In today's Oxen Group recap, we will be looking at Stratasys (SSYS) in our daily deeper look as well as looking at Ford (F), in our company news section, after the company reported its latest auto sales. The Oxen Group covers both companies year round, and we want to update our current pricing to reflect recent occurrences. Ford had another solid sales report, but it dropped...why? Additionally, as always, we will do our typical market overview, important news breakdown, and give our perspective on what's moving the market.

Market Overview

The markets moved lower on Tuesday, following through from Monday's weakness. There was not a ton of news coming out today, and it appears the market moved in tandem with Monday's overall tempo. Without much catalyst, traders were looking to a potential December taper as well as taking profits before a key Thursday-Friday period this week. During that time, we will get GDP, unemployment rate, and non-farm payrolls. Apple (AAPL) was helping to hold up the Nasdaq as the company neared a deal with China Mobile (CHL), the largest mobile company in China. Additionally, sales were out for major US auto manufacturers including Ford, GM (GM), and Chrysler, which we will cover further in the article.

Deeper Look

Stratasys

Overview

Today, we are taking a look at Stratasys. Heading into today, we had a Buy rating on the stock with a $141 price tag. We want to update the company after recent developments, discuss the company's main catalysts, look at industry trends, and update our pricing model.

Industry Trends

The 3D printing industry has been extremely popular over the past couple of years as these companies have been able to successfully leverage relationships with advanced manufacturing to print parts and help build models. The pie in that industry continues to grow, but the true growth portion of the market is in the consumer market. If consumers can adapt 3D printers, these companies will be able to live up to their valuations. Imagine printing a new piece of jewelry, some household tool, or nails to build something. The potential is endless to print.

(click to enlarge)

As we noted in a previous article about the potential:

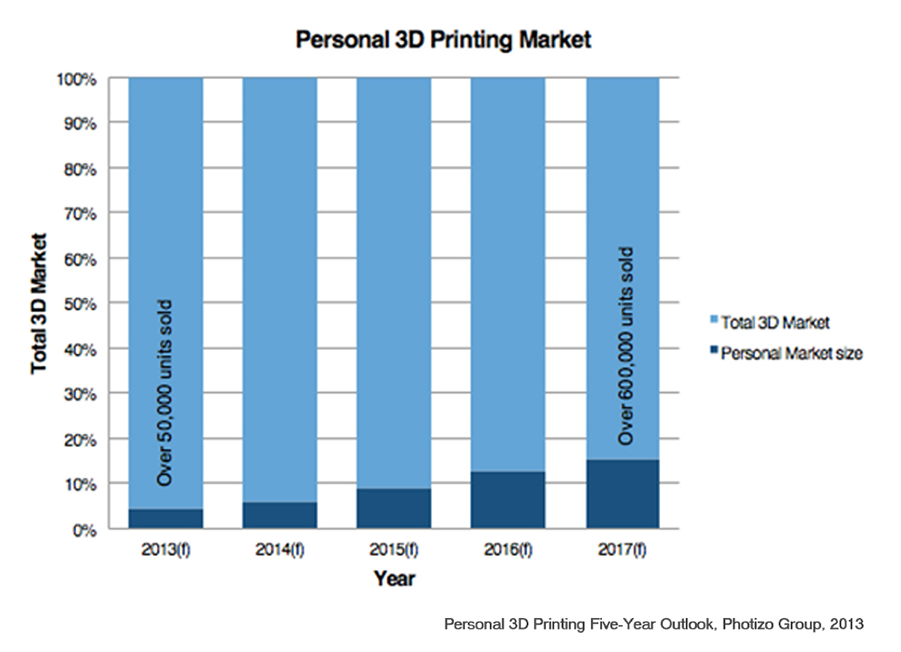

The 3D consumer printing industry potential is gigantic, and it should provide a lot of returns for the company. The company has noted that they believe 35K - 40K desktop printers were sold in 2012, and that number should double in 2013. From there, it's anyone's guess. Photizo Group, an imaging research firm, believes that 15% of the 3D printing industry could be personal consumption by 2017. They see the number of printers being sold at 650,000. Even if Stratasys had a quarter of the market, they could make nearly $500 million at current pricing for Mojo and Replicator. Those sales would just be in consumer printers alone and does not count the upside in inks and maintenance parts as well as the company's advanced manufacturing division that is growing at significant rates as well. As one can see, the growth here is definitely exciting.

Here are some statistics on the potential for consumer industry:

· 15% of printing consumption will be personal printing by 2017

{kind=link}

· Gartner has predicted that sub-$100K 3D printers will grow to 56K units in 2013 - a 49% jump over 2012

· The growth rate of personal 3D printers is expected to jump 75% in 2014 to nearly 100K units

· With only a few chains selling 3D printers, analysts predict that by 2015 the product will be in the 50 largest multinational retailers

Major Catalyst

Building on our conversation in the industry trends section, the main catalyst moving forward for SSYS is their ability to leverage and execute on the opportunity in the consumer market. Advanced manufacturing will always have a major part of this industry, but there are billions more consumers. Some of the issues that will occur are the breadth of what can be printed, the cost of the printer, and the maintenance of margins. Right now, SSYS operates with very solid, premium margins. Can that be maintained in their push into the consumer market?

Stratasys already made the first proper move by closing a deal with MakerBot, a consumer-based 3D printing manufacturer, back in August. Here is some more on that deal:

That deal brings in an expert team on consumer 3D printers. Up until the deal, Stratasys had not shown less interest in moving into the consumer market. Their lowest-priced device, Mojo, came in with a price tag of $10,000, and it was marketed toward small businesses that needed prototype devices, such as boutique artisans, architects, and design stores. Whether or not the deal was done out of necessity or out of general interest, MakerBot had become a player in the game with its Replicator and Replicator 2 printers that came in at much cheaper prices (around $2000).

3D Systems (DDD), the main competitor for SSYS, is also pushing into this space. The company has launched its Cube printing system, starting at $1299. The company wants to focus on printing household items, jewelry, and more. SSYS, however, is taking a slightly different approach. DDD wants consumers to buy their product. SSYS is starting by partnering with UPS (UPS) to provide 3D printers in-store. In this way, consumers can print a product at the store and ship it right away. It is similar to the old style of printing and copying at Kinko's, which was a great stepping-stone for in-home printers. SSYS will build its brand name and get more users using the product in this way than DDD will be able to by selling products at such a lofty price tag.

How is the company doing so far on this push?

In the company's latest earnings report, consumables are doing well. The company noted that it had seen a 30% increase in revenue compared to last year. Customer usage and growing install base has helped them. Yet, the company also noted that they are still not marketing directly to the everyday consumer yet as they continue to still wait for the consumer to catch up:

We think we have very aggressive marketing regardless of the time of the year. But again, I think that MakerBot today is targeting, like you said, I think correctly, low-end professional markets and multiple consumers which are individuals that have some technical capabilities are obvious, and we're having to market to them aggressively within the whole year and especially during the holidays.

Overall, the company has a lot of potential here to take part of this market share. DDD is in the lead at getting in the homes, but we prefer SSYS's route of working with clients that have a lot of use for the products, marketing through partnerships, allowing other users to try the printer first hand, and will eventually push into that area.

Pricing/Valuation

Right now, SSYS has a future P/E of 50.7, which is definitely strong. Yet, it represents the incredible opportunity and fact that net income is still limited compared to the strength of revenue. The company has only 2.0-price/book value, which shows you that there is potential in shares still. Let's take a look at various potential growth rates for key factors that will go into our DCF analysis.

Revenue - The company is expecting to continue to grow by 20% or more per year for the next several years. We are expecting revenue to come in around $480M for this FY with growth to around $650M in 2014. From there, we expect growth rates to taper to around 20% per year like the company has predicted.

Operating margins - The company wants operating margins to push to 15-20% over the next several years. Right now, operating income will come in negative for the year due to merger costs with MakerBot, but that should come back down. We would expect operating margin to improve pretty quickly to around 15% by 2016 and closer to 20% by 2017.

Capex - The company will likely continue to see capital expenditures grow and likely move to around 5-6% of revenue as the company continues to dedicate to a major expansion plan over the next several years. Depreciation should move up at a similar rate.

When we use this information in a DCF analysis, we use a cap rate for the company of 4.0%, which shows stronger growth levels. We used a tax rate of 20%. When we use that, we see that shares are now worth $146. The company's increased cash helped the price tag jump, but we also increased capex potential as well. With shares at $122, there is still decent upside. Further, this model is for through 2017. When we adjust to 2018, we see shares worth $165, meaning this stock is still a solid buy.

Company News

Today, in our company news section, we will be diving into Ford. The company took center stage today after they released their latest round of automotive sales. The company reported November sales were 7% higher year/year, beating 3% expectations. In the face of a government shutdown in the prior month, F still executed very well, selling over 190K units. Trucks saw a 17% growth rate, which is very important because they fetch a higher margin than cars, which were up 6%. SUVs were down 2%. Further, Ford's F-Series sold over 65K units, making it the bestselling vehicle in the country. Even Lincoln performed well with a 17% increase in sales year/year.

Shares, however, were dropping hard on the day. Why? Sales beat expectations, the company has the top-selling car, and it is selling more of its higher margin cars than before.

It could be that in a conference call, the company reported that it would build fewer cars in Q1 2014 than they did in 2013 and investors are cautious that 2014 will not be as strong for F. After 50%+ gains in the past year, investors may want to take some profits off the table. Additionally, it did not help that the company called the month "fairly typical" in its sales. Additionally, despite the strength in Lincoln, the company noted that its mid-sized car market was tough and they need to monitor it closely. Those red flags took some of the joy out of the report.

We have been banging the table to buy Ford since the beginning of the year, and those that listened are up 35% YTD. Yet, there is definitely more upside in these shares. Let's take a look at some of these concerns.

The company building fewer cars than they did one-year prior is actually not a big issue. The company has built a lot in 2013, and they have a bit of inventory to work off. The company had only 517K vehicles at the end of November 2012. This year, they have 682K. It is not that sales are bad, but that the company has oversupplied some on the front end. With a difference of 160K vehicles in inventory, the company is only dropping supply by 2%. Therefore, that means the company expects to see another strong December and beginning to 2014. We actually see the number as bullish with so much inventory still on the ground.

When talking about "fairly typical" results, Ford was noting that the pace of sales coming in at the back end of the month was typical of consumers, and it is not a negative at all. Finally, the company's issues at Lincoln are nothing new. Lincoln is about 3% of total business for Ford, and it is just not a make-or-break line. In fact, the company also noted they are building 4 new Lincoln models.

As we have noted before, we believe Ford has potential to over $20 this year. We are going to likely miss that somewhat, but we have a 2014 price target of $24, so we expect another 50% of upside in 2014.

Tomorrow's Outlook

Tomorrow, we will see the market get some more important news in the way of ADP Employment Change, Trade Balance, New Home Sales for September and October, ISM Services, and the Fed Beige Book. It is an extremely busy data day. Employment numbers will be crucial to how the market sets up for Friday and will work in tandem with the Beige Book to give the market a sense of potential for taper by the Fed. The Trade Balance is always crucial as well as new home sales. It is a packed full day. If jobs are strong, it pushes the potential for Fed taper further. If they are very good, though, it gives the market strength. A large beat is what we want. A slight beat likely spooks the market. The S&P 500 (SPY) and Dow Jones (DIA) have their work cut out to retake key levels of 1800 and 16000

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More...)

Business relationship disclosure: I have no business relationship with any company whose stock is mentioned in this article. The Oxen Group is a team of analysts. This article was written by David Ristau, one of our writers. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1874931-stratasys-and-ford-remain-solid-buys-whats-next-for-the-market?source=feed

Aucun commentaire:

Enregistrer un commentaire