SandRidge Energy (SD) under the leadership of former CEO Tom Ward was a perfect example of a company in which the interests of management were put before those of the company's shareholders. Huge salaries and corporate perks were bestowed upon management and Ward in particular, while profitability and gains in the stock price were conspicuously absent. Under the leadership of the new CEO James Bennett, the company has shifted its tune and really seems to be on the right track. SandRidge has dramatically lowered its cost structure, increased production while maintaining the same level of CAPEX and has improved on its capital allocation. Moving forward, SD represents a leveraged play on higher oil and gas prices, which combined with enhanced corporate governance, could lead to 50% appreciation from current levels.

The last five to ten years has produced such tremendous innovation in the energy space that it compares quite favorably with the technological innovations of the 1990s. Most of the investing public has become aware of horizontal drilling and the corresponding impact on increased natural gas supplies in North America, which is having dramatic geopolitical and economic consequences. Less understood are the innovations that have begun to emerge alongside horizontal drilling, such as stack drilling, which significantly lowers the costs per well when executed correctly. These technological marvels have been a dual edged sword in that they have boosted production, but the ending result has been to greatly reduce prices for natural gas in particular. Therefore, it has become necessary for just about every energy company that I've researched to shift production to oil and natural gas liquids where profit margins tend to be fatter.

SandRidge has made tremendous progress shifting production towards liquids through various acquisitions over the years. The company's biggest issues were the egregious expense structure and the fact that the company consistently spent far too much on CAPEX in relation to its operating cash flow, which pressured the company's leveraged balance sheet. The attractive elements of SandRidge are its high quality asset base, which offers easily attainable production growth and the continued improvements that the company has made in lowering its production costs. The company has made large investments in areas such as a saltwater disposal system, which it is able to leverage along with stack drilling, to consistently bring down its costs per well. For example, well costs are now less than $3MM and lease operating expenses have improved 22% YoY. Improved IRR's combined with flat capital expenditures will propel returns on invested capital, boost EBITDA and control leverage.

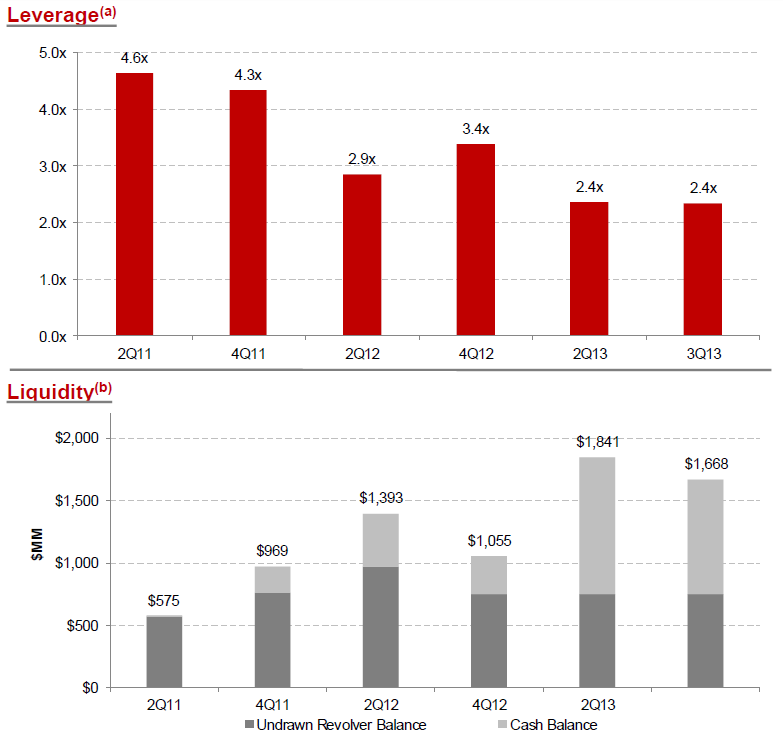

Earlier this year, SD set out a goal to reduce G&A expenses by 25% from a $200MM run rate to $150MM by Q4 this year. The company was able to reach that goal a full quarter ahead of expectations with an adjusted G&A run rate of $144MM. The fact that the company has been able to reduce G&A expenses so quickly shows the amount of fat that was symptomatic of the company's corporate governance prior to new management. As time goes by, I expect the company to further improve these metrics and as the market participants begin to recognize that the company has abandoned its profligate ways of the past, the valuation of SandRidge has considerable upside potential. The company closed the 3rd quarter with a 2.35 times leverage ratio and $1.7 billion of liquidity, which is comprised of $920MM of cash and approximately $750MM in borrowing capacity. Importantly, given the company's debt load, SandRidge has no debt maturities prior to 2020, so I'd expect the company to be able to grow into its balance sheet.

(Click to enlarge)

(Click to enlarge)

Source SD 3rd Quarter Earnings Presentation

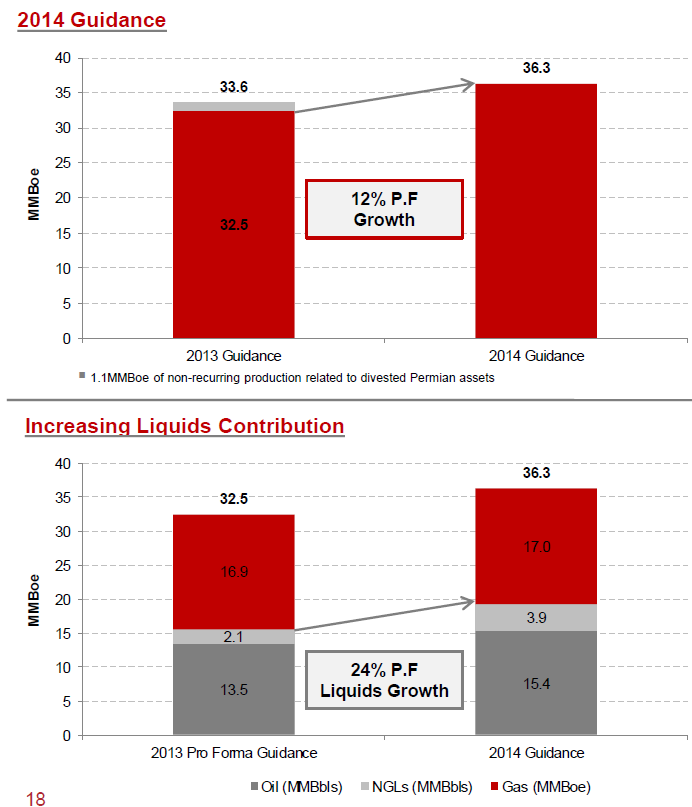

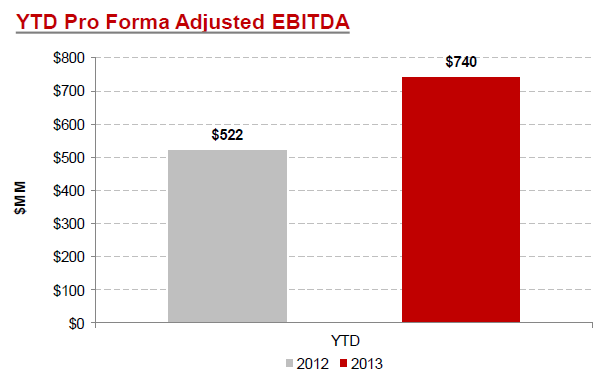

Resulting from the improvement in technology and execution, production growth in the Mississippian grew by 1% sequentially despite a rig count that was 15% lower than the 2nd quarter and 30% lower than the 1st. The company is projecting Mississippian production growth at the rate of 35-50% in liquids for 2014. Year to date 2013 versus 2012, SD has drilled 69 more wells in the Mississippian for $27MM less dollars. If you back out the sale of the Permian asset earlier in the year, which contributed about $50MM of EBITDA in 2012, EBITDA grew roughly 20% from 2012-2013. Looking forward to 2013, the midpoint of the guidance would yield 12% organic production growth and 24% liquids growth. Assuming $95 crude oil and $4 natural gas would yield about $1.075 billion of EBITDA, which would represent about 19% organic EBITDA growth over 2013 guidance.

(Click to enlarge)

(Click to enlarge)

Source SD 3rd Quarter Earnings Presentation

Based on 483.582MM shares outstanding and a recent price of $5.62, SD has a market capitalization of roughly $2.2718 billion. As of 9/30/13, the company had $920.257MM of cash and equivalents on the balance sheet, which is offset against $3.195 billion of long-term debt. This equates to an enterprise value of approximately $5 billion. This means that the company is trading just below 5 times EV/EBITDA for the forward year, which is quite cheap. Based on SandRidge's easy to realize growth footprint over the next several years, the stock should either rise or the valuation would have to go down, because EBITDA should increase in any stable pricing environment. In 3 to 4 years, it isn't hard to imagine $1.40-$1.5 billion of EBITDA generate, which could push the stock to $7.50-$10.00 per share.

SandRidge has some marketable assets in its Gulf of Mexico properties, which is uses currently to produce the free cash flow to finance growth. In addition, as the company further develops its core Mississippian region where it owns a great deal of land, there should be opportunities for partial sales of non-core acreage. Lastly, the opportunity does exist to monitor some of the company's infrastructure assets such as the saltwater disposal system into an MLP type asset structure. These options give me confidence that the company should be able to weather just about any storm. For investors that wish to play the stock more conservatively than just buying it outright, selling a put might not be a bad idea. The $5 puts expiring in January 2015 are going for about $0.78 per contract. This equates to an 18.5% return on the maximum risk of $4.22 assuming the stock's price is above $5 at expiration. Your worst case scenario would be that you could own the stock at a breakeven of $4.22, with the opportunity to double over the next several years.

Disclosure: I am long SD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1880031-sandridges-transformation-sets-the-stage-for-future-stock-appreciation?source=feed

Aucun commentaire:

Enregistrer un commentaire