By Ivan Deryugin

In the biotechnology sector, innovation can come in one of a few forms, including novel drugs or novel ways to deliver existing drugs. BioDelivery Sciences (BDSI) has taken the 2nd path, and through its proprietary drug delivery system - BioErodible MucoAdhesives BEMA - the company has laid the foundation to take share of two sizeable pharmaceutical markets. With a slate of catalysts in 2014 and a share price that has risen just 13% in 2013 (far below the NASDAQ Biotechnology Index's 63% rise), we find BDSI attractive at present levels. The stock is flat from our last public column in July, and we remain optimistic that BDSI can reach upcoming inflection points without requiring an equity financing. Nevertheless, a recent shelf filing suggests that a raise isn't off the table in the near-term, thus we suggest owning the stock with capital set aside for addition if the company raises cash through an equity financing.

Overview

BioDelivery's pipeline is based on its proprietary BEMA (BioErodible MucoAdhesive) technology, which has already yielded one FDA-approved product, Onsolis (fentanyl buccal soluble film) for the treatment of breakthrough cancer pain [Onsolis is also approved in Canada, Europe (marketed as Breakyl), and Taiwan]. BEMA is a small polymer film that is applied to a patient's mucosal membranes (inside the cheek) to rapidly deliver drugs for time-sensitive indications faster than traditional oral dosing. BEMA "strips" attach themselves in less than 5 seconds and dissolve fully within 15-30 minutes of adhesion. BioDelivery licensed Onsolis to Meda Pharmaceuticals for virtually all markets, with the exception of Taiwan and South Korea, and receives royalties on global sales. We note that the FDA has halted the sale of Onsolis in the United States; however, postponement does not relate to the safety and efficacy of Onsolis. Rather, it relates to the drug's manufacturing process. Onsolis has a shelf life of 2 years, and as the Onsolis film strips move closer to expiration, microscopic crystals occasionally form and the strips may fade in color. The FDA has expressed concerns that this may confuse patients and has halted sales of Onsolis in the United States until BioDelivery can reconfigure the manufacturing process. The company met with the FDA in December 2012 and submitted filings for a revised formulation in March 2013. BioDelivery is now waiting for results of ongoing stability studies, and assuming the company's plans are on schedule, Onsolis sales will resume in the 2nd half of 2014. We don't expect Onsolis to meaningfully move the needle for BioDelivery. Consolidated Onsolis royalties amounted to just under $1.8 million in the first 9 months of 2013, and for a company whose research & development expenses surpass $10 million per quarter, these royalties don't generate the capital necessary to fund ongoing R&D.

Bunavail: Changing the Opioid Dependence Landscape

BioDelivery's most advanced product candidate is Bunavail (BEMA Buprenorphine/Naloxone), which is designed to treat opioid dependence. The company submitted a New Drug Application to the FDA on July 31, 2013, and a PDUFA date of June 7, 2014 has been established. In keeping with BioDelivery's strategy, Bunavail is based on buprenorphine, which was first marketed in the 1980's and has a long track record as a treatment for opioid dependence. However, as a series of New York Times articles (available here and here) regarding opioid dependence has shown, Suboxone (buprenorphine marketed by Reckitt Benckiser) is not without controversy, and its clearly defined clinical benefits have been challenged by growing misuse and abuse, with some addicts themselves becoming addicted to Suboxone. Right or wrong, the controversy surrounding Suboxone has positioned BioDelivery to offer an alternative, one that is backed by stronger safety and dosing data. Reckitt Benckiser has already tried to block BioDelivery from filing for approval of Bunavail, filing petitions with the FDA to block the agency from accepting the Bunavail NDA through the 505(b)(2) approval pathway, arguing that Suboxone's patent exclusivity with Orange Book-listed patents does not allow the FDA to accept the filing. The FDA denied the petitions in September 2013, and the Bunavail NDA is now under review.

Bunavail's safety profile is favorable when compared to Suboxone (available in both tablet and sublingual film form). In head-to-head bioequivalence studies of Bunavail vs. Suboxone, patients in the Bunavail arm saw a significantly lower rate of constipation (13%) versus Suboxone (41%), as well as bioavailability that was twice as high, as shown in the table below.

Bunavail Bioavailability vs. Suboxone

Metric | Bunavail | Suboxone |

Relative Bioavailability | 50% | 25% |

Equivalent Buprenorphine dose | 4 mg | 8 mg |

Absorbed Amount via buccal mucosa | 2 mg | 2 mg |

Delivered to GI Tract | 2 mg | 6 mg |

Adverse events were manageable in the Bunavail arm of the study, with headaches serving as the most common side effect, occurring in 5.2% of patients, followed by fatigue and lethargy, reported in 2.4% of patients. Taste (an important factor in sublingual/muccal delivery) was also favorable. In its own clinical studies, almost 93% of Renckiser's Suboxone patients reported unpleasant tastes, versus 8% for Bunavail in the BNX-201 trial, due to its citrus flavoring. Given that Bunavail is based on a well-documented therapeutic agent and features a favorable side effect profile, we believe the product stands a good chance of securing approval.

But what of the commercial opportunity? Can BioDelivery take share from Suboxone? And more importantly, won't the presence of generics negate the market opportunity?

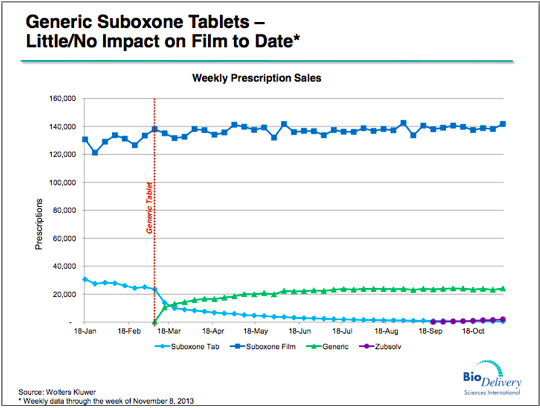

Suboxone generated sales of more than $1.5 billion in 2012, and currently holds virtually the entire market; Zubsolv [from Orexo (GM:ORXOF)] was approved by the FDA in July 2013 but to date has had little impact on the market. Generic Subaxone tablet sales began in March 2013 [Actavis (ACT) is attempting to launch generic Suboxone film strips, but has been sued by Reckitt Benckiser], but again have not dented sales of film strips.

(Click to enlarge)

Suboxone film strip sales have not been affected by the presence of generic tablets, and the arrival of generic film strips would still allow BioDelivery to compete on Bunavail's bioavailability, lower dosing, and favorable side effect profile. The company is forecasting that it can capture 25% of the market for opioid dependence, delivering $250 million in annual sales by 2018.

Currently, BioDelivery holds full rights for Bunavail, and is in the process of deciding on a commercialization strategy. The company has committed to partnering for the drug's international launch, but has not yet made a decision on whether to seek a partner in the United States. In conjunction with its Q3 results, the company stated that it would have details on its strategy "early next year." Note that with 75% of buprenorphine-prescribing physicians located east of the Mississippi River, the geographic area that BioDelivery would have to target on its own is far smaller than it might seem.

BEMA Buprenorphine: A New Approach to Chronic Pain

BioDelivery's 2nd BEMA pipeline product is BEMA Buprenorphine (which we will refer to as BEMA-B), now in Phase III trials for the treatment of chronic pain. BEMA Buprenorphine is developed in conjunction with Endo Pharmaceuticals (ENDP). BEMA-B will compete with other opioids such as Vicodin and morphine, and recent FDA actions have made the competitive landscape more favorable. In October, the FDA voted to recommend to the Department of Health and Human Services and the Drug Enforcement Administration that hydrocodone pills such as Vicodin be reclassified as Schedule II drugs (a designation already given to morphine), which would tighten restrictions on refills and rescind the ability of nurses and physician assistants to prescribe the drugs. Given that the D.E.A. has spent years pushing for such a measure, and that FDA advisory panels themselves recommended this move in early 2013, the policy change is expected to go into effect in early 2014. Buprenorphine has retained its classification as a Schedule III drug, which allows for easier access to refills and has less stringent prescription regulations, including the ability to phone in or fax refill prescriptions for 6 months.

Existing Phase III data for BEMA-B suggest a quality drug profile. In early 2011, BioDelivery announced interim results from the first of several Phase III studies involving BEMA-B. The primary endpoint of this study was the overall pain intensity difference between BEMA-B and placebo. Here, BEMA-B failed to achieve statistically significant efficacy (p=0.067) due to high response rates in the opioid-naïve segment of the placebo arm. However, the company suggests that there were a significant number of patients that did not titrate beyond the starting dose, skewing the results of the trial. When this segment of the patient population was eliminated, BEMA-B did indeed achieve statistically significant efficacy (p=0.025). We note that the agreement between BioDelivery and Endo Pharmaceuticals was signed in January 2012, meaning that Endo was fully aware of these trial results when it inked the agreement with BioDelivery. In August 2012, BioDelivery began the 2nd part of its Phase III program for BEMA-B, which consists of two separate Phase III studies in opioid-naïve and opioid-experienced patients. The two studies will enroll a total of 1,215 patients [740 in the naïve study (BUP-308) and 475 experienced study (BUP-307)], and both a double-blind and placebo-controlled. Both studies are focusing on patients with severe and chronic lower back pain that requires 24-hour opioid analgesia. Dosing will range from 30-160 mg in the experienced study, and up to 10 mg in the naïve study. The primary endpoint of these studies is the change from baseline in mean average daily pain intensity scores after 12 weeks of treatment.

On September 4, 2013, BioDelivery and Endo provided an update on the studies, suggesting that an interim analysis had found that no adjustments were necessary to the BUP-308 study, but that additional patients were needed in the BUP-307 study. We note that an independent biostatistician conducted the analysis, and both Endo and BioDelivery remain blinded to the studies. In November, BioDelivery reiterated that data from BUP-308 would be available in early Q1 2014 (perhaps alongside Q4 2013 results), and that data from BUP-307 would be available in mid-2014. Assuming positive results, BioDelivery and Endo are planning to file for FDA approval in the 2nd half of 2014, with a launch in 2015.

The agreement with Endo entitles BioDelivery to up to $180 million (including $30 million upfront) in milestone payments, of which it has received $45 million as of the end of Q3 2013. BioDelivery is eligible for an additional $80 million in clinical and regulatory milestone payments, and $55 million in sales-based payments, which are in addition to royalties on sales of BEMA-B; BioDelivery has stated that the rate ranges from the "mid to upper teens," and given the size of BEMA-B's addressable market, these royalties should be meaningful. In 2012, there are around 130 million prescriptions written for hydrocodone (to say nothing of the millions of OxyContin and morphine prescriptions written), and market research has shown that hydrocodone is the most likely source of market share for BEMA-B. As a frame of reference, BioDelivery has stated that siphoning off just 1.2 million prescriptions (around 1%) each year equates to $300 million in annual sales ($30 million in royalty income at a conservative 10% royalty rate). With the backing of Endo, we believe that a market share of 1% is conservative, and that royalty income should be meaningfully higher. Year-to-date, BioDelivery's expenses run at around $16.579 million per quarter, so BEMA-B needs to capture just 3% of the market ($90 million in royalty income at a conservative 10% rate) for BioDelivery to begin posting operating profits, without taking into consideration royalty income for Onsolis or sales of Bunavail.

Topical Clonidine Gel: Moving Beyond BEMA

BioDelivery's third and final pipeline product is topical clonidine gel, now in Phase II trials for the treatment of painful diabetic nephropathy. Clonidine has already been approved by the FDA (in tablet form) as Kapvay for the treatment of ADHD and is sold by Concordia Pharmaceuticals. In addition, Pfizer's (PFE) Nexiclon is a liquid and oral suspension form of clonidine. BioDelivery licensed clonidine from Arcion Therapeutics in March 2013 in exchange for 500,516 shares, a $2.5 million payment upon FDA acceptance of clonidine's NDA, as well as up to $60 million in cash payments for sales milestone, but only if net sales in the United States surpass $200 million on an annual basis (BioDelivery has forecast $300 million in peak annual sales) and single-digit royalties on global net sales. If approved by the FDA, clonidine gel would become the first topical treatment for painful diabetic nephropathy, and we note that the FDA has granted fast track status to clonidine. Clonidine works by stimulating the inhibition of the pain receptors in a patient's skin, and earlier Phase II studies have shown evidence of this. However, as with Bunavail's earlier Phase III studies, unfavorable patient populations muddled clonidine's prior Phase II study results. In its last Phase II study with 179 patients, clonidine failed to show statistically significant efficacy. This study, however, included patients who no longer had functioning nerve receptors. Given that clonidine works by stimulating receptor inhibition, the absence of functioning receptors made it essentially impossible for clonidine to show any efficacy. The drug showed statistical significant efficacy (p=0.01) within the subset of patients that did have functioning nerve receptors.

(Click to enlarge)

On December 2, BioDelivery announced that after meeting with the FDA on November 21, fast track status for clonidine has been reiterated, and that Phase III trials are set to begin next year. The FDA has agreed with BioDelivery's proposed Phase III program, which is formed of two placebo-controlled studies, and one specific safety study. The first Phase III trial is set to begin in Q1 2014, with data to be available as early as the end of the year. If successful, the 2nd Phase III study is set to be initiated in 2015, with an NDA now forecast for 2016, assuming that these studies yield positive outcomes. Existing treatments for painful diabetic nephropathy, such as Lyrica and Cymbalta, have failed to yield significant improvements in pain. Pfizer has admitted that it does not know exactly how Lyrica works, and Eli Lilly (LLY) has done the same with Cymbalta. The commercial opportunity for topical clonidine will likely become clear when BioDelivery provides further clarity on topical clonidine's side effect profile and efficacy in relation to existing treatment options.

Financial Review

BioDelivery ended Q3 2013 with just over $38 million in cash & equivalents and debt of just over $19 million, of which $5.333 million is due within the next 12 months. This debt, which was added to BioDelivery's balance sheet in July 2013, is the product of a loan agreement with MidCap Financial, and the full loan term is for 36 months. BioDelivery's burn rate has averaged $14.98 million per quarter in 2013, meaning that at present levels, the company has less than 3 quarters of cash on its balance sheet. However, this does not take into account pending milestone payments. The completion of Phase III BEMA-B studies entitles BioDelivery to an undisclosed milestone, and positive results from BUP-308 and BUP-307 would also lead to the injection of fresh capital from Endo. A commercialization agreement for Bunavail would provide further non-dilutive capital. In any case, BioDelivery will likely wait for clinical data from BUP-308 before making a decision on the size and timing of a secondary offering, and if BUP-308 data is positive, BioDelivery could utilize that as a catalyst off of which to strengthen its balance sheet, thereby providing traders with a defined exit opportunity (the company could also raise capital off of FDA approval of Bunavail, depending on its burn rate in 2014). The company filed an S-3 on November 29, allowing the company to raise up to $75 million in an unspecified mix of debt and equity, and we note that BioDelivery also has access to a $15 million at the market facility, which it may be using to bridge any capital needs until BEMA-B data is released.

We see the most likely outcome as a secondary offering just prior to or following the BEMA-B opioid-naïve data early in the first quarter, depending how far the stock advances beforehand. Either way, we'd prefer to be involved ahead of this decision, with powder dry to add when/if BDSI raises more capital. Bear in mind, however, that BDSI has some optionality with the Endo milestones and a potential Bunavail partnership.

Conclusions

BioDelivery Sciences has crafted a solid pain franchise, with defined commercial opportunities for Bunavail, BEMA-B, and clonidine, as well as compelling competitive propositions relative to existing standards of care. Endo Pharmaceuticals has provided an endorsement of BioDelivery's BEMA technology, and with the resumption of Onsolis sales in the United States in 2014, BioDelivery's BEMA technology will once again be visible to physicians in the United States, which will serve to highlight the utility of Bunavail and BEMA-B. We believe that with shares under $5, BioDelivery is undervalued relative to its future prospects, and we would be buyers ahead of a catalyst-rich 2014.

Disclosure: I am long BDSI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. PropThink is a team of editors, analysts, and writers. This article was written by Ivan Deryugin. We did not receive compensation for this article, and we have no business relationship with any company whose stock is mentioned in this article. Use of PropThink’s research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, PropThink, LLC and persons or entities with whom it has relationships (collectively referred to as "PropThink") has a position in all stocks (and/or options of the stock) covered herein that is consistent with the position set forth in our research report. Following publication of any report or letter, PropThink intends to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. To the best of our knowledge and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and not from company insiders or persons who have a relationship with company insiders. Our full disclaimer is available at www.propthink.com/disclaimer. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1876641-biodelivery-sciences-delivering-profits-in-2014?source=feed

Aucun commentaire:

Enregistrer un commentaire