Gold is beautiful. Not everybody thinks so, but generations upon generations of human beings have felt this way, and many still do today.

Gold ought to be money. Most people don't think so, but generations upon generations thought of it like this, and some still do today.

Is there anything that everybody can agree on -- past, present, and future -- when it comes to gold? There should be one: gold is a commodity. Silver is, too, by the way.

Whether gold is designated as money or not and whether it is seen as beautiful or not are relatively subjective determinations. A society could, by evolutionary accretions or by fiat, dismiss gold's monetary role, either wisely or foolishly. That is a monetary question.

A society could start to see gold as no more alluring than schist. That is an aesthetic judgment. Neither aesthetic nor monetary questions ought to be beyond debate.

But, the commodity-ness of gold (GLD) and silver (SLV) should be a relatively settled question. Of course, our understanding on the meaning and significance of the term "commodity" might change in the future, leaving gold and silver to be designated by more appropriate categories at some point. Like copper, tin, aluminum, platinum, iron, nickel, and lead, however, gold and silver appear on the periodic table, and I think that as physical objects, insofar as we can strip them of our more subjective designations, these two precious metals will continue to fall within the category of "commodities" for some time to come.

A gold bug should not find this objectionable. Gold's commodity-ness is precisely why it will likely always have a default monetary role in the unstable dynamics of our peculiar species.

But, in a world in which gold has been stripped of its monetary designation and become another tradable good, the question has to be asked, should we expect gold's price behavior to be the inverse of the new monetary standard, or will it trade as if it were another commodity?

GOLD AS SHADOW CURRENCY

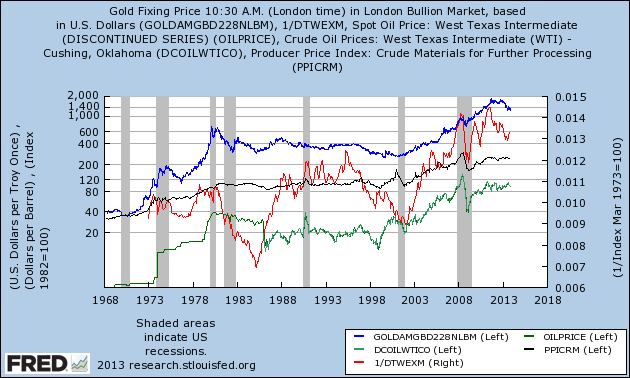

There are plenty of people who argue that gold should or does trade inversely to "the dollar." It is not always easy to tell what they mean by this.

Sometimes, they mean that it trades inversely to the dollar index (UUPT). That means, gold moves with foreign currencies, which are managed more responsibly than the dollar is. Allegedly.

(Click to enlarge)

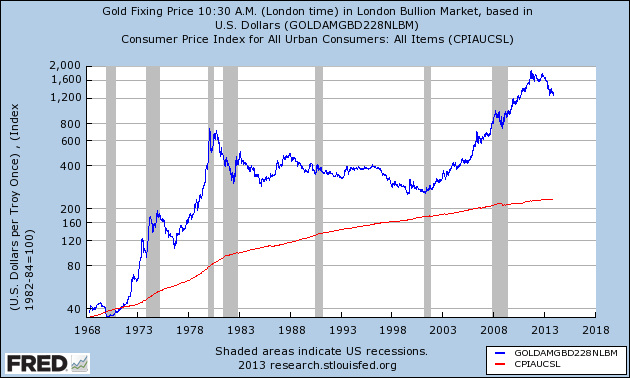

Sometimes, they mean that it should be traded inversely with the level of CPI. That is, the purchasing power of the dollar is being constantly corroded, and therefore, because gold is a shadow currency, it ought to rise with consumer prices.

(Click to enlarge)

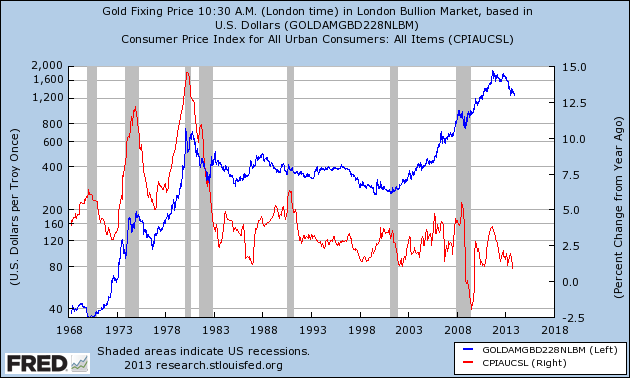

Sometimes, the gold-as-shadow-currency crowd suggests that it should move with the rate of change of CPI, that is, with inflation. Gold should move up when inflation rises, but down when inflation falls.

(Click to enlarge)

Or, they might stretch this out to argue that gold "forecasts" inflation rather than reacting passively to it.

Even those who are not gold bugs assume these points of view. For example, when people who are dismissive of gold claim that the jump in gold and silver in 2011 were 'predicting' inflation that never came, they implicitly share the assumption that the movements in the price of gold are driven by this shadow-currency function.

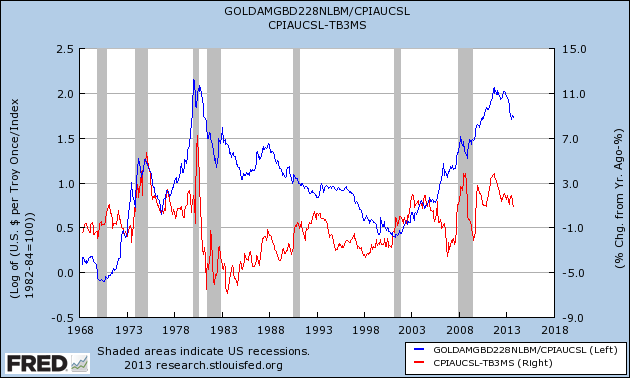

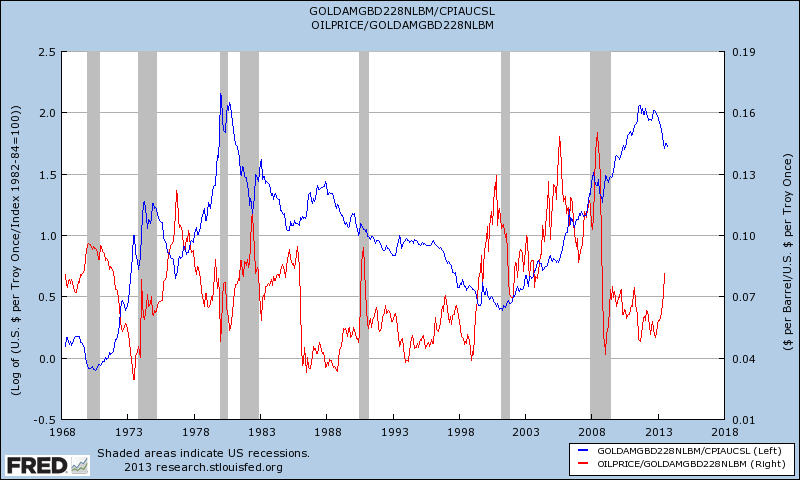

The most sophisticated variation of this argument is that the price of gold is an inverse function of real interest rates (IPE).

(Click to enlarge)

So, gold-as-shadow-currency theorists have plenty of options to choose from when shopping for a model of gold prices. The alternative perspective to the gold-as-currency school is more primal, the idea of gold-as-commodity. From that perspective, gold and silver would be expected to trade in patterns similar to other commodities. Which one wins?

GOLD AS HYPER-COMMODITY

Over the last forty years, gold has been more highly correlated with other commodities than it has been with the smorgasbord of dollar measurements.

| Correlations (1970-2013) | Gold (nominal) | Gold (real) |

| CPI (absolute level) | 0.70 | 0.21 |

| Inflation | -0.29 | 0.24 |

| Dollar index (inverse) | 0.62 | 0.32 |

| Real 3-month (inverse) | 0.32 | 0.28 |

| PPI-crude mat (nominal) | 0.87 | 0.52 |

| PPI-crude mat (real) | 0.19 | 0.52 |

| WTI (nominal) | 0.88 | 0.62 |

| WTI (real) | 0.65 | 0.77 |

That doesn't mean there isn't something very interesting going on in gold and silver, but that very interesting something can only be seen if one first accepts that gold and silver are commodities.

And, that very interesting something is that gold and silver trade more like commodities than commodities do. That is, if commodities generally go up 10% (not on any given day or month, but over the course of quarters and years), gold and silver might be expected to rise 15% or 25%. If the broad class of commodities drop 20%, precious metals might be expected to drop 35%. Or whatever number you like. The important thing is, over time, moves in the commodity markets are exaggerated in the precious metals markets.

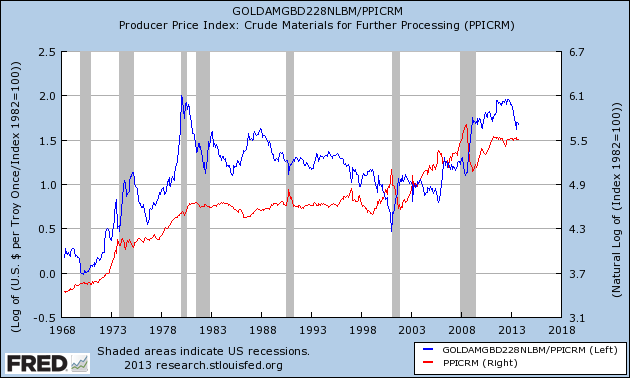

As you can see in the chart below, the ratio of gold to raw material prices (PPICRM) behaves like raw material prices themselves. Gold and silver have become hyper-commodities.

(Click to enlarge)

I think that is interesting enough. What makes it more interesting is that silver did not have this hyper-commodity characteristic before Nixon closed the gold window in the early 1970s. Silver was demonetized after the Civil War, so we have a good century and a half of data to look at, and prior to the 1970s, silver did not exhibit the hyper-commodity behavior that it has shown since.

Gold, of course, was not freely traded before the 1970s, so we cannot really do a before-and-after in the same way.

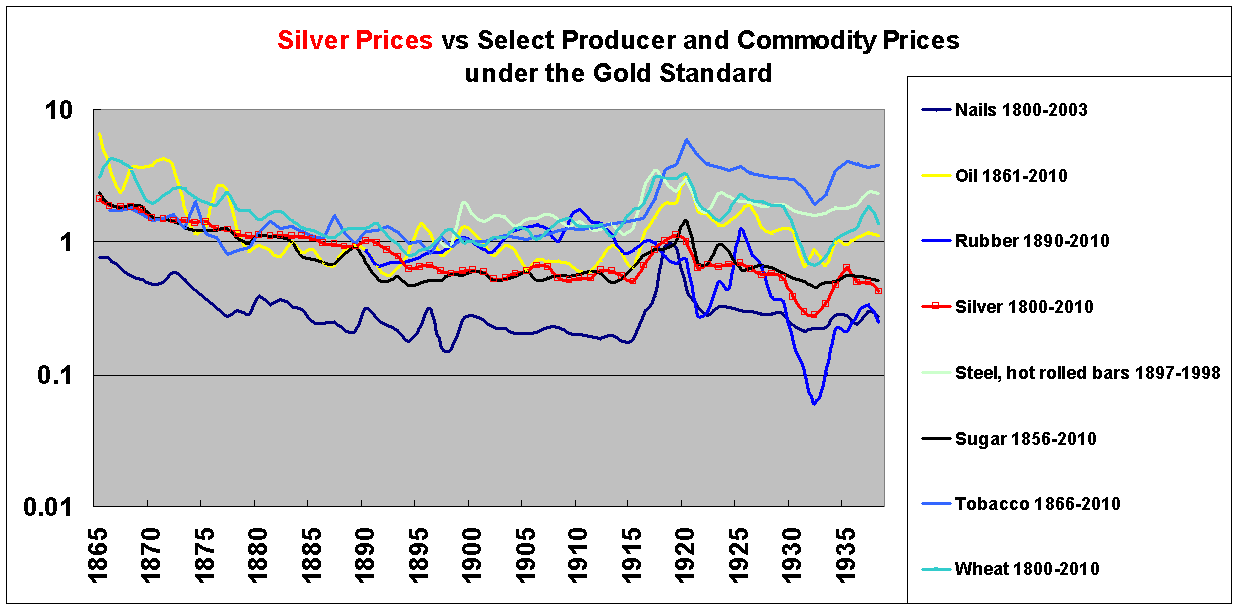

SILVER PRICES UNDER THE GOLD STANDARD

But, the fact that silver was correlated with other commodities during the global gold standard, when exchange rates would have been much more stable than they are under our fiat monetary system, should rule out the notion that precious metals, when freely traded, are priced inversely to foreign exchange rates. A generalized weakening of the currency will certainly raise the price floor of precious metals as it would with most goods and services, but it does not determine the price of gold or silver.

(Click to enlarge)

The point I am trying to make is that there are some intriguing things about gold and silver behavior in the post-Bretton Woods world, but nothing that suggests meaningful levels of manipulation. The argument for outright manipulation can only come from the ideological insistence that because gold must always be money, it must somehow trade inversely to some measure of the dollar, and where it does not do so, it is a breakdown in the markets rather than a breakdown in the underlying theory and assumptions.

Is there a way to reconcile the theme of manipulation with the observation that precious metals trade more or less as commodities? Perhaps. Perhaps the entire commodity sector is manipulated. Perhaps the manipulators camouflage their manipulation by making it appear as if gold and silver trade with other commodities. Perhaps their manipulation is so intermittent that it cannot be observed beyond very short periods.

Perhaps. But, where on earth does all this sleuth-work lead?

It makes one neither more sane nor more profitable. If gold and silver are being manipulated so as to shadow all of the other commodities in the world, my general advice is to take that into account in your trading, whether you think it is fair or sustainable or not.

I became interested in gold and silver because of my doubts about the sustainability of fiat currencies in the wake of the crisis and my suspicions with respect to long-term distortions caused by central banking. But, I have to be alive to the notion that that ideological predisposition does not do much to explain the behavior of gold and silver throughout the 1980s and 1990s, and that if I had been around to trade gold and silver on my ideological preferences in those days, I would have lost my shirt, pants, and shoes in the process.

The only way I could have made any money after that would be selling newsletters decrying market manipulation and ripping into whoever was at the Fed for being a shill or a fool.

CYCLICAL SHOCKS, COMMODITY BOOMS, AND PRECIOUS METALS

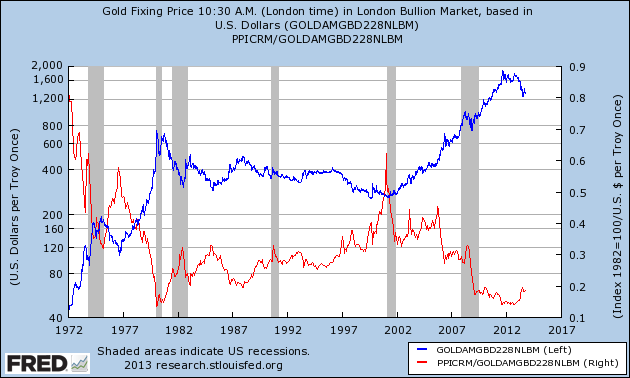

The history of the last forty years suggests that cyclical shocks to commodity booms are traumatic events that tend to have a secular impact on the future behavior of commodities, and this is most strongly felt in the precious metals. Depending on how you want to count these episodes, we have had two or three of these types of events, in 1980, 2008-2010, and perhaps 1973-1974. Cyclical shocks are as mean to commodity markets as they are to the wider economy, perhaps even more so.

(Click to enlarge)

Prior to my historical research over the course of the last twelve months, I suspected that the "new normal" would look more like the mid-1970s than the 1980s. I suspected precious metals would sharply "correct" and then revert back to the commodity boom theme as they did up until 1980.

Indeed, there was a correction in gold and silver, as with all commodities, and the commodity sector (DBC) did then resuscitate, especially precious metals and agriculture (DBA) -- recall that the first gales of the Arab Spring coincided with a ruthless rise in food and textile prices -- only to cavitate from the spring of 2011 onward.

(Click to enlarge)

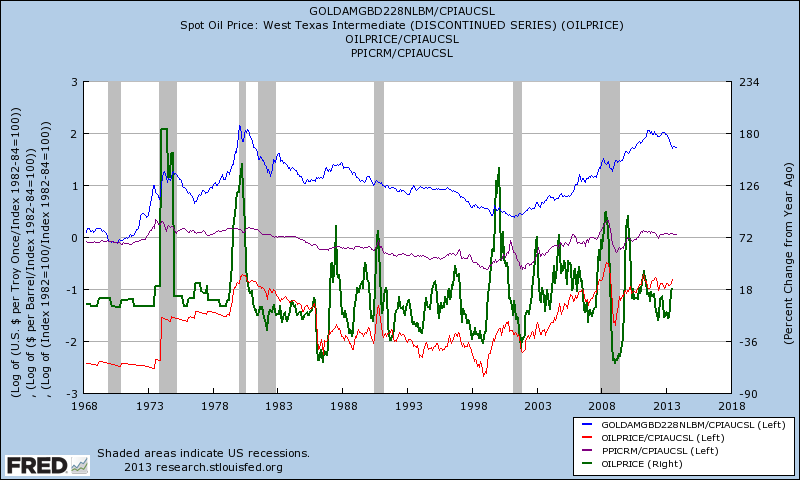

This points, however, to another notable way in which precious metals differ from the wider sector: gold and silver shine brightest before night falls in commodity markets. Over the last forty years, gold and silver react more violently to bull and bear markets than do the broader commodity markets, but gold and silver also tend to be a bit late to the party, especially relative to energy.

(Click to enlarge)

In the mid-1970s, gold corrected sharply, but oil did not flinch. In the 1980s, precious metals went parabolic, right before the beginning of a twenty-year bear market. In the late 1990s, oil and other commodities were beginning their upward march while gold was still bottoming. Gold was the last to know that there was a commodity boom on. In 2011, as in 1980, precious metals went parabolic right before keeling over, and now we have the first year of negative returns in gold and silver.

(Click to enlarge)

Perhaps that fits into some sort of manipulation narrative but none that I have ever heard of.

The best thing to do is to stick with simple facts, and then one can speculate and elaborate on those facts, as long as the fundamentals are not abandoned. In this case, the fundamental facts are that gold and silver are, first and foremost, commodities, and that is how they trade. Once those facts are acknowledged, there is room to talk about how gold and silver differ from other elements of the sector and what that might mean.

THE CURRENT OUTLOOK

Everything about this market suggests that we are in a bear market in commodities:

1. They have not recovered from the cyclical "shock" of 2008-2010.

2. Oil has weak legs.

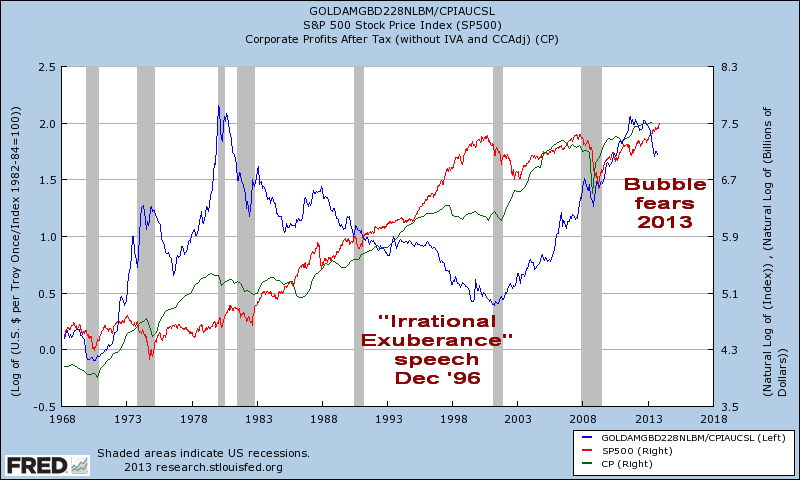

3. Anytime there is rampant speculation about a stock market bubble, stay clear of precious metals.

Point three might be surprising, but anytime there is talk about stock bubbles (SPY,DIA), precious metals suffer! Talk about "irrational exuberance" in the mid-1990s was a fair signal that there was very little money to be made in commodities, especially precious metals. And, there was plenty of time to wait for oil and other commodities to rise and for the stock market to crash before jumping into the gold market.

(Click to enlarge)

If one thinks on the inner dialogue within Mr. Market's head over the last year, the speculation about a stock market bubble has coincided quite well with the sharpest falls in gold and silver.

There is, of course, nothing to say that this sort of arrangement will continue to exist in the future. That is fair enough. I am open to any other set of plausible predictors of gold and silver prices. Real interest rates do not work. Inflation does not work. The dollar does not work. Asian demand does not work. Painting ideological opponents as hooligans does not work.

Maybe it's time to look at the facts and set ideology aside when it comes to how much rocks cost. My ideological prejudices continue to be those of a gold bug, but one does have to recall that we are talking about inanimate matter here. What really matters is what function it plays in the longer-term dynamics of human progress, and history is a good place to begin to understand that.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1871031-gold-and-silver-no-more-manipulation?source=feed

Aucun commentaire:

Enregistrer un commentaire