My purpose for this article is multi-faceted. I will argue that Aflac (AFL) is a company that fits remarkably well into the criteria we know the great "Oracle of Omaha" Warren Buffett looks for in investments for his company, Berkshire Hathaway (BRK.A, BRK.B). By doing so I hope to both educate readers on the characteristics that Warren Buffett/long-term value investors look for, and to make a compelling case for an investment in Aflac specifically right now.

I find many stocks by screening for candidates, but not Aflac. This was an intuitive find. Last summer, I actually interned as an insurance sales agent for the company and, while I must admit sales is extremely difficult and definitely not for me, I was very impressed with how well-run the Aflac organization is. It didn't come to me in an instant, but as my 10 week internship progressed and I learned about the company and became motivated to do some research, I gradually came to the realization that Aflac fits Warren Buffett's investment criteria almost perfectly. While some of the comparisons I make may further my point but not be all that material to the average investor, I think the overall thesis will be very helpful and educational in explaining why Aflac is an attractive investment and how to integrate Warren Buffett's best methods into your own strategy. My arguing points are below:

Business Model

Aflac is an insurance company. Insurance is one of Berkshire's biggest lines of business. By my count from the 2012 Annual Report, Berkshire owns at least 13 insurance subsidiaries including:

GEICO, the third largest private passenger auto insurer in the United States and two of the largest reinsurers in the world, General Re and the Berkshire Hathaway Reinsurance Group.

Warren Buffett has explained his love for insurance- the float it provides and a talented investment manager are a powerful combination, and float is usually a much cheaper capital source than equity or traditional debt:

Insurers receive premiums upfront and pay claims later. ... This collect-now, pay-later model leaves us holding large sums - money we call "float" - that will eventually go to others. Meanwhile, we get to invest this float for Berkshire's benefit. ...

If premiums exceed the total of expenses and eventual losses, we register an underwriting profit that adds to the investment income produced from the float. This combination allows us to enjoy the use of free money - and, better yet, get paid for holding it.

So float is good, but only when it's free. That's why Buffett stresses the importance of underwriting at a profit no matter what. He'd be happy to see that Aflac's combined ratio has been between 80-85% and the company has recorded an underwriting profit for at least the 11 years that data is shown for in the company's latest FAB.

Brand

Aflac has an extremely strong brand, especially relative to its size. CoreBrand estimated the company's brand equity was $3.4B in 2010 and it is probably worth substantially more than that now. Warren Buffett stresses the importance of differentiating/protecting a business from competitors through what he calls 'economic moats,' or powerful and sustainable competitive advantages. The most obvious, most-used, and historically Buffett's favorite form of economic moat is a strong brand. For example, Coca-Cola (KO) is one of Berkshire's biggest holdings and seemingly Buffett's favorite stock investment of his career. The biggest thing Coca-Cola has going for it is its incredibly strong brand which was, until recently, considered to be the strongest in the world for 13 straight years.

Most Japanese and Americans would agree that Aflac has a powerful brand. The company's duck mascot is loved and adored in both countries. It has starred in 53 US television ads and was honored in 2004 with a place on Madison Avenue's Advertising Walk of Fame. Consider this: both GEICO and Aflac are large, highly-regarded insurers with easily-recognizable names that are actually acronyms for their former identities, strong brands, and loved animal mascots that have been around for years.

Weird, huh?

But in investing, it's the future we care about, not the past. Aflac has a great brand now, but will that be the case in the future? I certainly think so. From my experience as an agent I learned how critical Aflac's brand is to the success of its agents and in turn, the success of the business. In the U.S., Aflac markets its products at the workplace. The value proposition to business owners is compelling- they don't pay anything (can subsidize or pay completely if they choose to) and get to advertise Aflac in their benefits plans. Therefore, if you can speak to them and get the point clearly across that they're not paying anything, there's a very good chance that they will comply and offer Aflac.

The challenge is actually talking to them. It's very difficult to get the ear of a business owner or HR manager. There are usually many gatekeepers involved and everyone is distrustful of salesmen. Aflac competes with much smaller supplementary health insurance companies that don't have anywhere near the brand that Aflac does. Aflac agents have a much higher chance of getting in front of the people who matter because of this unrivaled brand recognition.

The company knows this and continues to invest in advertising, spending over $100mm each in the US and Japan in each of the last 3 fiscal years, $127mm each in 2012. CoreBrand estimated the company's brand equity to be $3.4B in 2010 versus $940mm in 2002. That's a CAGR of 17.43%. The brand also doubled as a percentage of market cap. That kind of growth shows Aflac has been committed to growing it's brand and, because it is so vital to the business, I expect that focus to remain unchanged.

Size

Warren Buffett recently described himself as "elephant hunting." He's searching for big enough 'elephants' of investments that he can devote a material amount of Berkshire's cash to. Aflac is a $31B company with $129mm worth of stock changing hands daily. It is certainly a big enough elephant for Buffett and Berkshire. While this may be immaterial to many of the retail investors that read this, even institutional investors much smaller than Buffett can appreciate the liquidity and stability that a large, established company like Aflac offers.

Outlook

Not just Warren Buffett, but most sophisticated investors are interested in owning businesses that will not only continue to exist, but also benefit in a changing macroeconomic landscape. I believe Warren Buffett would appreciate Aflac's prospects. It seems clear, for better or worse, the direction of healthcare and health insurance in America with the ACA is socialized medicine. We may not get there, but we're headed in that direction. To figure out how this change will impact Aflac U.S., we need only look at Aflac Japan, where medicine is quite socialized and differences in coverage from one citizen to the next are few and far between. Because everyone in Japan has virtually the same coverage on their major medical and as in the U.S., the major medical offering does not cover everything and to the extent needed in many cases, citizens personalize and supplement their major medical with Aflac's supplemental offerings. Aflac has been incredibly successful there, with majority market share in some product categories. 90% of companies listed on the Tokyo Stock Exchange offer Aflac to their employees and Aflac insures one in every four households in Japan. I'm not saying Aflac will enjoy that kind of dominance in the U.S. anytime soon, but the opportunity is certainly there. The ACA introduces difficult-to-navigate complexities and regulations to the major medical insurance industry in the U.S., but it really doesn't affect Aflac much. Business owners and individuals will appreciate Aflac's simple, cash-pay, portable, ACA-unaffected plans and the 'shopping for insurance' focus will move to supplemental insurance like it has in Japan.

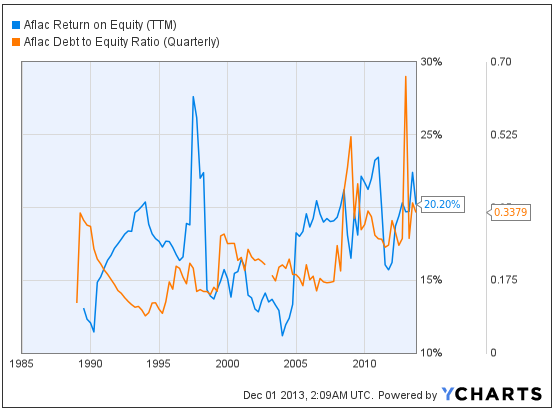

Highly-Profitable

To this point, I haven't really quantified Buffett's strategy. Buffett looks for what he calls great businesses- businesses that can sustainably generate high returns on unlevered capital. Aflac is a low-debt operation that has consistently generated ROE >12% for 25 years, averaging nearly 20% in the last 5 years. Through it all, the company has maintained a reasonable leverage level, with debt/equity averaging .3328 in the last 5 years. Sustainable- check. High returns- check. Unlevered capital- check.

(Click to enlarge)

Competent, Candid Management

Buffett looks for talented management that is willing to stay around and that he can trust to manage in a way that maximizes long-term shareholder value. Management's competence at Aflac has really already been demonstrated through my discussion of the brand, consistency, high ROE, and market share.

Determining whether a company's management is candid and worthy of your trust is much more abstract and difficult. To help us out, let's look at a business Warren has bought in the past. In 1973, Buffett began purchasing shares of the Washington Post Company (WPO). Since then he's added to his position, seen massive gains, and continues to hold his shares. At the time, the company was led by the late Katharine Graham. She was the daughter of Eugene Meyer, who bought the Post in a bankruptcy auction in 1933 and got the business going again. The Washington Post meant more to Katharine Graham than a typical CEO because it was her family's business. She grew up with the company and was probably trained informally her whole life for that position. Buffett knew she wanted nothing more than to extend her father's legacy and create her own by leading WPO to further successes. He also knew that the chances of her leaving and being replaced were highly unlikely. He and Katharine became great friends. She introduced him to some of most powerful people in America at the time personally and made him a ton of money professionally. Near the end of Katharine Graham's life, her son Donald took over as CEO. Buffett most likely reasoned he could trust Donald Graham for the same reasons he justified trusting his mother. Clearly his trust in Graham continues to be very strong. The Washington Post Company under Don Graham has turned into more of an education company than anything else through its Kaplan subsidiary. The company also recently sold its original core newspaper business, which Buffett delivered newspapers for as a young boy, to Jeff Bezos. The company is really struggling, but Buffett hasn't sold. He trusts Graham can turn it around.

Aflac is also a family-run business. The company was founded in 1955 by three brothers: John, Paul, and Bill Amos. As they handled the business, Paul's son Daniel prepared himself to become the company's future leader. In 1973, he started right out of college in the company's sales force and in 10 years rose to the rank of state sales coordinator before being named the company's president in 1983, COO in 1987, CEO in 1990, and chairman in 2001. He oversaw the emergence of the Aflac duck and the company's growing dominance in Japan and the US in the past 24 years. He's been named on Institutional Investor magazine's America's Best CEOs list in the insurance category five times, most recently in 2010. He's also been one of the top 50 CEOs on Chief Executive magazine's Wealth Creation index every year since it was created in 2008. He is now 62 years old and may not be running the show much longer, but his son Paul II is being groomed to take his place and seems very capable. I can't speak for Buffett, but I think these men are both competent and candid.

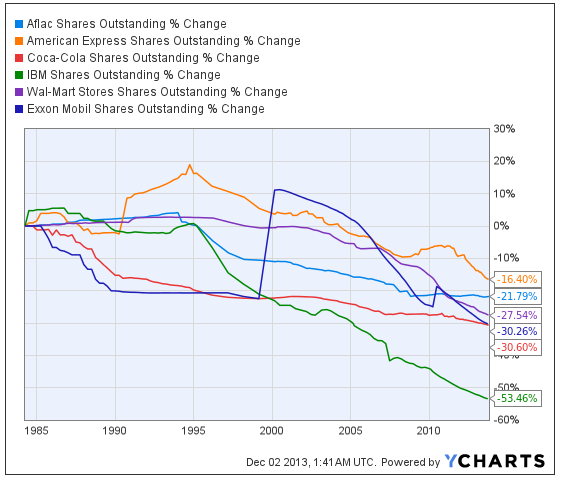

Capital Return

Though Warren Buffett is an outspoken critic of dividends as a return of capital (he much favors share repurchases for the tax savings and choice it provides to shareholders), he would much rather a company he owns return capital to him than destroy value keeping it on the balance sheet earning miniscule returns or wasted on an overpriced acquisition. This is one of the clearest commonalities in Berkshire's portfolio. The chart below shows Aflac along with many of Berkshire's biggest holdings. They've all reduced their share count a great deal through share repurchases.

(Click to enlarge)

Many Berkshire holdings also return capital by paying regular dividends which Aflac also does and has done for an impressive 30 years with annual dividend increases in almost every year and no decreases. Warren Buffett would appreciate this focus on delivering value to shareholders consistently.

Undervalued

Warren Buffett isn't a deep value hunter like many value investors. He looks for great companies at fair prices- slightly undervalued if he can get it, but such opportunities don't come very often with the large, consistent, quality companies he is open to investing in. I don't think Aflac is deeply-undervalued, but I do think the stock is trading at a pretty attractive level.

Valuing Aflac relatively by comparing P/B to that of other insurers won't do us much good because the company justifies a higher P/B by earning much higher ROE than most insurers do. Instead, I valued the company on an absolute basis using a dividend discount model. I used the following inputs/assumptions:

- Net Income (TTM): $3064mm

- Book value of equity, Now: $14658mm

- Book value of equity, Year prior: $15985mm

- EPS : $6.54

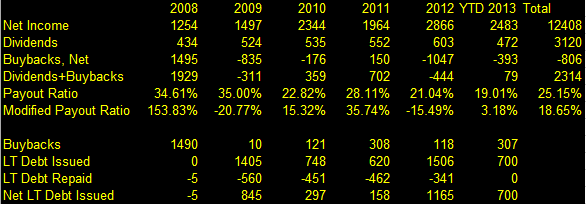

- DPS : $1.44 - Complications often arise when using a dividend discount model to value a firm that repurchases large quantities of stock like Aflac. The solution that valuation expert Aswath Damodaran recommends is to add net buybacks (cash spent on share repurchases less net increases in debt) to dividends, but when I did this for Aflac, I found that increases in long term debt actually outweighed the share repurchases in recent years, resulting in a much lower payout ratio that, if input into my model, would return a value higher than that returned by just inputting the actual dividends.

(Click to enlarge) To be conservative, I just used the actual dividends in my model. - Normalized ROE: 19.8% (5 year average) gradually deteriorating to terminal ROE

- Terminal ROE: 13%

- Risk-free rate: 2.79%

- Equity risk premium: 5.5%

- Beta: 2.32

- Terminal Beta: 1.2

- Length of high growth period: 5 years

- Terminal growth rate: 2%

I would be glad to entertain any other uncertainties or questions regarding my method in the comments section of this article. The value per share I came up with was $83.63, 26% higher than Aflac's current share price of $66.37. That's not spectacular, but that is a pretty big discrepancy for a company of Aflac's size and quality.

Conclusion

In this article, I've attempted to demonstrate that Aflac is a company with characteristics that Warren Buffett and many other long-term oriented value investors typically look for. Aflac is to me, the epitome of a 'great company at a fair price' right now. I don't think the fact that Buffett and Berkshire don't currently own Aflac shares invalidates my thesis. The Amos family may be against a large shareholder coming in. There may be insurance or anti-trust regulations I am unfamiliar with that would make it difficult for Berkshire to add Aflac shares to its already large insurance portfolio. It's unlikely but maybe Buffett just hasn't researched the company. Maybe he isn't comfortable investing in a company that derives most of its revenues from Japan and owns Japanese bonds in the face of a potential Japanese default. Whatever the case may be, I strongly believe Aflac to be a solid long-term investment and intend to execute on that thesis by buying shares soon.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in AFL over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1873831-aflac-an-attractive-buffettesque-investment?source=feed

Aucun commentaire:

Enregistrer un commentaire