In my last post, I looked at the yields and risk levels of a series of utility stocks and determined that a number of individual stocks looked more attractive than the sector as a whole. I received an email from a reader asking what I thought about selling covered calls against utility stocks as a way to boost income. I wrote about this topic back in 2009, as well as more recently in a series of articles at Advisor Perspectives. Selling covered calls against holdings of low-Beta stocks such as utilities can be quite attractive, not least because there is evidence that options on low-Beta stocks tend to be over-priced.

You can easily calculate the effective total yield that results from being a long a dividend-payer against which you sell a call. For those who are really focused on income, it will be attractive to sell at-the-money calls, those with a strike price near but just above the current asset price. This will provide the highest effective yield boost. As part of this process, I also obtain the implied volatilities for put options with which to validate my projections of risk. To demonstrate how this process works, I have taken a selection of utilities from my last post which also have options traded against them with expiration dates at least a year out. I have arbitrarily settled on using options expiring in January 2015 for these examples. I prefer options expiring at a year or longer to minimize the amount of work involved in maintaining a covered call strategy.

Before proceeding, I want to offer the following disclaimer. This is a post about a methodology and not intended to suggest that any of the resulting positions are necessarily attractive. In general, I shy away from looking at such things on a position-by-position basis and instead focus on the total portfolio.

To begin, I obtain the implied volatilities of at-the-money put options on these stocks and funds as a measure of downside risk. Implied volatility from options prices vary with strike price (the volatility smile or volatility smirk) and also vary depending on whether you are looking at puts or calls. In theory, the implied volatility between puts and calls should match up (according to what is referred to as put-call parity). In real life, this is often not the case. I am not going to delve into the meaning of put call parity violations except to say that I believe that implied volatility on put options is the best measure of downside risk.

For options on SPY expiring in January 2015, the at-the-money (ATM) implied volatility for put options is 18.3%, which is somewhat higher than the 14.6% volatility that SPY has exhibited over the past ten years. This is not surprising after the market has gone up 30% in the last twelve months. I calibrate my Monte Carlo model (Quantext Portfolio Planner) so that the expected volatility for the S&P500 is 18.3% and then run the model to calculate the expected volatility for the selected utilities.

The results are shown below:

| Name | Ticker | Expected Volatility | ATM Put Implied Volatility | Yield |

| First Energy | FE | 29.8% | 28.2% | 6.74% |

| Entergy | ETR | 21.4% | 27.0% | 5.36% |

| Southern Co. | SO | 15.8% | 22.4% | 5.00% |

| Utilities Select SPDR | XLU | 16.0% | 20.9% | 3.90% |

| S&P500 | SPY | 18.3% | 18.3% | 1.90% |

The first thing that should be apparent is that the Expected Volatility (generated by the Monte Carlo model) are very consistent with the implied volatilities. The second thing to notice is that the implied volatilities are higher than the simulated volatilities for two of the three stocks and for XLU. This second feature is a consistent trait of low-beta stocks as noted above. These results suggest that we have a reasonable handle on the relative risk levels of these utility stocks and the utility ETF (XLU).

The next step is to obtain the bid prices (what someone is willing to pay) for the call options that expire in Jan 2015. I have chosen the options with strike prices as close to the current price as possible but that is also higher than the current price. These options have 1.13 years to run. It is simple to calculate the effective annualized yield that you obtain from selling these call options. The results are summarized below. The Total Yield is the sum of the dividend yield and the effective addition yield from selling the covered call. This is adjusted to reflect the fact that the option expires is 1.13 years.

| Name | Ticker | Expected Volatility | ATM Put Implied Volatility | Yield | Current Price | Strike | Call Bid | Call Yield | Total Yield |

| First Energy | FE | 29.8% | 28.2% | 6.74% | $32.60 | $33 | $2.0 | 5.3% | 12.1% |

| Entergy | ETR | 21.4% | 27.0% | 5.36% | $62.28 | $65 | $2.5 | 3.6% | 8.9% |

| Southern Co. | SO | 15.8% | 22.4% | 5.00% | $40.74 | $43 | $1.3 | 2.8% | 7.8% |

| Utilities Select SPDR | XLU | 16.0% | 20.9% | 3.90% | $37.87 | $38 | $1.6 | 3.8% | 7.7% |

| S&P500 | SPY | 18.3% | 18.3% | 1.90% | $180.53 | $185 | $8.1 | 4.0% | 5.9% |

If you are willing to take on a position with a volatility of 28%-30%, you can generate annualized yield from FE of 12.1%.

The Monte Carlo simulation also generates an expected total return that would be consistent with the risk level of a position, and the expected total return for FE is 13.5%. The total yield from FE represents almost all of the expected return. This is similar to ETR, for which the Monte Carlo expected total return is 9.7% as compared to the total yield of 8.9%. It makes sense that the combination of yield and selling a covered call should capture almost all of the available return.

At the other end of the risk scale, you can generate a total yield of 7.7%-7.8% from XLU and SO for risk levels in the vicinity of that of the S&P500.

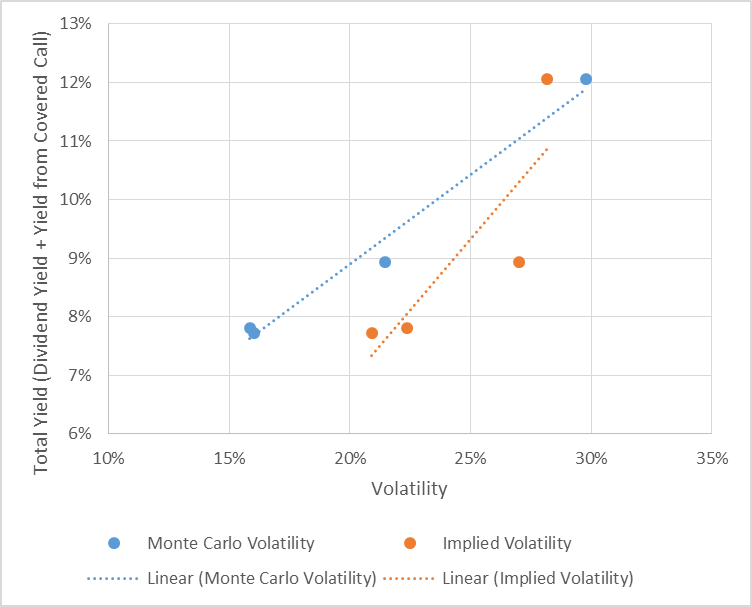

These stocks and fund have negative correlations to the ten-year Treasury yield ranging from -10% (ETR) to -40% (SO). The total yield vs. risk for the utility stocks and for XLU are summarized graphically below.

(click to enlarge)

So, where does this leave us? Using the simulated volatility levels from the Monte Carlo model, we might choose to sell covered calls on any of these stocks or XLU and the choice simply moves us up or down the risk-yield line. The results look somewhat more scattered when we use the option implied volatility and ETR appears to be the least-attractive alternative.

The fact that you can get a total yield (dividend plus call premium) of 7.7% from XLU is notable, not least because the expected volatility of this fund is somewhat less than that of the S&P500. The implied volatility for XLU is a bit higher than that of the S&P500, but this can be explained by the research showing that implied volatility of low Beta asset classes tends to be biased to the high side.

Finally, these results make it really clear why risk management is so important. Even a total yield of 9% to 12% will provide limited comfort in the event of a major drawdown in these positions. A position with annualized volatility of 27%-29% can lose a lot. As a rule of thumb, I have found that it is reasonable to estimate that you can reasonably lose an amount equal to twice the volatility in a bad 12-month period.

Disclosure: I am long SO. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1876611-covered-calls-to-boost-income-from-utility-positions?source=feed

Aucun commentaire:

Enregistrer un commentaire