Novartis (NVS) is a Swiss multinational pharmaceutical company, ranking among the largest companies among the worldwide industry by sales. Currently, it offers a dividend yield of 3.2%, which is below the yields offered by some of its closest peers but is still interesting for income investors. Novartis has a market capitalization of about $191 billion, and is traded on the New York Stock Exchange as American Depositary Shares [ADS]

Company Overview

In 1996, Ciba-Geigy merged with Sandoz, with the pharmaceutical and agrochemical divisions of both companies staying together to form Novartis. Other businesses were sold-off or like Ciba Specialty Chemicals were spun-off as independent companies. The Sandoz brand disappeared for 3 years, but was revived in 2003 when Novartis consolidated its generic drugs business into a single subsidiary. Novartis divested its agrochemical and genetically modified crops business in 2000,with the spin-off of Syngenta (SYT). Currently, Novartis provides healthcare solutions that address the evolving needs of patients and societies. Focused solely on healthcare, the company offers a diversified portfolio of innovative medicines, eye care products, cost-saving generic pharmaceuticals, consumer health products, preventive vaccines and diagnostic tools. Novartis is also a major shareholder of Roche (OTCQX:RHHBY), a Swiss pharma competitor, owning about 33% of its voting shares.

Novartis' businesses are divided into five operating divisions: Pharmaceuticals, Alcon (eye care), Vaccines and Diagnostics, Sandoz (generics), and Consumer Health (divided into two divisions: Over-the-Counter and Animal Health). In 2012, pharmaceuticals was Novartis' largest division, accounting for 57% of its sales. Alcon generated 18% of the company's sales, followed by Sandoz with a 15% weight. Vaccines and Diagnostics and Consumer Health are smaller segments, accounting together for only 10% of Novartis' sales. Geographically, Novartis has a very good diversification given that its sales are spread worldwide. Europe is the company's largest market accounting for about 35% of sales, followed by the U.S. with a weight of 33%. Asia, Africa, and Australasia account for 23%, and the remaining 9% is generated in Canada and Latin America.

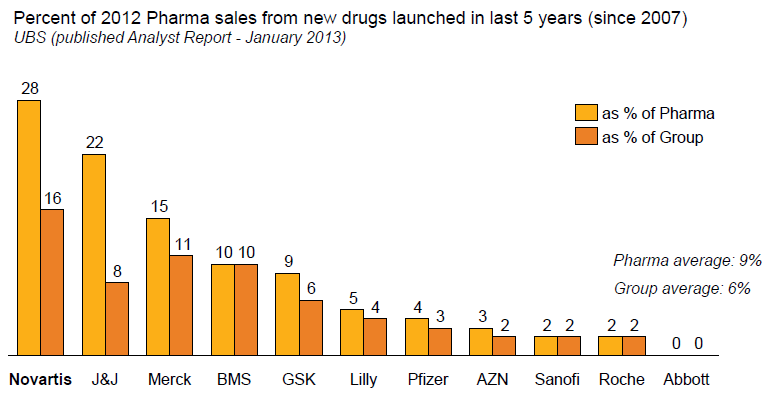

One of the key issues facing the pharmaceutical industry right now is the high number of patent expirations until 2015, which is affecting most companies in the sector. This impacts negatively the companies revenue growth, earnings, and ultimately its ability to pay dividends. Novartis has a diversified product portfolio, which helps to address the patent expiration issue. Its three largest products account for 20% of its sales, and its largest product (Glivec) is responsible for only 8% of the group's sales. However, Novartis lost in 2012 the patent for Diovan in key markets leading to an annual drop of 22% in sales, showing that is not completely immune to this issue. Glivec will also lose its patent in the U.S. in 2015 and other key market by end-2016, which will certainly lead to lower sales over the medium term. On the other hand, Novartis had a highly successful period of new drug launches between 2007-10 and continue to rejuvenate its product portfolio, having achieved 11 major regulatory approvals during 2012. Novartis has a higher weight in sales of new drugs launched in the last five years compared to its closest peers, which places the company in a better place to face patent expirations than the majority of its competitors.

(click to enlarge)

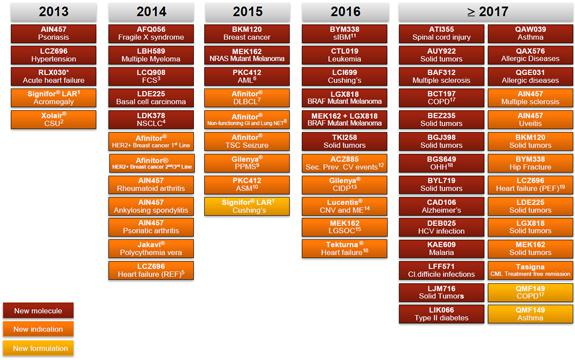

Novartis has a leading new product pipeline with more than 200 projects in clinical development, including 138 in the Pharmaceuticals Division. In 2012, Novartis research & development expenditures were 21% of its sales, reflecting its huge efforts to bring new drugs to the market. The company has a substantial number of potential product approvals and late-stage clinical trial read-outs over the coming 24 months as shown in the next graph, which if they are approved will certainly give a boost to Novartis' top-line growth.

(click to enlarge)

In 2012, Novartis generated almost $57 billion in sales, a decrease of 3% from the previous year. Without the currency effect, sales were flat compared to 2011. Recently launched products accounted for $16.3 billion or 29% of Novartis' sales, up from 25% in 2011. Its EBIYDA was above $20 billion, reaching an EBITDA margin above 35%. Operating income stood at $11.5 billion, an increase of 4.6% leading to an operating margin above 20%. Its net profit was $9.6 billion, or $3.93 per share. During the first nine months of 2013, Novartis' net sales increased by 4% to $42.8 billion compared to the same period of 2012. Its earnings-per-share also increased by 4% to $2.92.

Going forward, the company's strategy is based on the diversification of its healthcare portfolio, accelerating growth with new launches, a greater presence in emerging growth markets, and enhancing productivity through efficiency initiatives. Novartis' productivity improvements are targeted to be equivalent to 3-4% of sales per year in 2014 and 2015, improving its profitability even further. The company is also reviewing its portfolio and may perform some divestitures over the next few years focusing its business on pharma, eye care, and generics. Indeed, Novartis recently signed an agreement to sell its blood transfusion diagnostics unit to Grifols (GRFS) for $1.7 billion. Sales in this unit were only $565 million in 2012, so its weight within the group is relatively small. This may be the first of several announcements related to the allocation of capital at Novartis, which is supportive for its shareholder remuneration policy as it raises cash which should be returned to shareholders through dividends or share buybacks.

Dividends

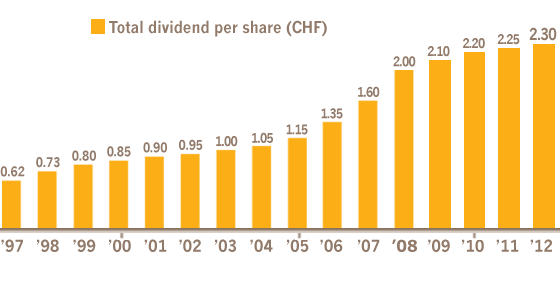

Regarding Novartis' dividend, the company has a very good history given that in 2012 it delivered the 16th consecutive annual dividend increase. This means that since its inception in 1996, Novartis has always raised its annual dividend which is quite impressive. In 2012, Novartis dividend per share was CHF 2.30 ($2.54), an increase of 2.2% from the previous year. The dividend payout ratio was only 58% in 2012, an acceptable level for a stable company like Novartis.

(click to enlarge)

Like many European companies, Novartis pays only one dividend per year. Another negative factor is the Swiss withholding tax, which is currently quite high at 35% and reduces the company's dividend attractiveness. Recently, Novartis announced a share buyback program of $5 billion to be executed during the next two years and also wants to deliver a growing dividend over the coming years.

Novartis is highly cash generative. In 2012, its operating cash flow was above $14 billion, and its capital expenditures were only $2.8 billion. This left plenty of cash to remunerate shareholders, which amounted to $6.2 billion through cash dividends. Therefore, Novartis' free cash flow after dividends was more than $5 billion, which is a huge amount and leads to a very sustainable dividend over the long-term. This good free cash flow generation was applied in the reduction of the company's debt levels. During 2012, Novartis' net debt decreased from $15 billion to only $11.6 billion, representing a low leverage ratio (net debt-to-EBITDA) of 0.58x.

The company's strong cash flow generation and balance sheet is clearly supportive of its shareholder remuneration policy and shows how conservative its management is. As of 30 September, 2013, its net debt was about $11.4 billion or a net debt-to-EBITDA ratio below 0.6x. This low leverage ratio enables Novartis to perform share buybacks and deliver a growing dividend over the next few years, while at the same time maintain its strong credit rating of AA with no intention of exceeding this level.

Conclusion

Novartis does not offer a high-dividend yield, especially after taxes, but it is very safe and has good growth prospects over the coming years. Its good cash flow generation and strong balance sheet leaves plenty of room to increase shareholders remuneration, both from a growing dividend and share buybacks. Novartis is also one of the companies least affected by the patents expiration issue, making it one of the top picks within the global pharmaceutical sector.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1869691-buy-novartis-for-a-safe-and-growing-income?source=feed

Aucun commentaire:

Enregistrer un commentaire