I tried to create a dividend portfolio that can outperform the market by a big margin. The following screen, which draws inspiration from the work of the well-known investor Ben Graham, shows such promise. In most of my previous screens, the demand was to rebalance the portfolio every four weeks and replace the stocks that no longer comply with the screening requirement with other stocks that comply with the requirement. Since many investors do not have the opportunity to rebalance the portfolio every four weeks, in this portfolio the demand is to rebalance only every six months.

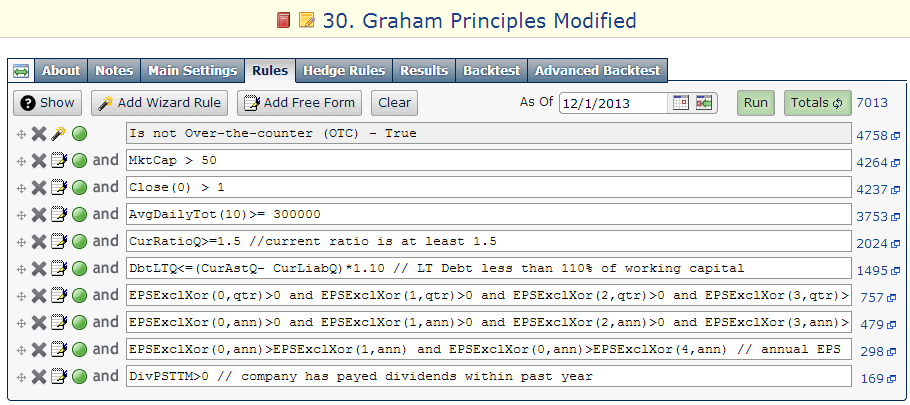

The screen's method requires all stocks to comply with all following demands:

- The stock does not trade over-the-counter (OTC).

- Market cap is greater than $100 million.

- Price is greater than 1.00.

- Average daily total amount traded for the past 10 days.

- Current ratio is at least 1.50.

- Long-term debt is less than 110% of working capital.

- Last 4 quarters of EPS above breakeven.

- Last 5 years of EPS above breakeven.

- Annual EPS grew over past year and past 5 years.

- Company has paid dividends within past year.

- The twenty stocks with the best ranking according to Graham principles among all the stocks that complied with the first ten demands (the ranking system is available on Portfolio123's All-Stars list).

I used the Portfolio123's powerful screener to perform the search and to run back-tests. Nonetheless, the screening method should only serve as a basis for further research. All the data for this article were taken from Yahoo Finance, Portfolio123 and finviz.com.

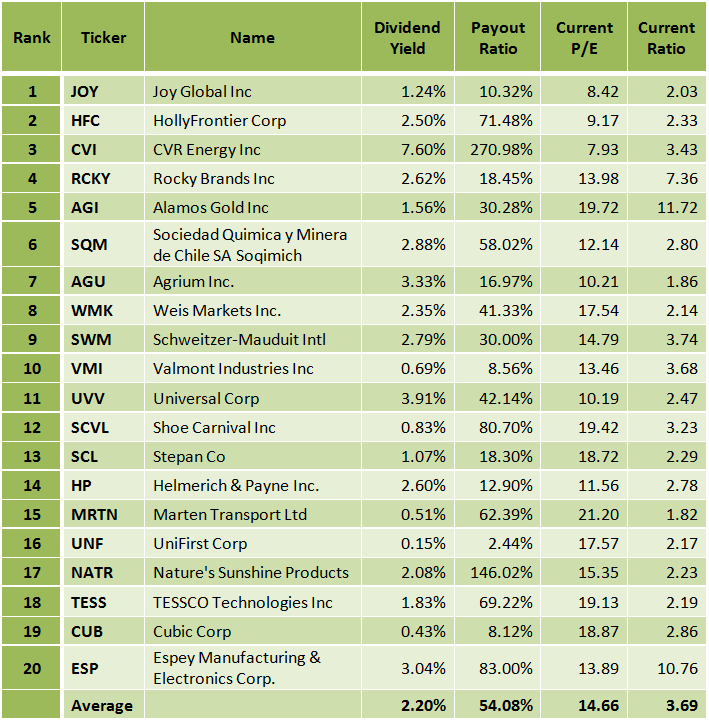

After running this screen on December 01, 2013, I discovered the twenty stocks which are shown in the table below. In this article, I describe the five best stocks according to Graham ranking system.

(click to enlarge)

The table below presents the dividend yield, the payout ratio, the trailing P/E ratio and the current ratio, for the twenty companies.

(click to enlarge)

Joy Global, Inc. (JOY)

Joy Global Inc. engages in the manufacture and servicing of mining equipment for the extraction of coal, copper, iron ore, oil sands, and other minerals.

See my article from November 15, 2013.

(click to enlarge)

Chart: finviz.com

HollyFrontier Corp (HFC)

HollyFrontier Corporation operates as an independent petroleum refiner and marketer in the United States.

(click to enlarge)

(click to enlarge)

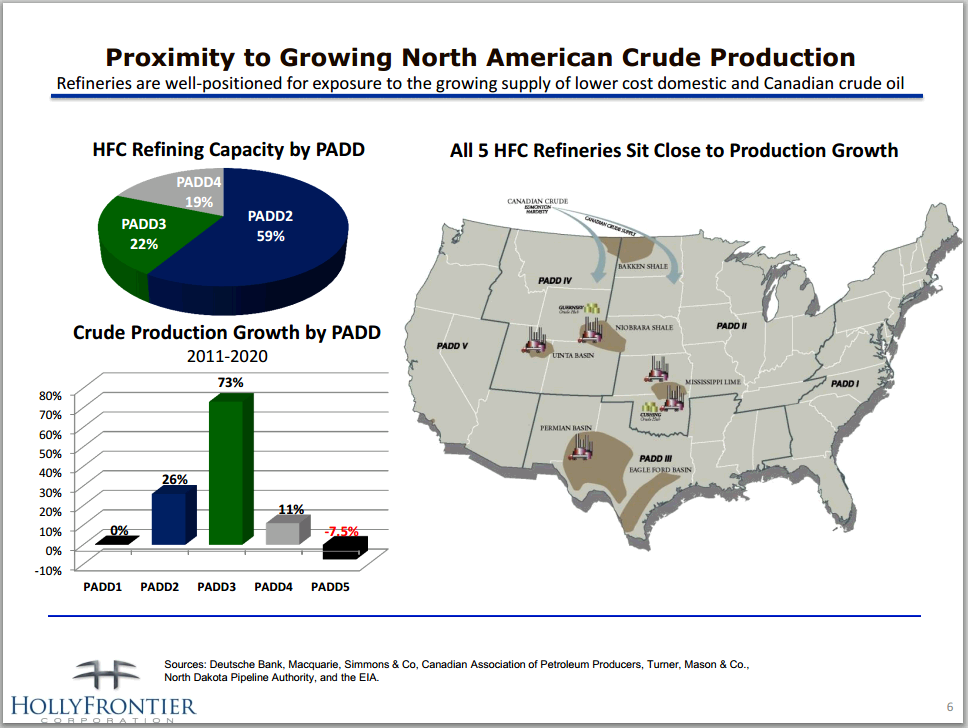

Source: company presentation

HollyFrontier has a very low debt (total debt to equity is only 0.16), and it has a very low trailing P/E of 9.17 and a very low forward P/E of 12.11. The current ratio is at 2.33, and the price-to-sales ratio is very low at 0.47. The forward annual dividend yield is at 2.50%, and the payout ratio is at 72.5%.

The HFC stock price is 5.52% above its 20-day simple moving average, 9.87% above its 50-day simple moving average and 5.96% above its 200-day simple moving average. That indicates a short-term, a mid-term and a long-term uptrend.

HollyFrontier has recorded strong revenue, cash flow, EPS and dividend growth during the last three years and the last five years, as shown in the charts below.

(click to enlarge)

Source: company presentation

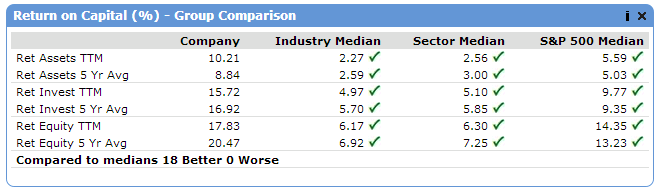

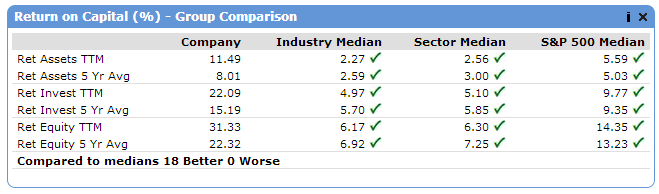

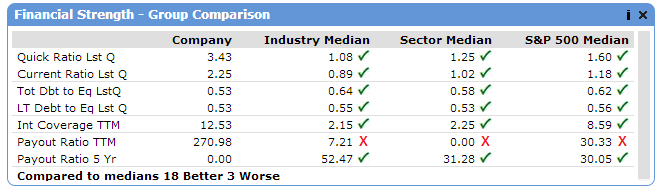

Most of HollyFrontier's stock valuation and return on capital parameters have been better than its industry median, sector median and the S&P 500 median, as shown in the tables below.

(click to enlarge)

(click to enlarge)

Source: Portfolio123

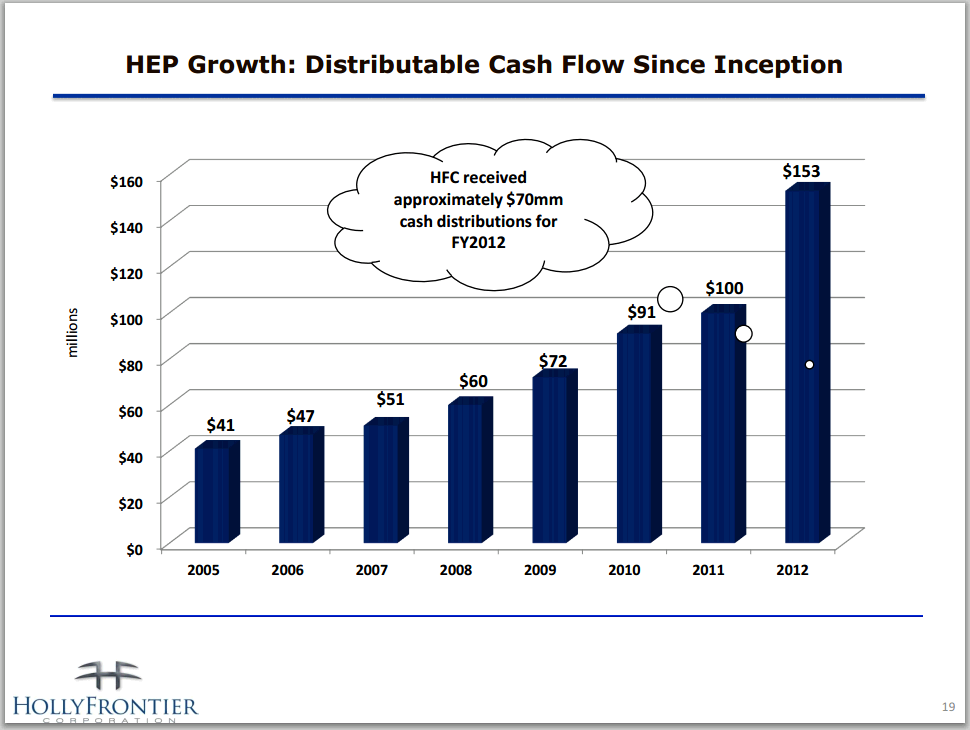

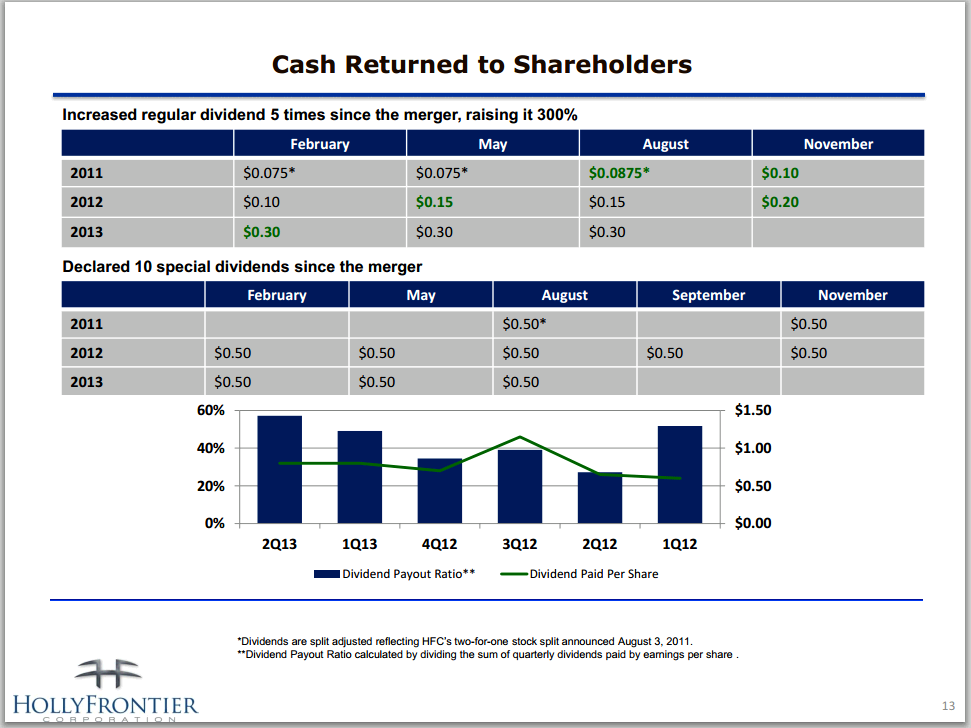

The chart below emphasizes the continuous cash returned by the company to its shareholders.

(click to enlarge)

Source: company presentation

On November 06, HollyFrontier reported its third-quarter financial results. The company reported third quarter net income attributable to HollyFrontier stockholders of $82.3 million or $0.41 per diluted share for the quarter ended September 30, 2013, compared to $600.4 million or $2.94 per diluted share for the quarter ended September 30, 2012.

In the report, HollyFrontier's President & CEO, Mike Jennings, commented:

Contraction in the Brent to WTI differential continued to squeeze inland refined product margins from prior year highs, resulting in a year-over-year decrease in third quarter earnings. In addition, higher crude oil prices and elevated RIN costs negatively affected our capture of benchmark refining margins during the third quarter. Looking forward, we see continued growth in North American crude oil production and are confident that our geographic proximity and ability to process both light and heavy crude streams will create attractive opportunities, even as transportation logistics and related crude differentials are rationalized.

HollyFrontier has recorded strong revenue, EPS and dividend growth, and considering its compelling valuation metrics, HFC stock can move higher. Furthermore, the rich dividend represents a nice income.

Risks to the expected capital gain and to the dividend payment include; a downturn in the U.S. economy and lower refining margins.

(click to enlarge)

Chart: finviz.com

CVR Energy, Inc. (CVI)

CVR Energy, Inc., through its subsidiaries, engages in petroleum refining and nitrogen fertilizer manufacturing activities in the United States.

CVR Energy has a very low trailing P/E of 7.93 and a very low forward P/E of 12.78. The price-to-sales ratio is very low at 0.39, and the price-to-cash ratio is at 3.02. The current ratio is very high at 3.43. The forward annual dividend yield is very high at 7.60%, and the payout ratio is very high at 271%.

The CVI stock price is 8.30% above its 20-day simple moving average and 4.91% above its 50-day simple moving average. That indicates a short-term and a mid-term uptrend.

CVR Energy has recorded strong revenue and EPS growth, during the last year, the last three years and the last five years, as shown in the table below.

Most of CVR Energy's return on capital, financial strength and stock valuation parameters have been better than its industry median, sector median and the S&P 500 median, as shown in the tables below.

(click to enlarge)

(click to enlarge)

(click to enlarge)

On November 01, CVR Energy reported its third-quarter financial results. The company reported third quarter 2013 net income of $44.0 million, or 51 cents per diluted share, on net sales of $1,977.1 million, compared to net income of $208.9 million, or $2.41 per diluted share, on net sales of $2,409.6 million for the third quarter of 2012.

In the report, Jack Lipinski, chief executive officer said:

Our third quarter results were heavily impacted by unprecedented downtime related to the Fluid Catalytic Cracking Unit outage at CVR Refining's Coffeyville refinery. Significantly weakened crack spreads and product basis, as well as tightening crude differentials in late August, further impacted our results. The refinery resumed full operations on Sept. 11 and maintained strong operational performance for the remainder of the quarter.

CVR Energy has recorded strong revenue and EPS growth, and considering its good valuation, CVI stock can move higher. Furthermore, the very rich dividend represents a gratifying income.

Risks to the CVI stock include; the global commodity nature of its fertilizer products, the impact of global supply and demand on its selling prices, and the intense global competition from other fertilizer producers.

(click to enlarge)

Chart: finviz.com

Rocky Brands, Inc. (RCKY)

Rocky Brands, Inc. designs, manufactures, and markets footwear and apparel under the Rocky, Georgia Boot, Durango, Lehigh, Mossy Oak, and Michelin brand names.

See my article from November 15, 2013.

(click to enlarge)

Chart: finviz.com

Alamos Gold Inc. (AGI)

Alamos Gold Inc., a gold mining company, engages in the development, exploration, mining, and extraction of precious metals, primarily gold in Mexico and Turkey.

Alamos Gold has a trailing P/E of 19.72, and a forward P/E of 30.52. The price to book value is at 1.92, and the current ratio is very high at 11.72. The forward annual dividend yield is at 1.56%, and the payout ratio is only 30.3%.

Alamos Gold has recorded strong revenue and EPS growth during the last three years and the last five years, as shown in the table below.

Alamos Gold's margins and return on capital parameters have been much better than those of the industry median, the sector median and the S&P 500 median, as shown in the tables below.

(click to enlarge)

(click to enlarge)

On October 31, Alamos Gold reported its third-quarter financial results. EPS came in at $0.08, a $0.01 better than analyst expectations.

Third Quarter 2013 Highlights

- Sold 48,000 ounces of gold at an average realized price of $1,329 per ounce for quarterly revenues of $63.8 million

- Generated cash from operating activities before changes in non-cash working capital of $26.4 million ($0.21 per basic share); after changes in non-cash working capital of $25.7 million ($0.20 per basic share)

- Recognized quarterly earnings of $9.2 million ($0.07 per basic share)

- Ended the third quarter with cash and cash equivalents and short-term investments of $433.7 million, and working capital of $460.1 million

- Completed the acquisition of Esperanza for net cash consideration of $44.7 million and the issuance of 7.2 million share purchase warrants ("warrants") with a five-year term and an exercise price of CAD$29.48

- Completed the acquisition of Orsa for cash consideration of $3.4 million

- Announced a semi-annual dividend of US$0.10 per common share payable on October 31, 2013. The Company has paid a total of $71.1 million in dividends to shareholders over the past four years

In the report, John A. McCluskey, President and Chief Executive Officer explained:

Production of 43,000 ounces in the third quarter of 2013 was consistent with our expectations and total cash costs of $491 per ounce and all-in sustaining costs of $810 per ounce were in line with guidance and remain among the lowest in the industry. The gold price continued to trend lower in the third quarter; however, with our low cost structure we continue to generate strong margins with operating cash flow of $25.7 million. Our strong performance year to date with production of 151,000 ounces at total cash costs of $461 per ounce has us well positioned to meet our 2013 production guidance of between 180,000 and 200,000 ounces of gold at total cash costs of between $500 and $520 per ounce of gold sold.

Alamos Gold has recorded strong revenue and EPS growth, and considering the fact that Alamos Gold's production costs are among the lowest in the industry, AGI stock can move higher. Furthermore, the solid dividend represents a nice income.

(click to enlarge)

Chart: finviz.com

Back-testing

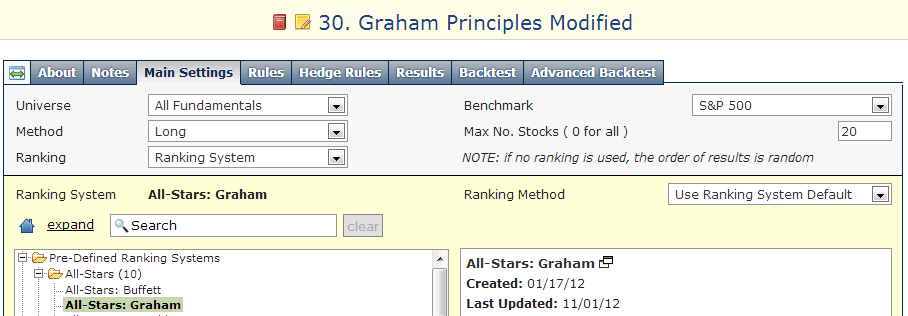

In order to find out how such a screening formula would have performed during the last year, last 5 years and last 15 years, I ran the back-tests, which are available by the Portfolio123's screener.

The back-test takes into account running the screen every six months and replacing the stocks that no longer comply with the screening requirement with other stocks that comply with the requirement. The theoretical return is calculated in comparison to the benchmark (S&P 500), considering 0.25% slippage for each trade and 1.5% annual carry cost (broker cost). The back-tests results are shown in the charts and the tables below.

Since some readers could not get the same results that I got in some of my previous posts, I am giving, in the charts below, the Portfolio123 exact codes which I used for building this screen and the back-tests. The number of stocks left after each demand can also be seen in the chart.

(click to enlarge)

(click to enlarge)

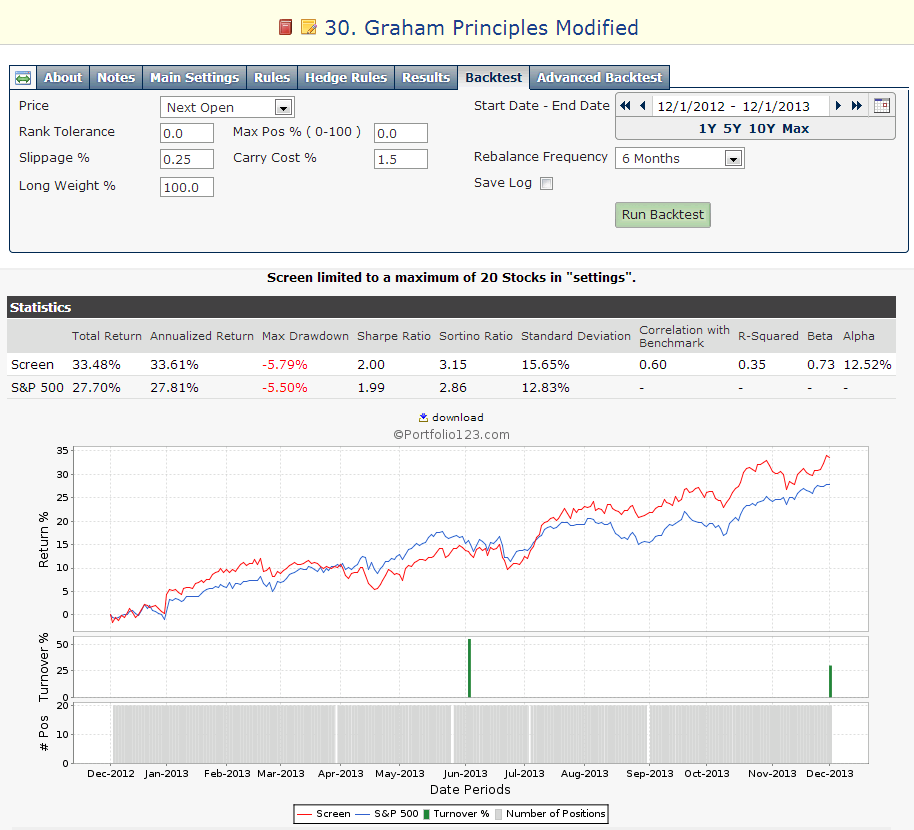

One year back-test

(click to enlarge)

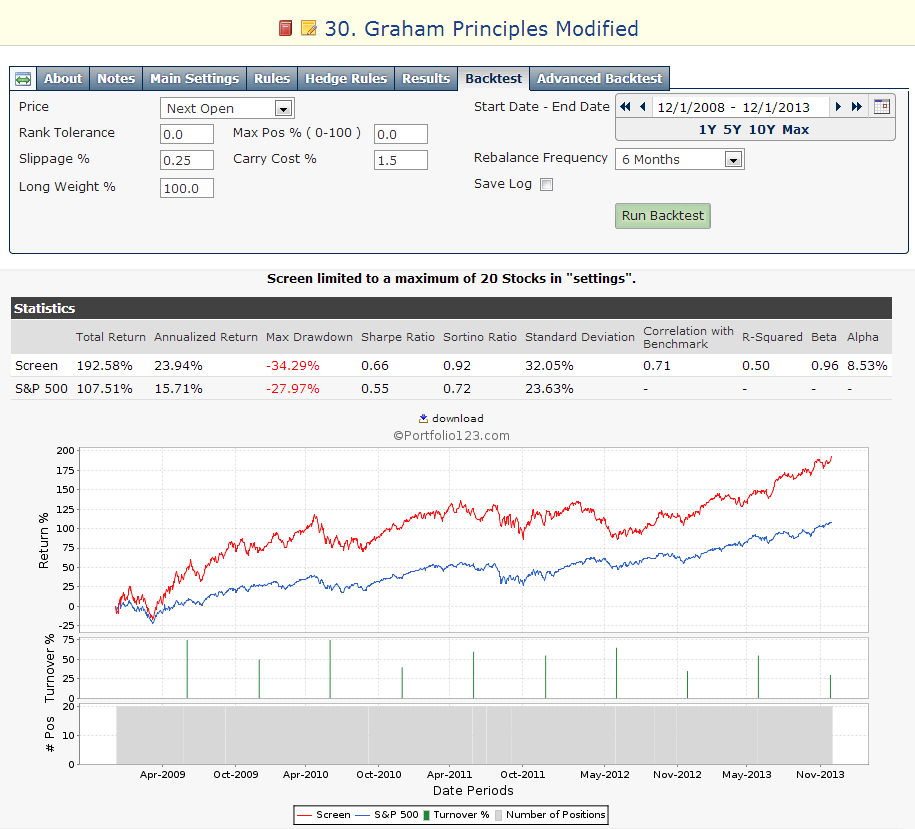

Five years back-test

(click to enlarge)

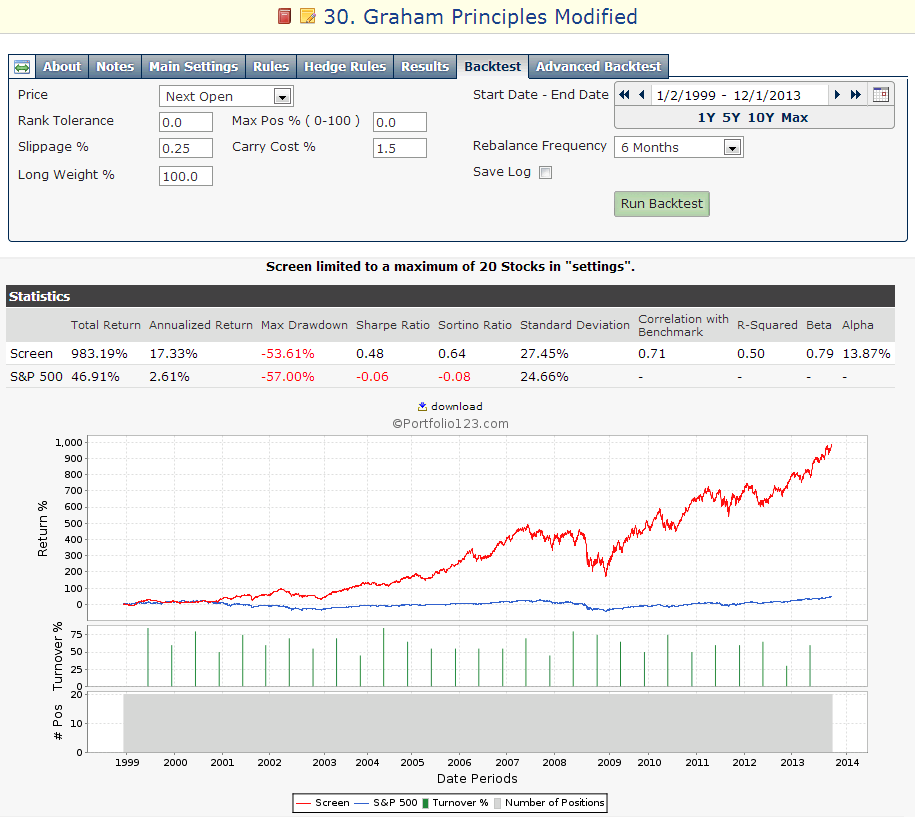

Fifteen years back-test

(click to enlarge)

Summary

The dividend screen has given much better returns during the last year, the last five years and the last fifteen years than the S&P 500 benchmark. The Sharpe ratio, which measures the ratio of reward to risk, was also much better in all the three tests.

One-year return of the screen was high at 33.61%, while the return of the S&P 500 index during the same period was at 27.81%.

The difference between the dividend screen and the benchmark was even more noticeable in the 15 years back-test. The 15-year average annual return of the screen was very high at 17.33%, while the average annual return of the S&P 500 index during the same period was only 2.61%. The maximum drawdown of the screen was at 53.61%, while that of the S&P 500 was at 57%.

Although this screening system has given superior results, I recommend readers use this list of stocks as a basis for further research.

Disclosure: I am long AGI, CVI, HFC, JOY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1873871-a-long-term-winning-dividend-portfolio-based-on-grahams-principles?source=feed

Aucun commentaire:

Enregistrer un commentaire