When you think of Coca-Cola (KO) in the context of blue-chip investing, you probably it's the one indispensable company cropping up in 401k mutual funds, trust funds, pension plans, and plain-as-day brokerage accounts across the country. Maybe you think of its 30% returns on equity, 500+ brand collection, or $10 billion in annual profits that literally span the globe across 210 countries. Maybe, as you watched highlight reels of the 50th anniversary of President Kennedy's death, you mused about all of the changes in America since then, and simultaneously connected the dot that Coca-Cola stock has raised its dividend during every year since that defining, tragic assassination.

But while Coca-Cola is gold-plated with positive associations of wealth-building and growing its dividend every year throughout most of the life of Seeking Alpha's readership, BP Oil (BP) seems to elicit none of those positive connotations. BP cut its dividend in 1993, 2000, and 2010. Linear dividend growth is not part of this company's profile. It is mentally associated with negligence, catastrophe, and a dividend that can be charitably described as "fluctuating."

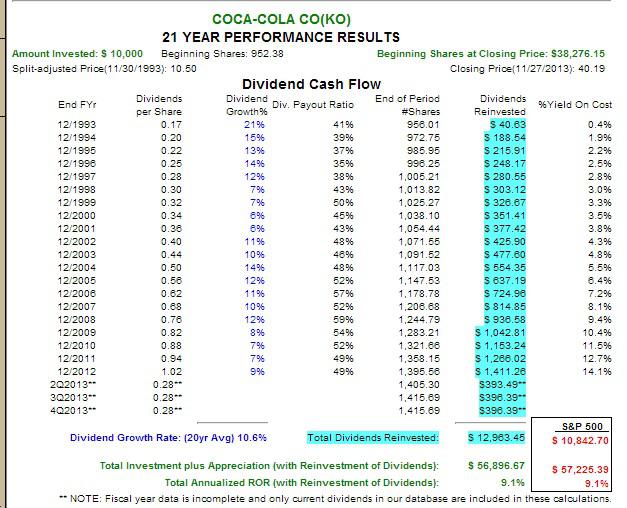

Yet, look what happens when you take a look at these F.A.S.T. Graphs that compare fates of investors that chose to make $10,000 investments in Coca-Cola and BP respectively, on November 30th, 1993.

(click to enlarge)

(click to enlarge)

For the Coca-Cola investor, the results were quite nice. The investment compounded impressively at 9.1%, turning every dollar invested back then into $5.68 today. With a yield on cost of 14.1%, you would be receiving $0.14 annually today for every dollar you invested into Coca-Cola in 1993.

Yet, BP did a little bit better. Despite the dividend cuts, wild price fluctuations, and an oil spill so severe that stock market commentators regularly discussed whether the firm would even survive intact, the company still managed to compound wealth at 9.9% annually, a superior rate to Coca-Cola. Every dollar invested into BP twenty years ago would be worth $6.56 today. And the yield-on-cost of the investment may be substantially higher than what you might expect, coming in at a current rate of 26.2%. For every dollar you tucked away into the oil giant twenty years ago, you'd be collecting over a quarter in annual dividend income today.

The question worth examining-the one which will improve our tools as long-term investors-is this: What causes a problematic oil company with no exceptionally growing dividend policy to outperform an excellent blue-chip holding that simultaneously moves from strength to strength, growing its dividend every year?

Here's my answer: Coca-Cola had two strikes going against it over the past twenty years, compared to BP. First, its valuation was extraordinarily high during much of the reinvestment period in the late 1990s. Reinvesting your dividends into Coca-Cola stock between 1997 and 2002 was not an optimal decision. The company's P/E ratio was above 30 every year during that period, and it averaged over 50x earnings in 1998. You don't get rich during the moments when you reinvest dividends into large companies with 2% earnings yields.

BP, being a large oil company, does not become overvalued for extended periods of time in the way that top-caliber non-cyclical companies do. BP had a brief moment in 1998 when profits temporarily collapsed from $2.44 to $1.39 per share and its P/E ratio hit 30, but for the most part, BP has been a company that trades at a valuation in the high single digits or low double digits. Each dollar reinvested into BP bought you a much larger claim on future profits than someone reinvesting into Coca-Cola.

The second strike against Coca-Cola is that its dividend in relation to share price is much lower. From 1997 to 2002, Coca-Cola's dividend yield was below 1%. The only time its dividend yield ever crossed 3% for an extended period of time was during the most recent recession (2008, 2009, and 2010).

BP, although its dividend was not growing in a linear fashion, managed to return much larger chunks of income to its owners. BP's dividend has regularly been above the 3% mark, with the figure regularly hovering around the 4-5% mark since 2008 (minus the nine-month period on 2010 when the dividend was suspended). In short, for much of the past twenty years, BP owners that reinvested were taking a dividend payments roughly doubled that of Coca-Cola owners and reinvesting it into a company trading at one-half or even one-third the valuation level.

The comparison between Coca-Cola and BP validates an important premise that often shows up in the work of Wharton professor Jeremy Siegel. The notion is that taking large chunks of income and reinvesting them at low valuations can often to lead better returns than someone owning a company that had a higher growth rate.

Some of you might be thinking, "That's nice, Tim. I wish you would have told me that twenty years ago. What am I supposed to do with that information, now?"

And my answer would be this: You should look to companies that have high current yields and seem likely to return large chunks of income to owners over the next five, ten, fifteen years. Ideally, you should find companies that blend that character trait with a low valuation simultaneously.

One place to study is the tobacco sector. Altria (MO) is sitting there with its 5.19% dividend yield, Lorillard (LO) with a 4.29% yield, and Reynolds (RAI) with its 5.00% yield.

Personally, Altria is the only one coming close to meeting the second element of that test: low valuations. Tobacco companies compound best when you reinvest your dividends at P/E ratios between 10-13, which has been frequently the case historically. Now that Altria is creeping below 15x earnings, it is getting closer to that magic spot. But the higher valuations of Lorillard and Reynolds American would suggest prudence and patience before initiating a position, perhaps.

The other place to look is, well: Big Oil. Conoco (COP) has enjoyed a recent run up, but BP and Royal Dutch Shell (RDS.B) are still in that sweet spot of companies yielding between 4.5-5.25% and trading at P/E ratios in the single digits. There are a lot of roads to wealth creation, and one of my favorites is taking high yielders around the 5% mark and reinvesting them into securities trading at 6x, 7x, or 8x earnings.

Finding an excellent company is one component of the wealth-building process. But ideally, you should find the intersection of price with excellence. Because oil companies see their profits temporarily fall by 50% or so twice every generation, investors tend to demand high yields (particularly from the European supermajors) and value the companies around 10x earnings (or less) for extended periods of time. You should keep in mind that this is fertile ground for building wealth.

If you walked up to someone on the street and said, "I've owned BP stock for the past twenty years", the person would probably respond, "I'm sorry." And if you told someone you had been a shareholder of Coca-Cola for the past twenty years, that same person might start wondering if you could find room for one more person in your will. But surprisingly, it is the BP investor that has done a bit better. As you go forward, you should categorize this information right next to the fact that Royal Dutch Shell has compounded returns north of 14% annually since 1907/1908. Share price growth is a nice way to get richer, but don't forget about Big Oil and Big Tobacco. High dividends and low P/E ratios can get you there, too.

Disclosure: I am long BP, COP, RDS.B. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1870261-why-do-troubled-companies-like-bp-outperform-coca-cola-for-20-years?source=feed

Aucun commentaire:

Enregistrer un commentaire