ROYT is an oily trust that trades at a significant premium compared to other trusts when measured by trailing yield. Is it worth the price?

As part of a recent portfolio update, I conducted a deep technical evaluation of a set of oil and gas trusts. I took a hard look at the numbers, reviewed years of SEC filings, and built an engineering-style model to forecast trusts' future distributions based on individually tailored forecasts of production, prices, and expenses. This article discusses the fourth trust that I reviewed, Pacific Coast Oil Trust (ROYT).

A summary of the fair value for ROYT for various rates of return and risk is provided at bottom. The text of the article discusses the model and key assumptions. Comments, challenging questions, and discussion is encouraged.

A General Model of an Oil and Gas Trust

Oil and gas trusts are a type of commodity investment in which an investor purchases the right to future net profits from a set of wells. ROYT was created by the Pacific Coast Energy Company (PCEC), a subsidiary of BreitBurn Energy Partners (BBEP), to own profits from the "sale of oil and natural gas production from... properties... in the Santa Maria and Los Angeles Basins [of California]." (Source: ROYT Prospectus, p1.)

For an investor, ROYT's value, as that of all trusts, is based on the NPV of its distribution stream. Although other methods, such as trailing yield and proven reserves, are sometimes used to compare trusts, these other methods are poor proxies for the distribution stream because they ignore critical considerations, such as the cost to extract resources, uncertainty related to extraction economics, and the reality that trusts have no influence over capital investment. However, these factors may be considered directly through the development of a bottom-up model of a trust's accounting.

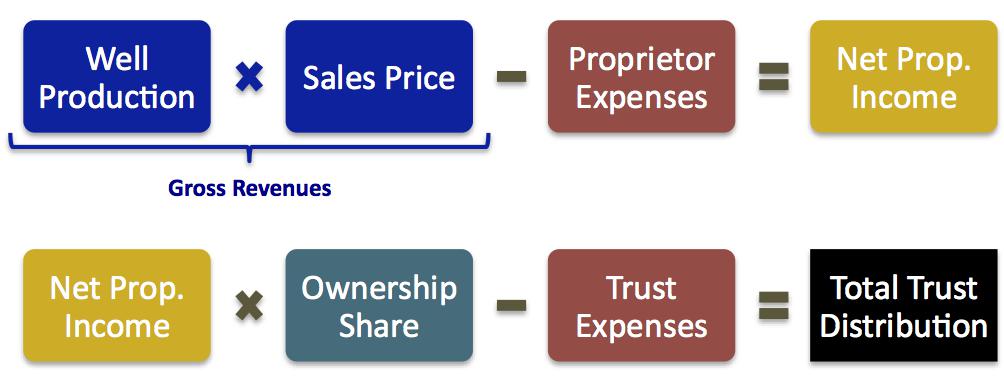

Generally speaking, a trust's distributions are determined in a two-step process (shown below). First, the proprietor calculates the overall net property income by subtracting production and sales-related expenses from the underlying properties' gross revenues. Then, the trust administration determines the total distribution by subtracting their expenses from the trust's share of the net property income.

(click to enlarge)

Although trusts typically report only historical performance, forecasts may be developed for future well production, sales, and expenses (and, therefore, the resulting distributions) through a careful reading of a trust's SEC filings and some number crunching.

Of course, in the case of trusts, the devil is in the details. As discussed in my earlier article, "Tricks that Inflate the Value of Oil and Gas Trusts," trusts and well proprietors use a number of accounting and contractual techniques to manipulate net income and, indirectly, the distribution. These tricks can mislead the investor, so it is wise to be aware of them when investing in trusts. To account for these details, the generalized model must be modified significantly to estimate a specific trust's distributions. The rest of this article discusses these modifications as made for ROYT.

ROYT Trust Distribution Model

Well production

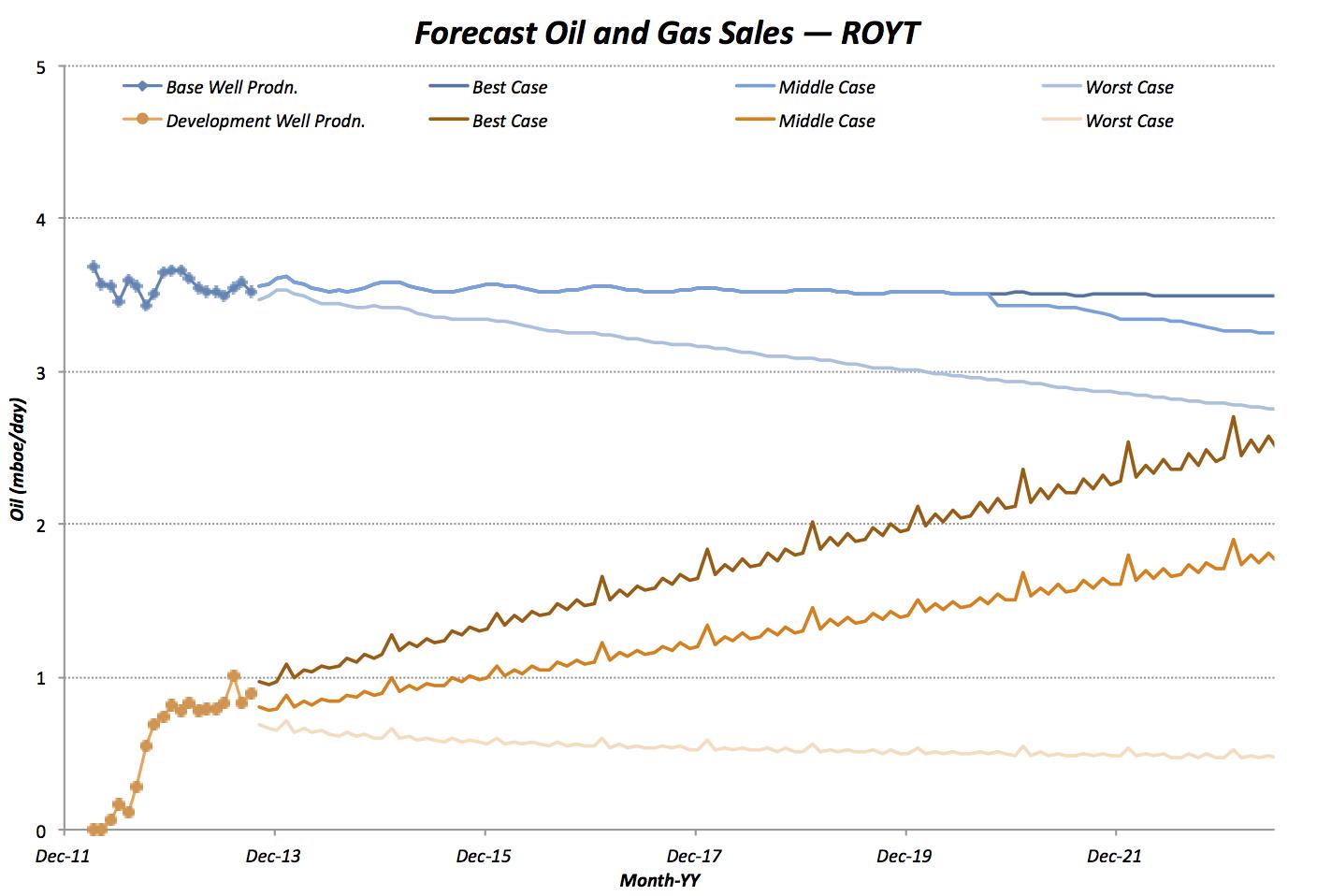

ROYT produces oil from two sets of wells. One set, the "base" wells, was completed and brought into production before the creation of the trust. The second, "development," set represents additional wells brought online through ongoing investment. Moving forward, the number of base wells should remain constant, while the number of development wells should increase. Both sets of wells exhibit remarkably stable production when measured on a per well basis. For example, average decline for the base wells is less than 0.2%/year.

The stability of ROYT's wells is both a boon and a curse for forecasting. Given historical performance, it is possible to generate extremely tight-fitting curves that forecast a near-zero decline in production long into the future. However, common sense suggests that, at some point in time, production will decline at a faster rate. Therefore, for the base wells, I chose to model uncertainty by the date at which production begins to decline. In the best case, production remains stable for a very optimistic 20 years, before declining at 2.5%/year; in the middle case, the decline begins in 7 years; and in the worst case, 0.

For the development wells, forecast uncertainty depends on the number and schedule for new wells. The model assumes that, in the best case, PCEC adds 1 well per month for 200 months; in the middle case, 1 well is added every other month; and in the worst case, no additional wells are added. The chart below shows the actual and forecast production rates for each case and both sets of wells.

(click to enlarge)

Sales Price

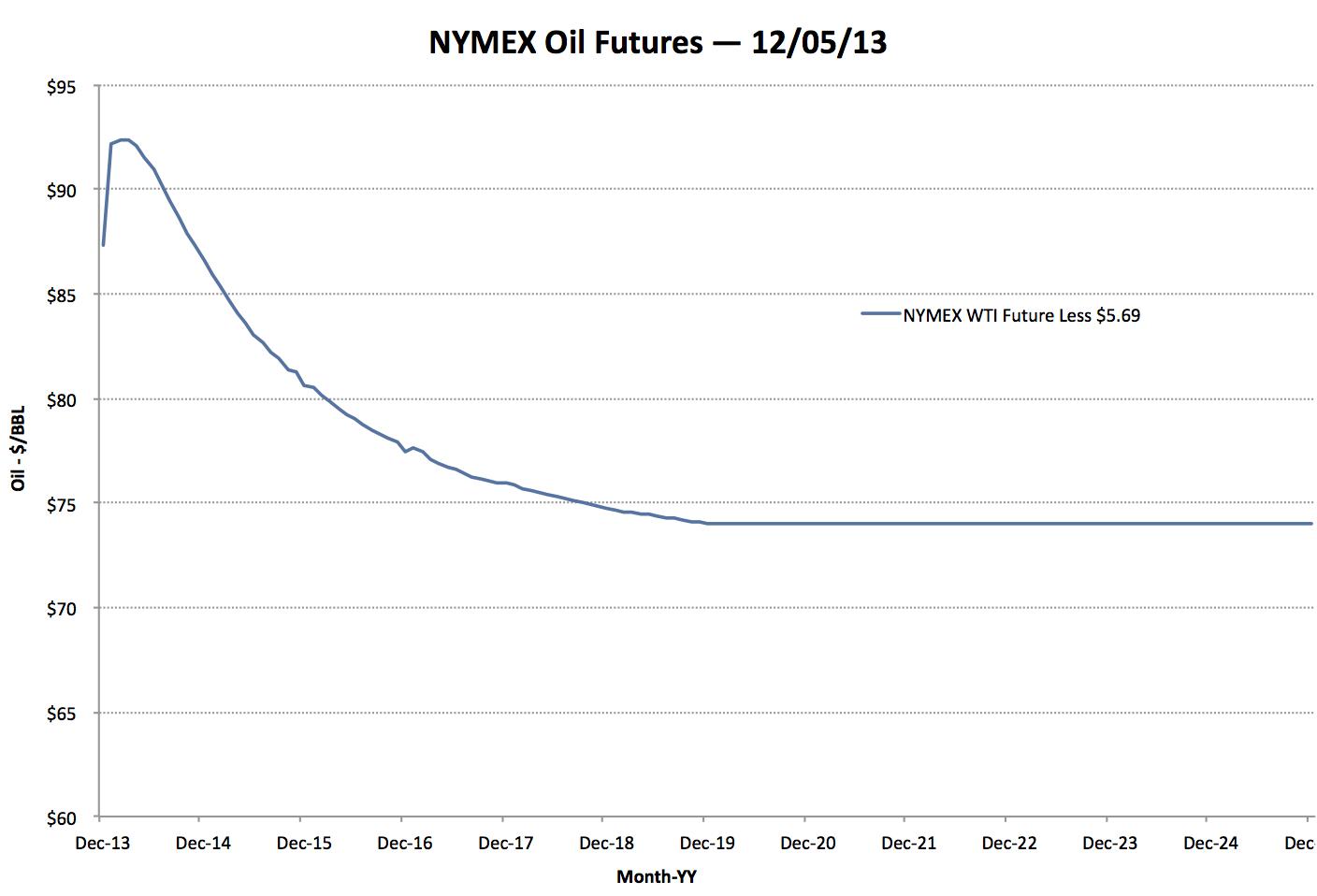

PCEC sells oil (and a very limited amount of gas) through closed contracts with terms that are unavailable to the investor. ROYT's own estimate for reserve value (see prospectus) assumes that sales prices would be $5.69/boe less than NYMEX WTI Light Sweet Crude prices; the model assumes the same. As of 12/05/13, sales prices are assumed to start around $93, before dropping to $74/boe by 2019.

(click to enlarge)

Proprietor Expenses

PCEC deducts a series of categorical expenses from gross revenues before the trust receives its share. The model assumes that these expenses will continue such that:

- "Operating" expenses for the base wells will remain $0

- "Lease" and "Production and Tax" expenses will change in proportion to the volume of oil produced

- "Development" expenses will be incurred at a rate of $365k/mo.(equivalent to the current average) until 2018 and $0 thereafter

- "Overhead" will increase at a rolling rate equal to that of the past 12 months

- PCEC's management fee, which is now $1M/year and set proportional to the CPI, will increase at 2%/year

Trust Expenses

ROYT trust administration deducts a single charge that combines all trust expenses. Over the past 6 quarters, the charge has varied between $41k (Dec. 2012) and $305k (Mar. 2013), with an average of $52k/mo. The model assumes that this charge will be incurred at $52k/mo. moving forward.

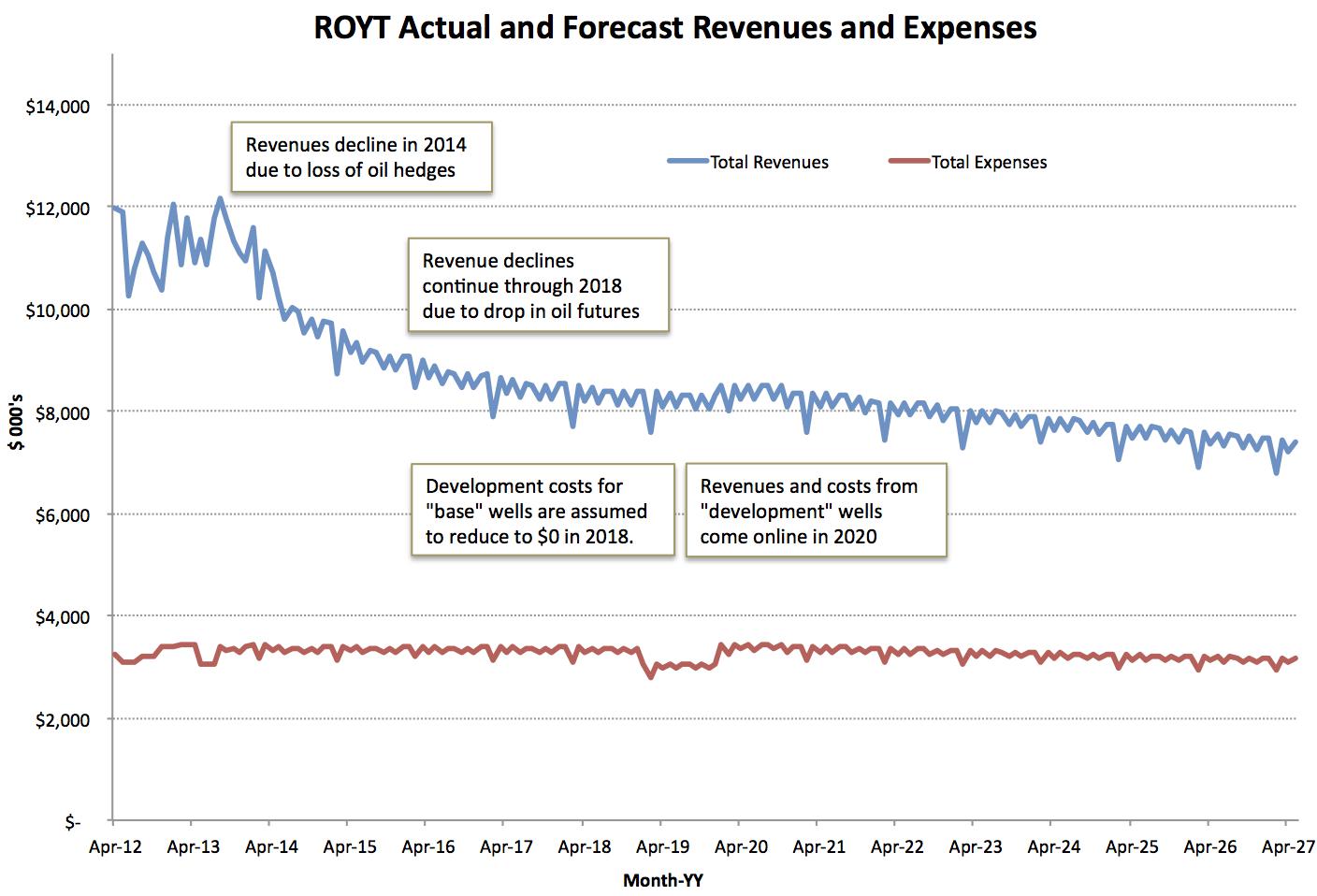

The figure below shows the historical and forecast revenues and expenses for ROYT, assuming the middle case.

(click to enlarge)

Other Assumptions

ROYT currently receives a 7.5% royalty payment for production from the development wells. Once PCEC recuperates its development costs for these wells, this payment will increase to a 25% net royalty. PCEC guidance estimates that the conversion may happen "around 2020;" the model assumes a date of Dec. 31st, 2019.

ROYT also has rights to the proceeds from hedging contracts that amount to 2k boe/day at $115/boe through March 2014. Due to ROYT's reporting schedule, some hedging revenue may be reported as part of the Q2 2014 SEC filing.

Lastly, while ROYT has no set dissolution date, it does have several dissolution conditions. The model forecasts distributions until such a date when one of the conditions is met and then assumes that the trust's remaining interests are sold with proceeds going to trust unit holders. With stable production, this date is far in the future, and the NPV of the residual has only nominal value.

ROYT Valuation

So what's ROYT worth? The NPV of ROYT's future distributions, as estimated by the model, for the best, middle, and worst cases, and for various rates of return, is summarized below:

(click to enlarge)

As I read the table, it suggests that the NPV is highly dependent on an investor's desired rate of return and that the current market valuation of ROYT ($13.73, as I write this), assumes that production will follow the middle case with an appropriate rate of return of under 8%.

For my personal investment, I would prefer a minimum of 8% return on the middle case (or 10%+ on the best case), which would value ROYT between $12.39 and $13.34. Noting that the current market valuation is only slightly higher, it suggests that ROYT is relatively fairly valued and that could be a terrific play for those who believe that oil price futures after March 2014 will rise.

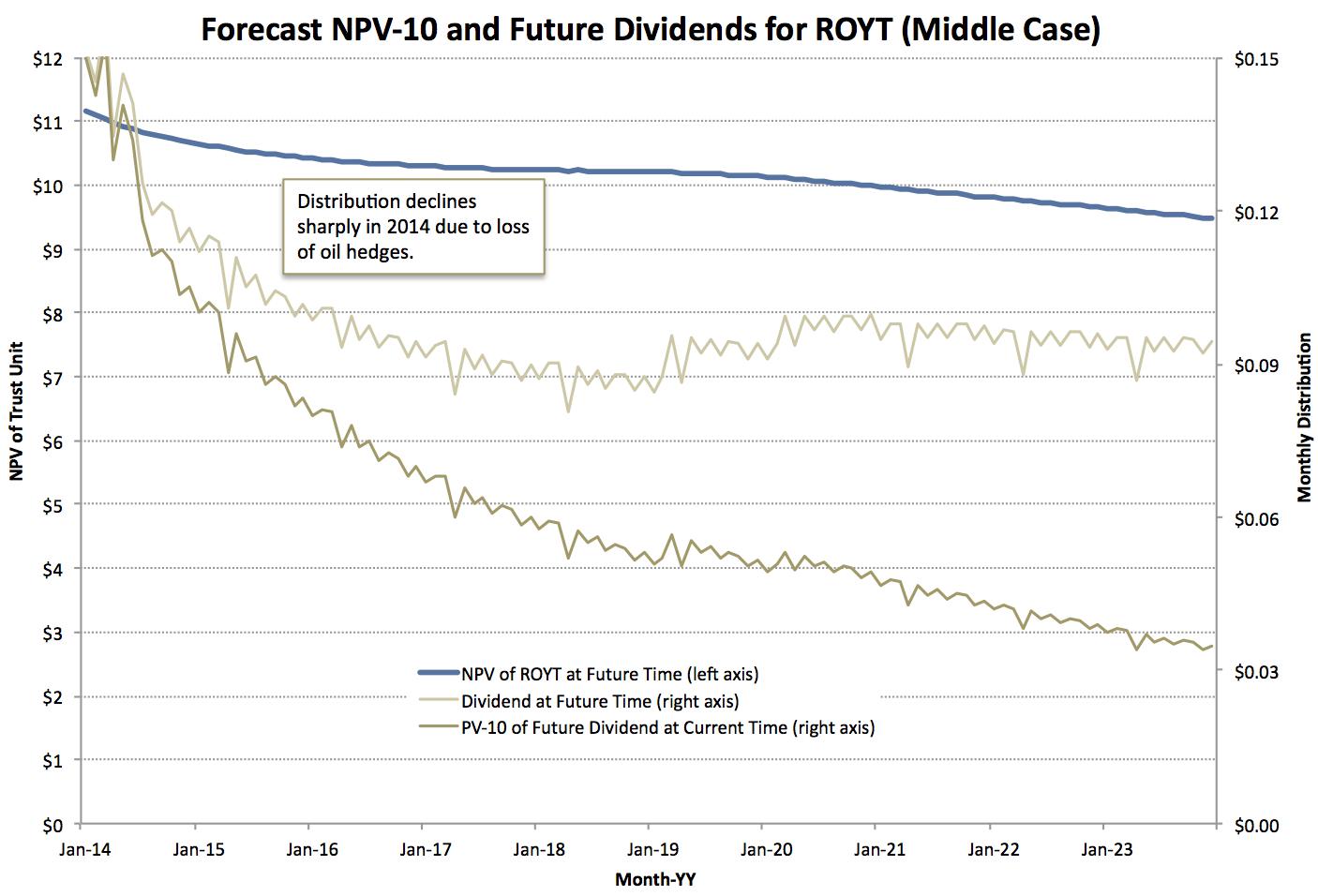

The chart below shows the forecast dividend for ROYT through 2014, assuming the middle case. Although the actual distributions will deviate from these estimates, the chart should give a hint of what the structure of the distribution will look like over time. Interested investors should note that the distribution is set to drop significantly in 2014 as the oil hedges expire. While the effect on NPV will be minimal due to the long life of the wells, it is likely that some current investors may see the drop in distribution as a sign of weakness and sell their units. This, in turn, may create a buying opportunity. Given that the current price seems fairly valued, I plan to wait for that opportunity before taking a position.

(click to enlarge)

Comparing ROYT's valuation to other trusts

ROYT is the fourth trust evaluated by the model and ROYT's results can be compared to those of the other trusts to provide a relative valuation. Other trusts that have been evaluated include:

- Enduro Royalty Trust (NDRO) (Forecast as of 11/12/13)

- ECA Marcellus Trust I (ECT) (Forecast as of 11/19/13)

- Hugoton Royalty Trust (HGT) (Forecast as of 11/25/13)

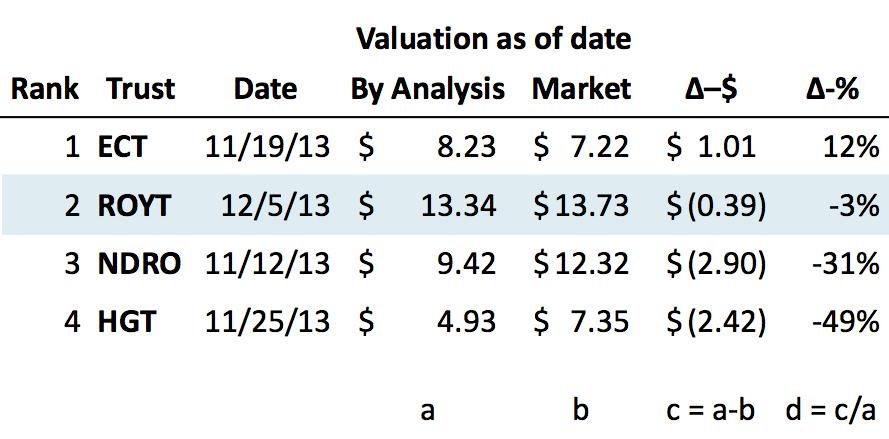

The table below shows a ranking of trusts based on the difference between the model NPV and the market price at the time of evaluation. For ROYT, the difference is -3%, which places it in second place.

(click to enlarge) In addition to the trusts mentioned above, investors wishing to do their own comparative analysis may wish to compare ROYT against:

In addition to the trusts mentioned above, investors wishing to do their own comparative analysis may wish to compare ROYT against:

- Chesapeake Granite Wash Trust (CHKR)

- Mesa Royalty Trust (MTR)

- MV Oil Trust (MVO)

- Permian Basin Royalty Trust (PBT)

- SandRidge Permian Trust (PER)

- SandRidge Mississippian Trust II (SDR)

- SandRidge Mississippian Trust I (SDT)

- Whiting USA Trust I (WHX)

- Whiting USA Trust II (WHZ)

Disclosure: I am long ECT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1883781-pacific-coast-oil-trust-a-forecast-of-future-distributions?source=feed

Aucun commentaire:

Enregistrer un commentaire