pre-tax expenses increased by $5M (24%) in the quarter as increased management fees paid to Brookfield Asset Management offset reduced financing costs. BIP also reached an agreement to sell its 42% interest in its New Zealand regulated distribution business, initially acquired in 2009 as part of the recapitalization of Babcock & Brown Infrastructure. The Partnership expects to receive proceeds of approximately $410M from this sale by the end of 2013, following the approval of the New Zealand Overseas Investment Office. This comes on the heels of BIP harvesting $470M from the sale of its timber operations

Source: BIP's Investor Relations

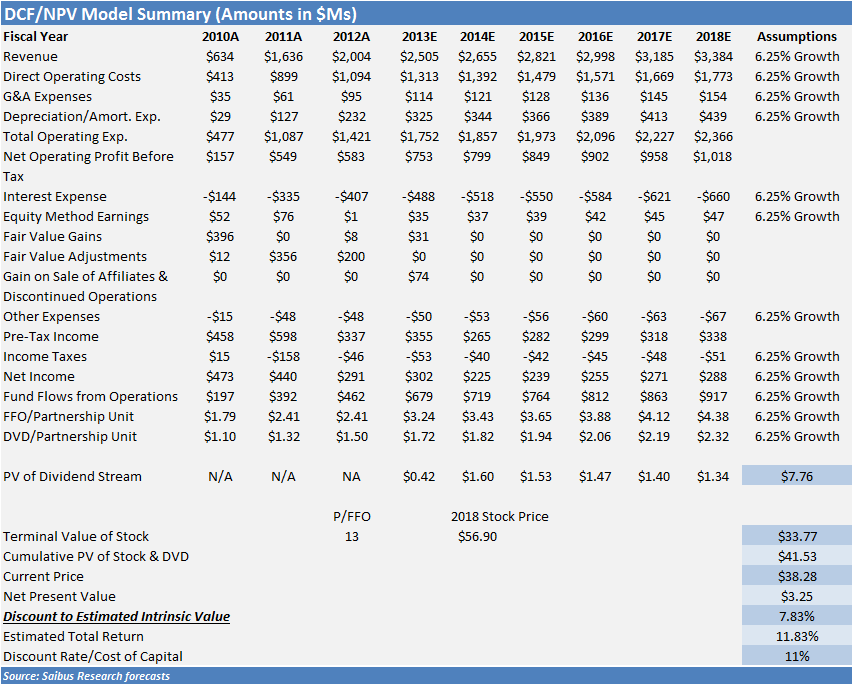

In conclusion, this investor still likes what he sees from Brookfield. BIP's unit price has pulled back 8% since its November highs and investors looking for high yields and non-equity correlation should consider BIP's portfolio of unique, hard-to-replicate assets. BIP has provided unit-holders with strong returns from capital appreciation and partnership unit distributions since it went public in 2008. While BIP's unit price is within ~8% of its fair intrinsic value and investors should not expect the relative returns to be as breathtaking over the next 5 years as the previous 6 years, this investor expects that this will be a great alternative to the S&P 500 and traditional utilities as represented by the XLU.

Source: FactSet Marquee and Our Estimates

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1876831-brookfield-offers-high-dividend-yield-and-steady-growth-from-infrastructure-assets-neutral?source=feed

Aucun commentaire:

Enregistrer un commentaire