The business

ChipMOS TECHNOLOGIES (Bermuda) LTD (IMOS) is the largest independent provider of testing and assembly services for LCD and other flat panel display (FPD) driver semiconductors globally and a leading provider of testing and assembly services for advanced memory products in Taiwan. It operates in 4 business segments as outlined by the graphic below. Note that it is one of the only two companies globally providing gold-bumping services.

(click to enlarge)

* Source - ChipMOS Investor presentation

ChipMOS counts the who's who of the semiconductor industry as its customers. One of the most notable customers is Micron (MU) which has emerged as a big winner from the ongoing consolidation of the memory industry through its acquisition of the Japanese company Elpida.

* Source - ChipMOS Investor presentation

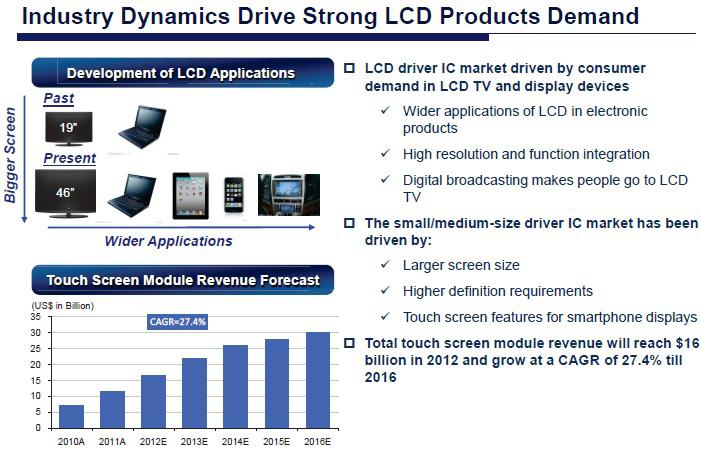

The breakneck growth in smartphones, tablets and high-definition TV's clearly bodes well for the future of ChipMOS as the demand for semiconductor and LCD driver testing is probably not going to go down anytime soon.

(click to enlarge)

* Source - ChipMOS Investor presentation

The opportunity

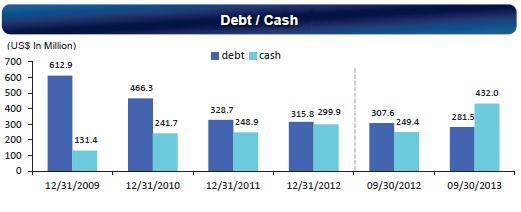

Being a small-cap company based in Taiwan, ChipMOS is off the radar of most institutional investors which is perhaps the reason that the shares are trading pretty cheap relative to the quality of the business. The company has tailwinds at its back and that is reflecting in its improving fundamentals: a stable and growing revenue stream, upward trend in margins and a balance sheet becoming healthier by the quarter.

Since year-end 2009, the company has managed to pay off 330 million USD in debt (It came down from 612 million to 281 million) and at the same time increased its cash-in-hand from 130 million to 430 million USD. Hence its net cash position has moved from - 482 million (minus 482 million) to +150 million: A total change of roughly 630 million. The magnitude of this change can only be appreciated in the context of the company's current market cap: 591 million USD.

(click to enlarge)

* Source - ChipMOS Investor presentation

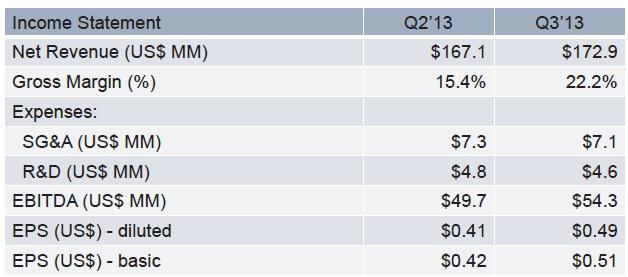

The free cash flow (FCF) per share was 4.1 USD in 2011 , 3.3 USD in 2012 and 1.35 USD in first 3 quarters of 2013. The current share price is about 20 USD giving a ~10% FCF yield for the current year and more on a normalized basis. This is cheap based on the improving fundamentals and growing business, and the market is not paying anything for further potential growth.

* Source - ChipMOS Investor presentation

The FCF is starting to fall to the bottom line as the depreciation from an ill-timed capacity build in 2007-08 wears off. Hence, EPS is showing a positive trend too.

(click to enlarge)

* Source - ChipMOS Investor presentation

The stock is clearly undervalued and the management knows this. Therefore, there was a stock buyback plan in place but the management did not retire as many shares as investors would have wished. The buyback plan has recently been shelved and instead the management has another plan to unlock the company's value.

Bring me home

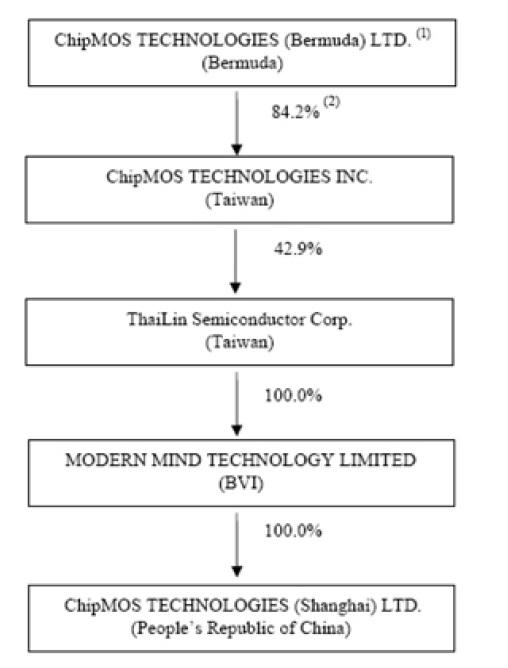

ChipMOS is a Taiwanese company which is currently listed in Bermuda and trades on the NASDAQ in US. It has a pretty complicated corporate structure which has been well-explained by Jaret Wilson in his excellent SA post on the subject. This has perhaps served to confuse investors and hidden the true value of the ChipMOS franchise.

(click to enlarge)

* Source - ChipMOS Annual Report

Understandably, ChipMOS has decided to streamline its corporate structure. The company is much better known in Taiwan than in the US and this is surely the reason that the management has decided to list the company back home in Taiwan and are on track to make it happen.

The company revealed during the 3rd quarter 2013 that ChipMOS Bermuda has reduced its ownership of ChipMOS Taiwan to below 70% which is a requirement for ChipMOS Taiwan to list on the Taiwan stock exchange. On 27th November 2013, ChipMOS Taiwan submitted an application to list on the Taiwan stock exchange (TWSE). The listing is expected to be completed by second quarter 2014.

Conclusion

ChipMOS Bermuda now owns approximately 62.1% of the outstanding shares of ChipMOS Taiwan. When ChipMOS Taiwan is listed on the TWSE, the new stock will probably be in high demand and the prices of IMOS and the newly listed company will have to move in lockstep. Therefore, I believe this to be an excellent opportunity to invest in an undervalued growth business with tailwinds at its back and with a clear near-term catalyst to unlock its value. Once the listing on TWSE happens, the shares of IMOS could easily trade in the $30-40 range.

Disclosure: I am long IMOS, MU. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1870371-taiwan-listing-of-chipmos-in-2014-set-to-unlock-value?source=feed

Aucun commentaire:

Enregistrer un commentaire