Recently, bitcoin has become a hot topic. The number of news items that cover bitcoin is growing relentlessly. A lot of this attention results from the fact that bitcoin is new, and equally important, pretty difficult to understand. Take the expression 'cryptocurrency' (see Wikipedia) which is already difficult to comprehend. And this is only about its name. Another part of the bitcoin discussion, however, focuses on the question to what extend bitcoin will become a general excepted currency and a credible financial asset for investors. Numerous sources claim that bitcoin could take over the role of gold as a safe haven. Or, that it could become an attractive alternative for the dollar or the euro, given the massive stimulus program of the Fed and the loose ends in the construction of the Eurozone.

A lot of these statements seem to be based on 'qualitative' expectations about future developments. I have thus far seen little work on a quantitative comparison with other, more common, asset classes. Now that bitcoin has left its very early stage of infancy I will try to shed some light on some basic risk and return characteristics of this digital currency. This analysis reveals some interesting aspects about bitcoin.

Meteoric rise

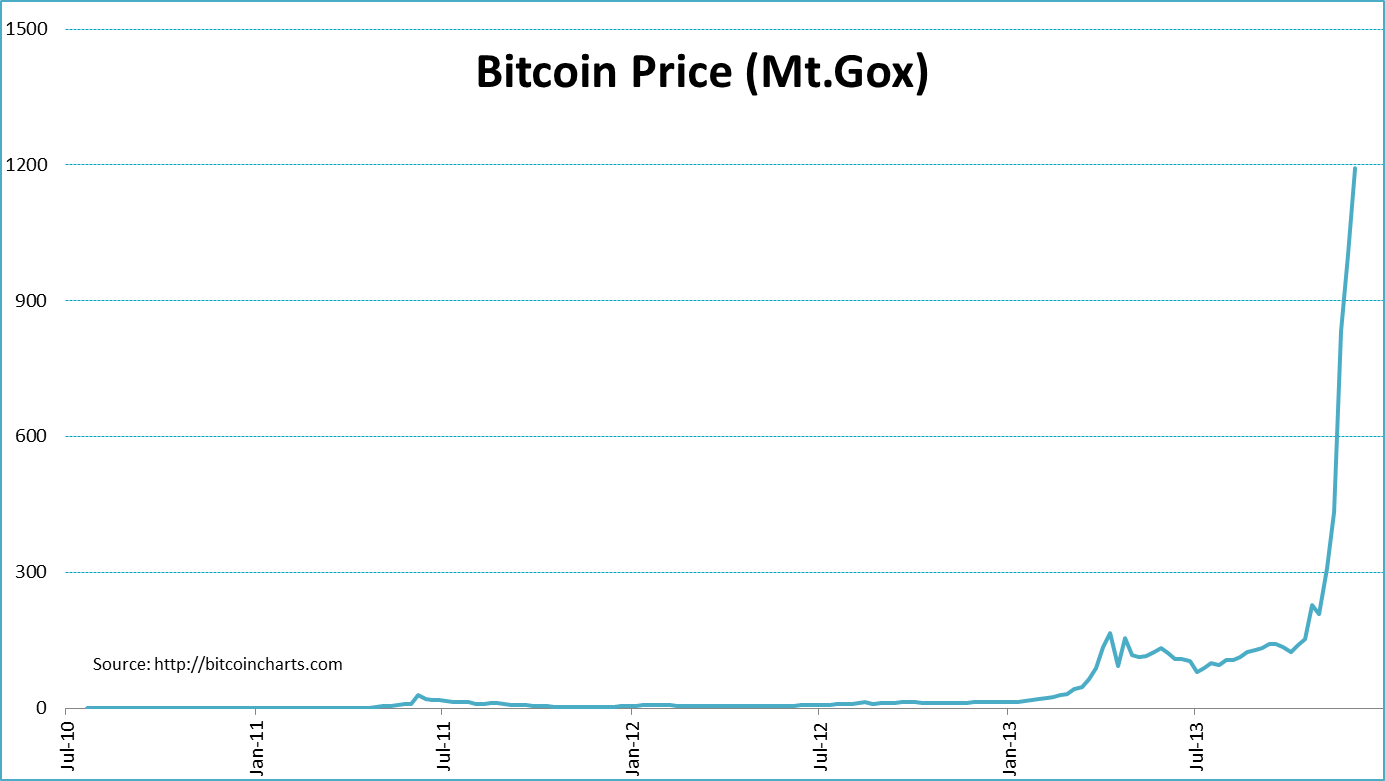

Let's start with a simple graph (see below) showing the price development of bitcoin. The data are from here. I take the data from Mt. Gox, as this website is generally considered as the world's most established Bitcoin exchange. Although simple, the graph already tells a lot. We are not dealing with a regular asset class here. The price of bitcoin has experienced a meteoric rise from USD 0.07 cents in July 2010 to almost USD 1200 (December 4th 2013). Besides perhaps some obscure mining companies that stumbled on a high grade ore, I cannot think of any investment showing this price pattern. Companies like Netflix (NFLX) and Tesla (TSLA), which experienced extraordinary returns recently, can in no way compete with the returns bitcoin has realized.

(click to enlarge)

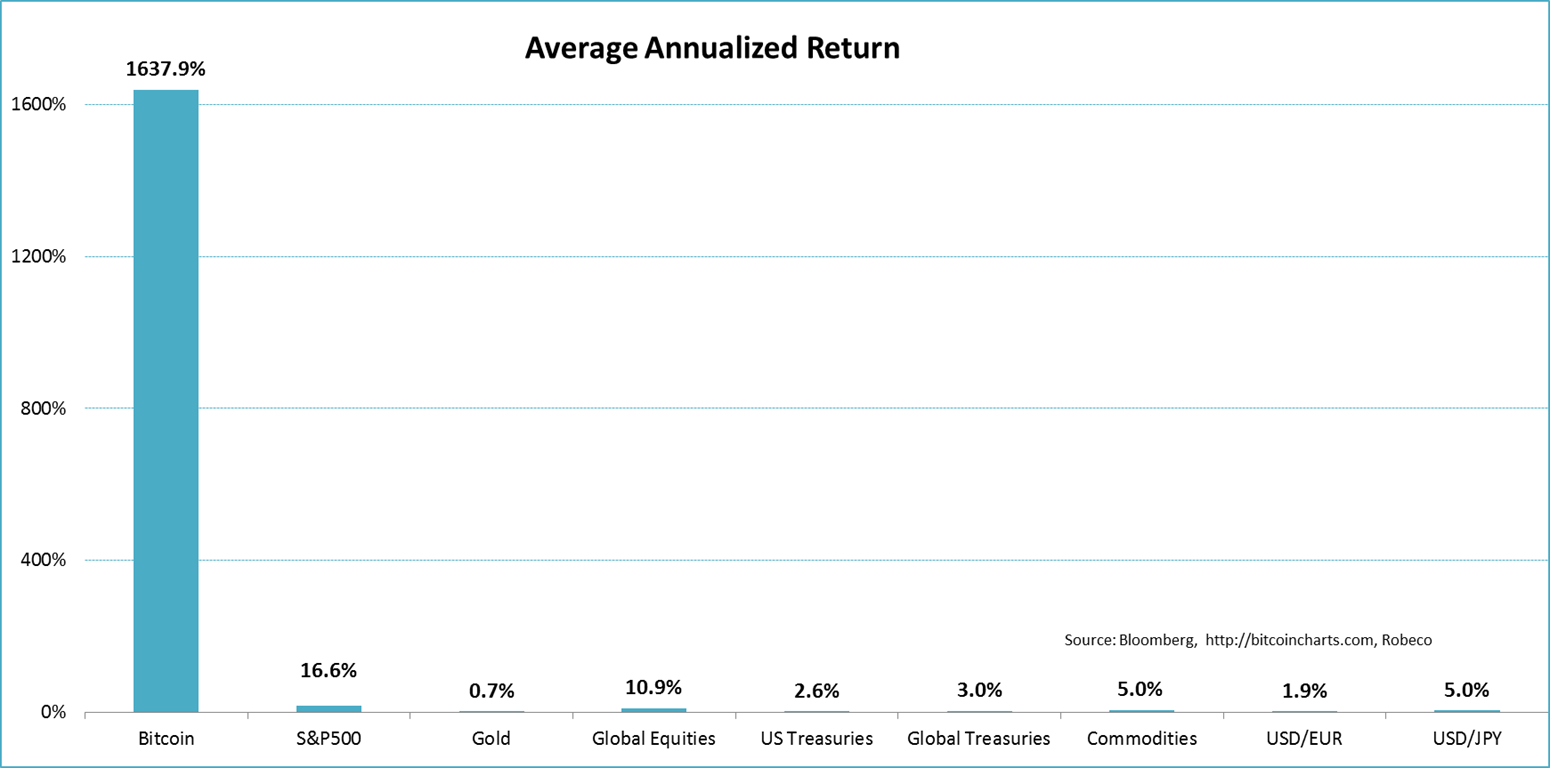

To put things into perspective, the next graph shows the returns of bitcoin and some major asset classes. Again, the incredible rise of bitcoin stands out. On an annualized basis bitcoin has returned more than 1600% since July 2010. This compares to an annualized return for the S&P 500 index (SPY) of almost 17% and just under 11% for global equities (URTH). Other assets like commodities (DBC) and treasuries (GOVT) have risen even 'less'. And gold (GLD)? Over this specific gold period gold has generated almost no return at all (+0.7%). Finally, bitcoin returns are in no way anything like the returns on common currencies like the euro (FXE) and the yen (FXY).

(click to enlarge)

Correlation

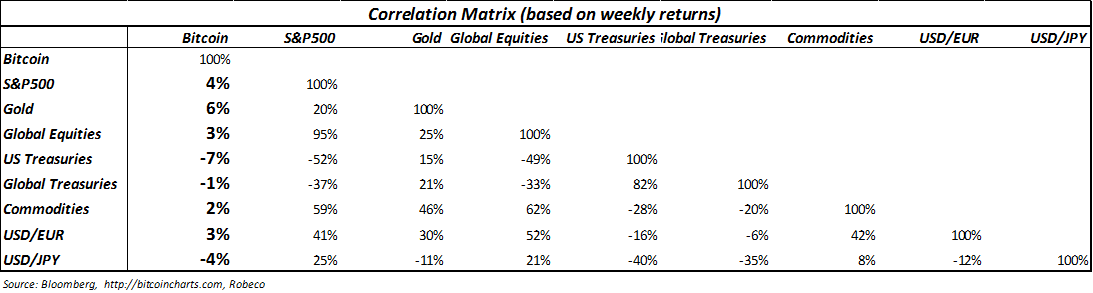

Although the difference in return is extreme, it could still well be that bitcoin returns move in tandem with the returns of one or more of the major asset classes. To get an idea to what extend the returns of bitcoin and other asset classes are related I calculated the correlation of weekly returns. The results are shown in the table below. As can be derived from the second column, bitcoin returns are pretty much uncorrelated with all other asset classes. Statistically, this implies that there a diversification benefits to be gained.

(click to enlarge)

Extreme return, extreme risk

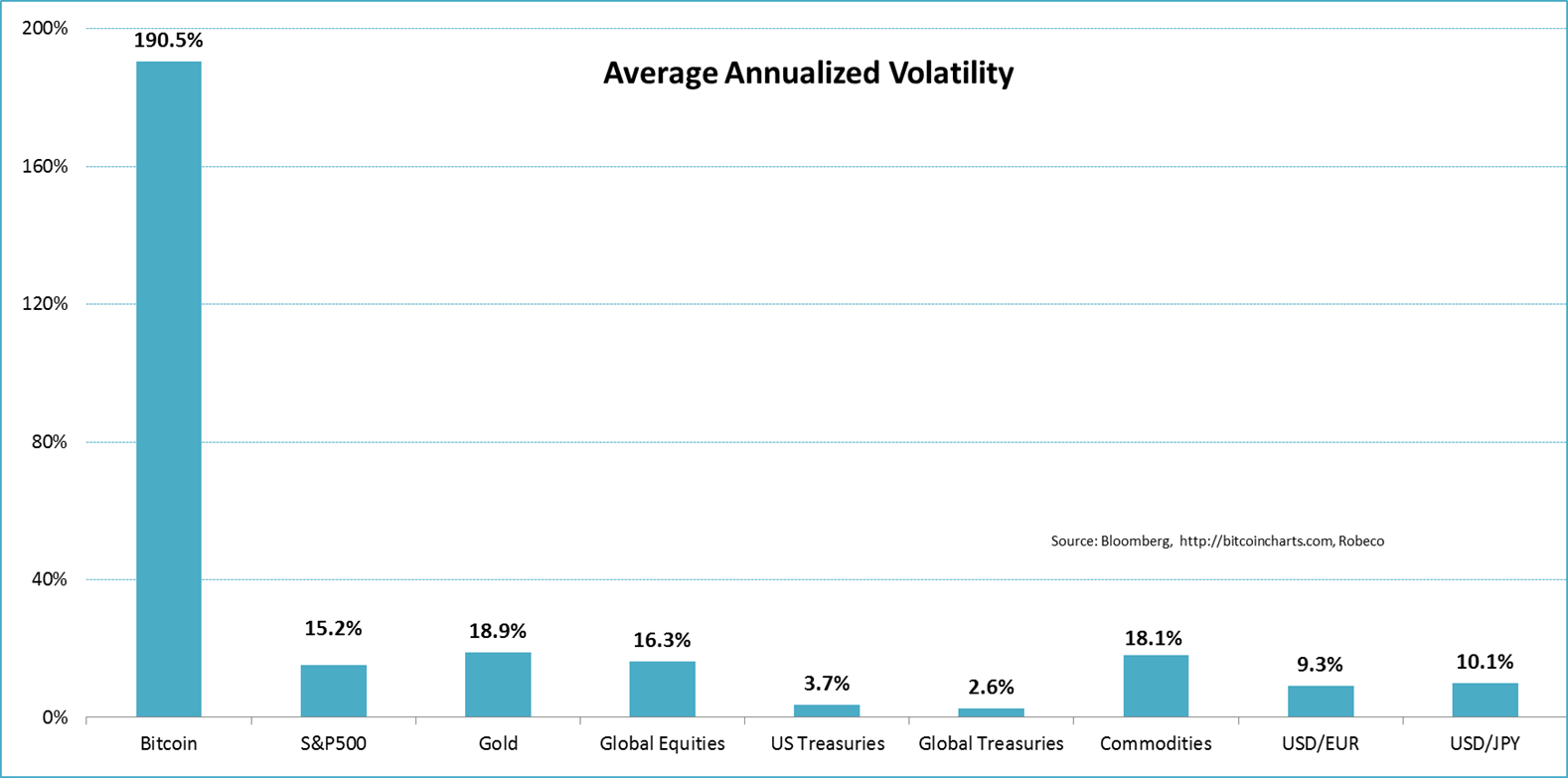

Looking at returns is only half the story. Return and risk are two sides of the same, yes, coin. In order to give an objective view on the characteristics of bitcoin in relation to other, more common asset classes, risk should be taken into account as well. The next graph shows the annualized volatility of the asset classes already mentioned above. Again the results are very explicit. Not only are bitcoin's returns remarkably high, so is its risk. The average annualized volatility of bitcoin is 190%(!), almost ten times larger than the second-largest volatility (gold 18.9%). Equally important is that these findings are in fact in compliance with traditional risk and return metrics. Higher returns are accompanied by higher risk. However, for bitcoin the extreme return probably also means an unbearable risk from a traditional investment perspective.

(click to enlarge)

Let me try to explain this. With major asset classes like equities and bonds it's common to look at the relationship between risk and return, for example measured by the Sharpe-ratio (return divided by risk). For instance, since July 2010 global equities realized a Sharpe-ratio of 0.67 and bonds of 1.15, which is already pretty impressive. But that is nothing compared to bitcoin that realized a Sharpe-ratio of 8.60. This has never been realized by any other asset class. However, only looking at the Sharpe-ratio would mask the sheer magnitude of the return and risk that are behind it. A risk of 190% is just too much to deal with. No (multi asset) investor is able to except such risk and return characteristics as it would make all other investment decisions totally irrelevant.

(click to enlarge)

To point this out, I have calculated the risk-return characteristics of two multi asset portfolios. The first is a traditional multi asset portfolio containing 50% global equities and 50% global treasuries. The second portfolio invests exactly 1% in bitcoin leaving 49.5% for both global equities and global treasuries. The results are shown in the graph below. They are pretty straightforward. Only a 1% investment in bitcoin is more than enough to completely reshape the risk and return characteristics of the whole portfolio. A 1% investment will make the whole multi asset portfolio look like bitcoin. Including only 1% bitcoin would have resulted in an annualized return of 344% compared to 7.1% for the 50-50 portfolio. At the same time the annualized volatility would rise to 111% compared to 8.2% for the traditional portfolio. This is no longer a multi asset portfolio benefiting from diversification. This is a bitcoin portfolio with some extras.

(click to enlarge)

Conclusion

Bitcoin is a very complex but also a very interesting new development within the financial markets. One that has brought some early adopters already a lot of good fortune. Also one that has done very well from a theoretical risk-return perspective. The Sharpe-ratio is incredibly high and the correlation with other asset classes is very low.

But it is at this point too early to see bitcoin as a mature new asset class like equities, bonds or other currencies. Its characteristics are simply too extreme at this point in time. Therefore is does not provide a realistic alternative for investors, yet. This could well change in the future. As with any new investment class, reaching a mature status takes a while. To determine how far bitcoin has come in this process, we should not only depend on (sound) qualitative statements and expectations. To establish if and when bitcoin becomes a credible alternative to investors we have to look at the numbers as well. For now, Wall Street and bitcoin are different worlds.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1876731-bitcoin-and-wall-street-different-worlds-for-now?source=feed

Aucun commentaire:

Enregistrer un commentaire