The US economy is on a path to revival. The economy is making its way out of recession and the government is aiming to increase its spending in order to stimulate this recovery. Construction industry is a highly cyclical one. Construction picks pace during the middle and the late stages of an economic expansion, whereas, the construction stocks are quite suppressed during recession and, especially, in the early stage of recovery. These are the right times to invest in construction.

As the US economy is making its way out of recession, I believe that the worse time is over for the construction industry. Nowadays, I am putting most of my attention to this sector and these companies are becoming a must have in my investment recommendations.

As there are many players in this industry, it becomes a bit tricky to screen out the most promising bets. So, like many other investors, I start my analysis from the basic valuation multiples comparison in order to identify the one stock that deserves a further scrutiny. From the vast pool of players, I put together Tutor Perini (TPC), Foster Wheeler (FWLT), Toll Brothers (TOL) and KB Home (KBH). These are the companies with a market cap of less than $6 billion, not very huge, but you can mostly identify value within such stocks.

Looking at their multiples, two companies stand out to me; TOL and TPC. TOL has the best price to earnings growth out of the lot and TPC stands out on the basis of all other multiples. So, I will base this article on the analysis of TPC and analyze TOL in another one.

SOURCE: Morningstar

About the company

Before I move my analysis further, let me provide a brief overview about the company under consideration. Tutor Perini provides comprehensive project management services, general contracting and pre-construction planning services to public agencies worldwide and private customers. It has four segments that are Civil, Building, Specialty Contractors and Management Services.

The company's performance was better than the industry in most of the aspects over the trailing twelve months. Its operating margins, net margins, ROA and ROE are higher than the industry average. The company's financial leverage is 2.89 times, which is higher than the industry average of 2.31. Therefore, the higher ROE is mainly attributable to a higher financial leverage as well as a higher net margin of the company.

SOURCE: Morningstar

Digging deeper

In order to identify an investment opportunity and the future prospects of a construction company, it's important that you understand the backlog of that company. The construction contracts play a very crucial role in analyzing the companies' future performances. The backlog becomes a tool to enhance the visibility of the future earnings.

As the stock price is the function of earnings and earnings of Tutor Perini depends upon the backlog and new contracts that the company attains, I have conducted a detailed analysis of the company's backlog and contracts in order to examine the future earnings.

Historic backlog

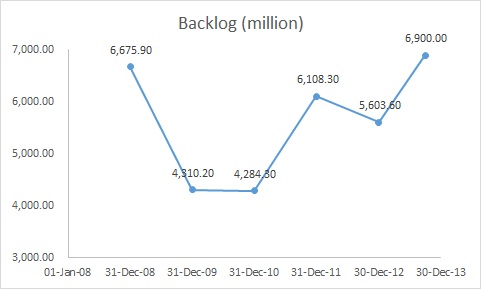

The company's backlog, as of 30 September 2013, is $6.9 billion, which is the highest since the third quarter of the fiscal year 2008. As shown in the following chart, backlog witnessed a razor sharp decline during the recessionary period, from $6,675.9 million to $4284.30 million.

(click to enlarge)

SOURCE: Company's Financials

However, as the economy slowly initiated recovery, the backlog increased from $4,284.30 million to $6,900 million by September 2013. As the US economy is just getting out of recession, I believe that the company's backlog, as a result of more contracts, will increase going forward. Increase in backlog indicates that the company's revenue in the future is secured.

Forecasted backlog

The company has won three projects and a contract since the beginning of the fourth quarter of 2013. On Oct. 21, the company announced three projects with a total worth of about $77 million. The company will record these projects in the backlog of the fourth quarter of FY13.

Ordot Dump Closure Construction & Dero Road Sewer Improvements Project is the project with the highest value. This project has a value of $40.9 million. The project is expected to start in the first quarter of the fiscal year 2014 and complete in July 2015. Therefore, the entire amount of this project will appear in the backlog of the fourth quarter.

U.S. Navy Lockwood Terrace Home Revitalization Project has a net value of $23.8 million, which is expected to begin in April 2014 and complete by 2015. Therefore, the entire amount of this project will also appear in the backlog of the fourth quarter.

The third and last project that the company has included is Duty Free Shoppers Interior Finishing Project. This project has a total worth of $12.7 million. Work on this project has started in October 2013 and expected to complete by March 2014. As the total duration of this project is approximately five months, and about half of the job will be done in the fourth quarter, therefore, I believe that the company will realize half of the $12.7 million in the fourth quarter of 2013 and the remaining half will be added in the backlog of the same quarter.

On Nov. 13, Tutor Perini's subsidiary, Roy Anderson Corp., won a contract of worth $61.3 million. Construction is expected to begin from this month and the completion is expected in December 2014. As per the company's press release, the entire value of the contract will be added in the fourth quarter of the current fiscal.

The company's backlog is $6.9 billion as of 30 September 2013. According to the analyst consensus, the company will be able to record $1.16 billion of revenues, which also indicates that the company's backlog will decrease by $1.16 billion in the fourth quarter. However, value of the three new projects and a contract will increase the backlog as of December 31, 2013. The amount that will be added from the three projects is 71.05 million. The entire amount of contract for the construction of the 225 Baronne Mixed-Use Development Project will be added in the backlog. Therefore, the increase in backlog, resulting from the three projects and a contract, will be $132.35 million, which will be partially offset by the backlog decline of $1.16 billion (that will convert into revenues in the fourth quarter of fiscal 2013).

The company's backlog, as of 31 December 2012, is $5,603.60 million, which, I believe, will increase to the level of $5,872.35 million by the end of 4Q13. This indicates a year over year increase of 4.49% in the backlog. From 31 December 2010 to the end of FY13, the company's backlog grew at a CAGR of 11.08%. As the economy is on its revival path, I believe that the company's backlog will grew more quickly.

Is the backlog better than competitors?

The backlog on its own may not provide a clear image of the company. The prospects should be compared with the other players to analyze the true potential the company has. For that I will compare the company's Enterprise Value/Backlog ratio with its competitors in order to figure out whether the Tutor Perini's prospects are better positioned than its peers or not. Tutor Perini has an enterprise value of $1,750 million, which is lower than its competitors' enterprise value. However, on the flip side, the company's total current backlog has a value of $6,900 million, which is higher than its all direct competitors. Therefore, the company's EV-to-Backlog ratio is 0.25, which is lower than its competitors EV/backlog multiple. Thus, I can say that, based on the backlog the company holds in relation with the enterprise value of the company, TPC is undervalued as compared to its peers.

SOURCE: Yahoo Finance and Companies' Financials

Intrinsic Value Calculation

Backlogs have a direct relation with sales, earnings and cash flows. Increase in backlogs will increase earnings, sales as well as cash flows, which will eventually give boost the stock price of the company. Therefore, I believe that the multiple based valuations will be appropriate in order to compute the intrinsic value.

As shown in following table, the company is undervalued based on all the multiples except the price-to-cash flow ratio. The company's operating cash flow was negative for the trailing twelve months therefore; its price-to-cash flow multiple reaps unreliable results. The company's CFO trailing twelve months CFO is negative as the company reported negative figures in 1Q13 and 4Q12 (as the company's account receivables increased, payables declined and other operating activities dipped).

In the base case scenario, I have assigned 30 percent weight to each of the ratios, price-to-earnings and price-to-cash flow, as these two multiples give a clearer picture of the company's financial position. I have assigned 20 percent weight to each of the remaining to multiples. Using different weights, intrinsic value of the stock is calculated as $34.04, which gives a capital return of 50.47%.

In the best case scenario, I have assigned less weight to price-to-cash flow as the Tutor Perini is overvalued according to this multiple. By assigning more weights to the remaining multiples, the fair value of the stock is $41.62, which gives an upside potential of 83.12%.

The company's operating cash flows are negative, which is the reason for the negative price-to-cash flow ratio. It is very difficult for the company to manipulate cash flows. Moreover, the company is overvalued according to the price-to-cash flow multiple. Being more prudent, I have assigned 50% weight to the price-to-cash flow. By assigning different weights to other three multiples, intrinsic value of the stock is calculated at $24.79, which gives a 9.60% upside potential.

Final Call

The company witnessed a strong increase in its backlog over the last couple of years. Tutor Perini is cheap on the basis of multiples and enterprise value-to-backlog ratio. The company's enterprise value is lowest among its peers while backlog is the highest among its competitors. Therefore, its enterprise value-to-backlog ratio is the lowest, which indicates that the company is undervalued according to this multiple.

Backlogs confirms the company's ability to generate revenues in the future. Strong increase in the backlog during the last couple of years indicates that the company will be able to generate higher revenues as well as higher margins in the future. Therefore, I would suggest investors to consider Tutor Perini a decent investment opportunity.

(click to enlarge)

SOURCE: YCharts

In addition, the company missed analysts' earnings consensus by 6 cents in the most recent quarter, which led to a price decline in the market. The company announced earnings of $0.49 a share for the third quarter. As shown in the following graph, stock price on Nov. 4 2013 was $22.85, whereas the stock is currently trading around $22.6. Therefore, I think it is an appropriate time for the investors to a take long position on the stock.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1861351-tutor-perini-a-strong-backlog-and-investors-skepticism-have-made-this-stock-an-all-case-winner?source=feed

Aucun commentaire:

Enregistrer un commentaire