Mid-cap stocks have done quite well this year. The return of the S&P MidCap 400 index year-to-date is at 27.32%, while the return of the S&P 500 index during the same period is at 25.87%.

In my previous post, I described the best S&P 500 dividend stocks according to Buffett principles. In this article I describe the best mid-cap dividend stocks which are included in the S&P MidCap 400 index, according to the same principles.

A Ranking system sorts stocks from best to worst based on a set of weighted factors. Portfolio123 has a powerful ranking system which allows the user to create complex formulas according to many different criteria. They also have highly useful several groups of pre-built ranking systems, I used one of them the "All-Stars: Buffett" in this article. The ranking system is based on investing principles of the well-known investor Warren Buffett.

The "All-Stars: Buffett" ranking system is quite complex, and it is taking into account many factors like; book value growth, operational P/E, price to book value, trailing P/E, price to Tangible book value, price to cash flow and EPS Stability, as shown in the Portfolio123's chart below.

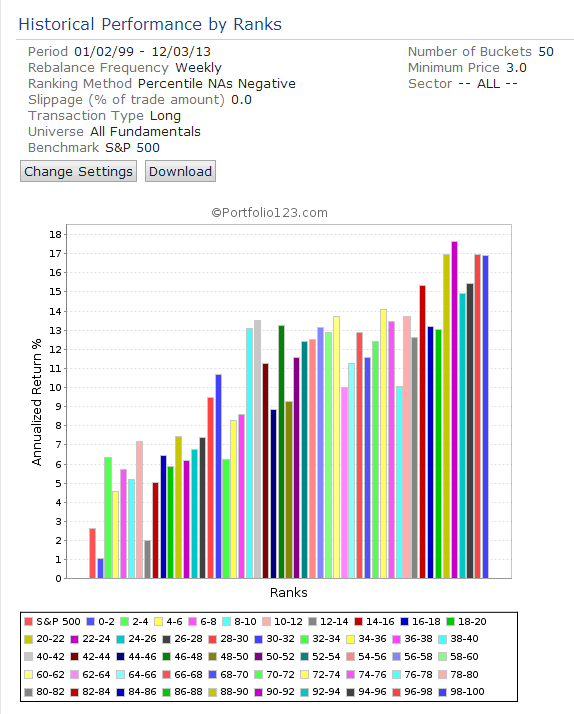

In order to find out how such a ranking formula would have performed during the last 15 years, I ran a back-test, which is available by the Portfolio123's screener. For the back-test, I took all the 7,014 stocks in the Portfolio123's database.

The back-test results are shown in the chart below. For the back-test, I divided the 7,014 companies into fifty groups according to their ranking. The chart clearly shows that the average annual return has a very significant positive correlation to the "All-Stars: Buffett" rank. This brings me to the conclusion that the ranking system is useful.

(Click to enlarge)

After running the "All-Stars: Buffett" ranking system on the companies which are included in the S&P MidCap 400 index and pay a dividend with a higher than 1% yield, on December 04, before the market open, I discovered the twenty best dividend stocks, which are shown in the chart below. In this article, I describe the three best stocks according to this ranking system. In my opinion, these stocks can reward an investor a significant capital gain along with a solid dividend. I recommend readers use this list of stocks as a basis for further research. All the data for this article were taken from Yahoo Finance, Portfolio123 and finviz.com.

(Click to enlarge)

ManTech International Corporation (MANT)

ManTech International Corporation provides technologies and solutions for critical national security programs in the United States and internationally.

ManTech International has a very low debt (total debt to equity is only 0.17) and it has a very low trailing P/E of 13.17 and a forward P/E of 15.32. The price to book value is very low at 0.87, and the price-to-sales ratio is also very low at 0.43. The price to free cash flow for the trailing 12 months is at 17.59, and the average annual earnings growth estimates for the next five years is at 8%. The forward annual dividend yield is quite high at 2.98%, and the payout ratio is only 38.9%.

ManTech has recorded revenue and EPS growth, during the last five years, as shown in the table below.

Most of ManTech's stock valuation parameters have been better than its industry median, sector median and the S&P 500 median, as shown in the table below.

(Click to enlarge)

Source: Portfolio123

On October 30, ManTech reported its third-quarter financial results, which missed EPS expectations by $0.02.

Third Quarter 2013 Highlights

- Revenue: $567 million

- Diluted EPS: $0.48

- Cash Flow from Operations: $77 million

- Bookings: $647 million in contract awards for a book-to-bill ratio of 1.1

- Dividends: $0.21 per share paid in September; $0.21 per share authorized for December

In the report, ManTech Chairman and Chief Executive Officer George J. Pedersen said:

Our cyber, intelligence, and health businesses continue to grow, and we continue to generate exceptional cash flow. With a Continuing Resolution that funds the government at last year's levels through January 15, 2014, our employees who had been furloughed have returned to work performing their mission-critical activities. ManTech's strong balance sheet and positioning with priority missions offer stability during this period of uncertainty.

ManTech has recorded revenue and EPS and growth, and considering its cheap valuation metrics, and its good earnings growth prospects, MANT stock can move higher. Furthermore, the rich dividend represents a nice income.

(Click to enlarge)

Chart: finviz.com

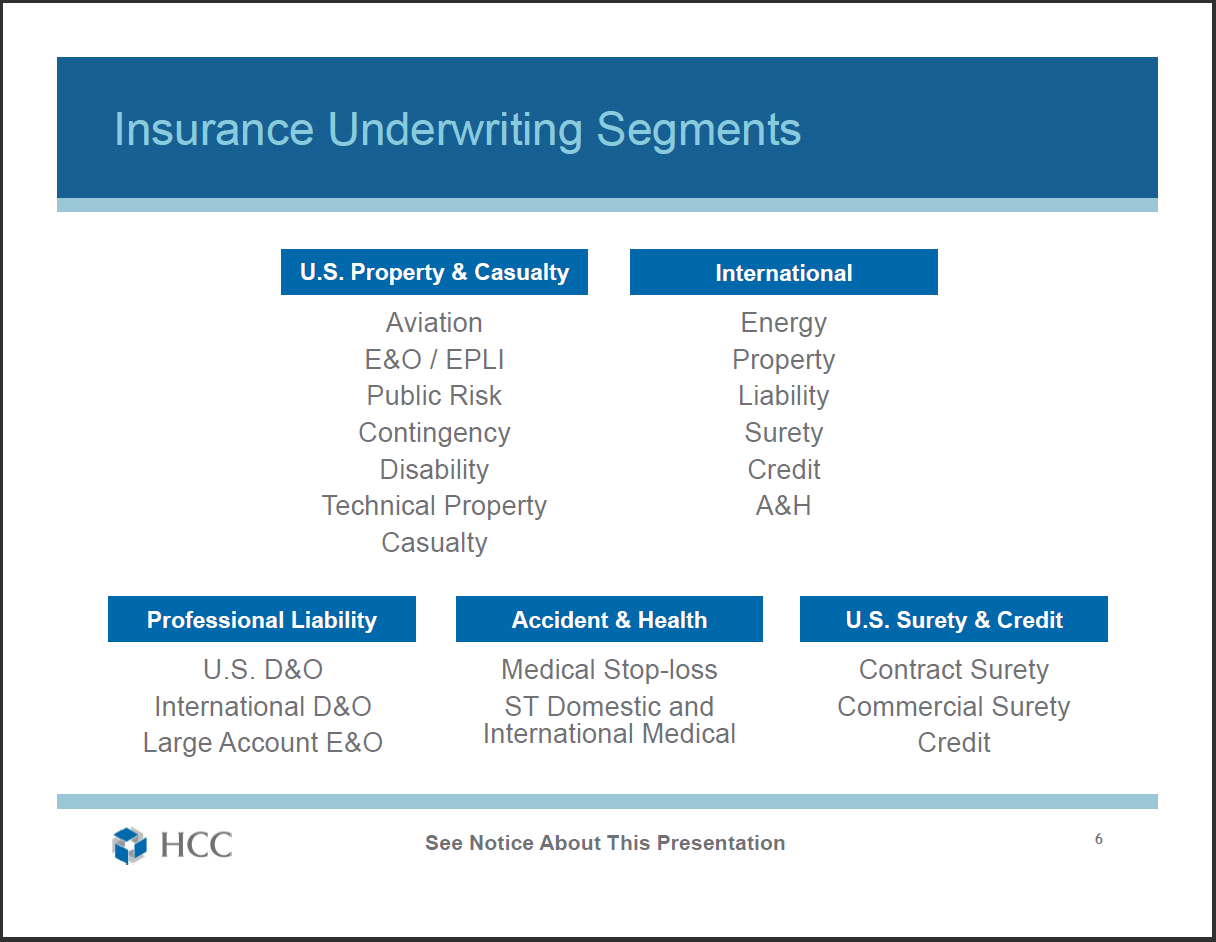

HCC Insurance Holdings Inc. (HCC)

HCC Insurance Holdings, Inc. underwrites non-correlated specialty insurance products worldwide.

(Click to enlarge)

(Click to enlarge)

Source: Q3 2013 Investor Presentation

HCC Insurance has a very low debt (total debt to equity is only 0.18), and it has a very low trailing P/E of 10.05 and a very low forward P/E of 12.43. The price to free cash flow for the trailing 12 months is very low at 12.15, and the average annual earnings growth estimates for the next five years is at 7.0%. The forward annual dividend yield is at 1.98%, and the payout ratio is only 14.5%. The annual rate of dividend growth over the past three years was at 9.41% and over the past five years was at 9.62%.

The HCC stock price is 1.71% above its 50-day simple moving average and 5.86% above its 200-day simple moving average. That indicates a mid-term and a long-term uptrend.

HCC Insurance has recorded solid revenue, EPS and dividend growth during the last year, the last three years and the last five years, as shown in the table below.

On October 29, HCC Insurance reported its third-quarter financial results, which beat EPS expectations by $0.12.

Third Quarter 2013 Highlights and Updated 2013 Guidance:

- Net earnings of $98.2 million, or $0.98 per diluted share

- GAAP combined ratio of 83.5%

- Pretax net catastrophe losses of $17.9 million

- Annualized return on equity of 11.1%

- Annualized operating return on equity of 10.8%

- Updated net earnings guidance for 2013 of $3.70 to $3.80 per diluted share

HCC Insurance has recorded solid revenue, EPS and dividend growth, and considering its cheap valuation metrics and its good earnings growth prospects, HCC stock still has room to go up. Furthermore, the solid growing dividend represents a nice income.

Risks to the expected capital gain and to the dividend payment include a downturn in the U.S. economy and large catastrophe losses.

(Click to enlarge)

Chart: finviz.com

Stancorp Financial Group Inc. (SFG)

StanCorp Financial Group, Inc., together with its subsidiaries, provides financial products and services in the United States.

StanCorp has a very low debt (total debt to equity is only 0.26) and it has a low trailing P/E of 14.00 and a very low forward P/E of 12.66. The PEG ratio is very low at 0.77, and the price-to-sales ratio is also very low at 0.98. The price to free cash flow for the trailing 12 months is very low at 10.89, and the average annual earnings growth estimates for the next five years is very high at 18.20%. The forward annual dividend yield is at 1.73%, and the payout ratio is only 20.4%.

The SFG stock price is 1.88% above its 20-day simple moving average, 8.31% above its 50-day simple moving average and 28.65% above its 200-day simple moving average. That indicates a short-term, a mid-term and a long-term uptrend.

On October 22, StanCorp reported its third-quarter financial results, which beat EPS expectations by $0.38. The company reported net income of $59.0 million, or $1.32 per diluted share for the third quarter of 2013, compared to net income of $44.9 million, or $1.01 per diluted share for the third quarter of 2012. In the report, Greg Ness, chairman, president and chief executive officer said:

Our business lines reported excellent results for the third quarter of 2013, which included a very favorable group insurance benefit ratio and record earnings in our Asset Management segment. We are seeing the benefits from the pricing actions that we have taken and are executing on our plan to deliver long-term shareholder value.

StanCorp Financial Group has compelling valuation metrics and strong earnings growth prospects, and considering the fact that the stock is in an uptrend, SFG stock can move higher. Furthermore, the solid dividend represents a nice income.

(Click to enlarge)

Chart: finviz.com

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1880411-best-mid-cap-dividend-stocks-according-to-buffett-principles?source=feed

Aucun commentaire:

Enregistrer un commentaire