Larry Summers gave a short speech a week ago praiseworthy for its attack on cyclical thinking, and it has been creating plenty of buzz since. Summers hypothesized that the economy had been experiencing a bout of prolonged stagnation well before the financial crisis hit five years ago.

His train of thought is simple. We experienced a series of "bubbles" in stocks, real estate, commodities, corporate profits, and perhaps bonds over the last two decades. But, there was very little in the way of "overheating." In other words, despite unprecedented expansion in credit, asset prices, and employment, inflation has not been a problem since…well, perhaps since the Great Stagflation of the 1970s.

Not only has inflation been soft, but GDP has failed to reflect the credit and asset bubbles. The subpar economic recovery since the crisis, therefore, is not merely a cyclical-level failure. It is only the latest incarnation of what he calls a "secular stagnation," but which (since I have been trying to redefine "secular" for my own purposes in recent articles) I will call the Great Stagnation.

(click to enlarge)

Paul Krugman doesn't think that Summers is all that far off. He suspects that in the midst of this Great Stagnation, it was the bubbles that kept us going. In an economy characterized by consistently depressed growth, a bit of bubbly makes things feel a bit better, even if it doesn't really solve the underlying problem.

Summers concluded his speech by encouraging his audience to think in the coming years whether or not a zero interest rate policy exacerbated the stagnation if the "natural rate of interest" was negative and what kind of policies that would imply moving forward.

Krugman is calling this the Summers/Krugman/Hansen hypothesis. Since that doesn't roll off the tongue so well, and it will be a nuisance typing again and again, let's call it the "SKH hypothesis."

Problems With Summers & Krugman's Argument

I think the SKH hypothesis is clever but deeply problematic for a couple of reasons, but primarily because it creates as many quandaries as it eliminates.

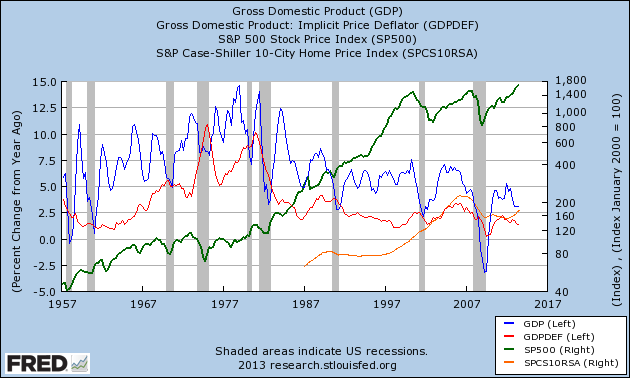

For one, it implies that we went from a Great Stagflation lasting up until the very early 1980s and then, with a very short intermission, slipped into a Great Stagnation. In other words, since at least the 1960s, the last fifty years have been marked by deep systemic imbalances moving from one sustained extreme (high inflation, high unemployment, high GDP, weak stocks and bonds, stable credit growth) to another (low inflation, low unemployment, low GDP, strong stocks and bonds, excessive credit growth). That suggests that Summers's audience should be thinking about more than just what to do when the natural rate of interest is in "secular" decline, but why that decline might occur in the first place.

This line of attack also makes one wonder what the connection between financial markets and the real economy are. As Summers rightly points out, on the cyclical level, it is easy to make the connections. In a cyclical crisis, the yield curve flattens, oil spikes, stocks fall, unemployment rises, GDP falls, industrial production falls, and so on. That does not mean we know precisely how these factors interact, but there is a fairly clear pattern.

Above and beyond the cyclical level, however, there appears to be almost no relationship. Asset prices and employment bloomed while GDP and inflation wilted. But, there is a certain symmetry to be found between the Great Stagflation and Great Stagnation that makes one think that there is a deeper underlying relationship between these factors.

From my perspective, to a certain extent, lumping all of these trends together seems to conflate what I call "structural" and "secular" effects, but in order to keep this article relatively neat and tidy, I won't burden it beyond simply noting my idiosyncratic bifurcation (or trifurcation, if you include the cyclical level) between secular and structural. Rather, I will just mention a few themes that I think suggests that this SKH hypothesis is right in a certain respect--there are much more important things to take note of beyond the cyclical ups and downs of a set of economic factors--and wrong in another--that financial bubbles 'saved' us from the worst of chronic stagnation.

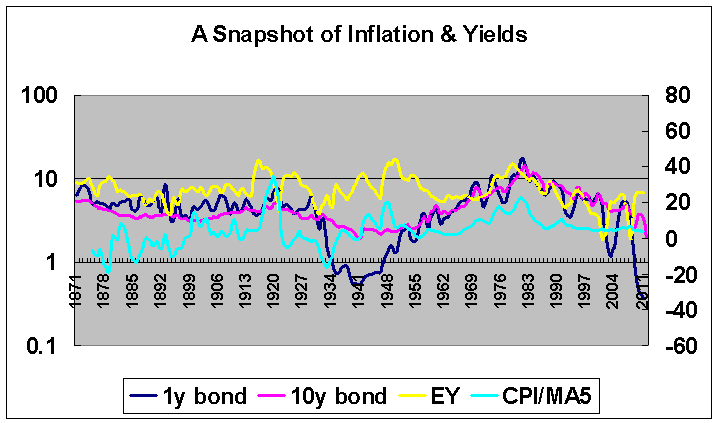

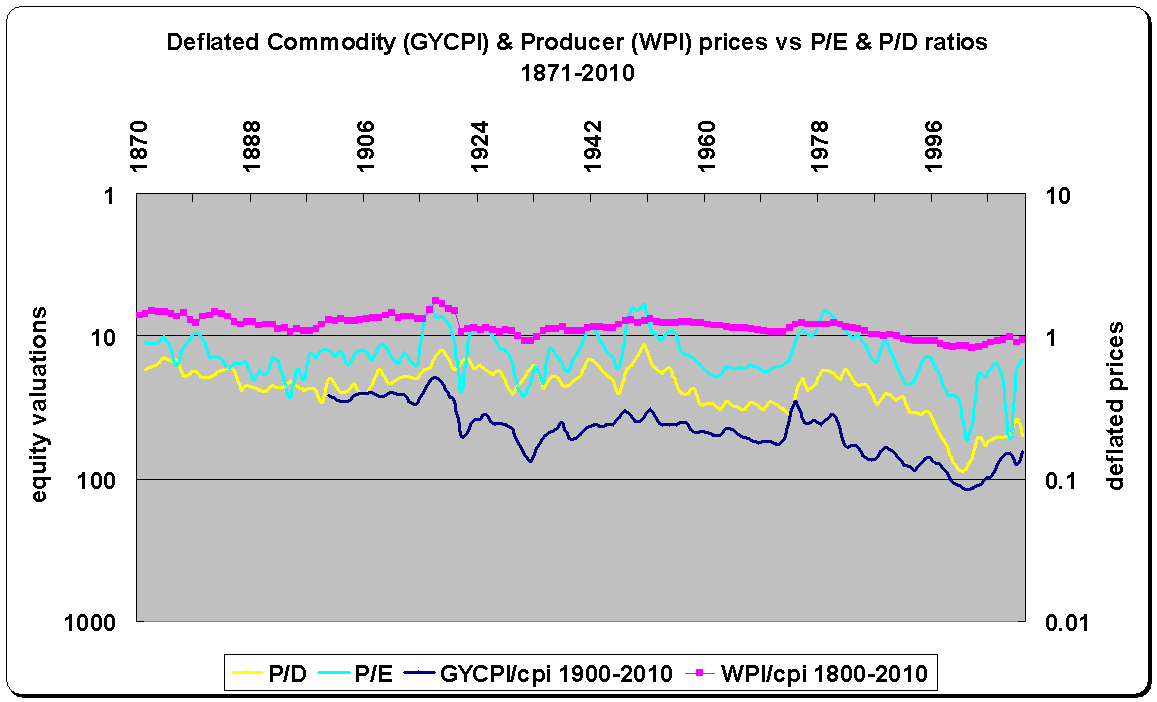

This might best be summed up by noting the rise of the domination of the earnings yield since World War II. Quite simply, the earnings yield (the inverse of the P/E ratio) appears to set the tone for a number of the factors mentioned above: for commodity prices, inflation, unemployment, stocks, and interest rates.

(click to enlarge)

(click to enlarge)

(Source: Shiller, Pfafenzeller, Jastram)

The relationship between commodity prices and the earnings yield goes back as far as we have reliable data for the earnings yield, and it appears to go back centuries before that. It is only a matter of time before that connection is accepted. What is somewhat newer is the connection between inflation and the earnings yield. That only goes back a little over a century and is part of what Friedman called the shift "from Gibson to Fisher." It is also, incidentally, much stronger than the relationship between inflation and interest rates.

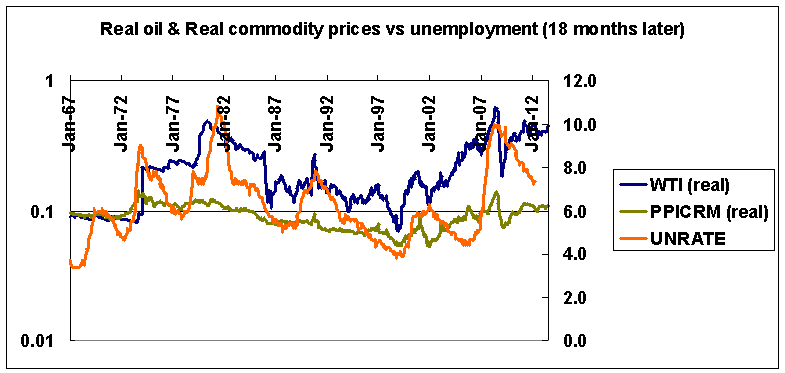

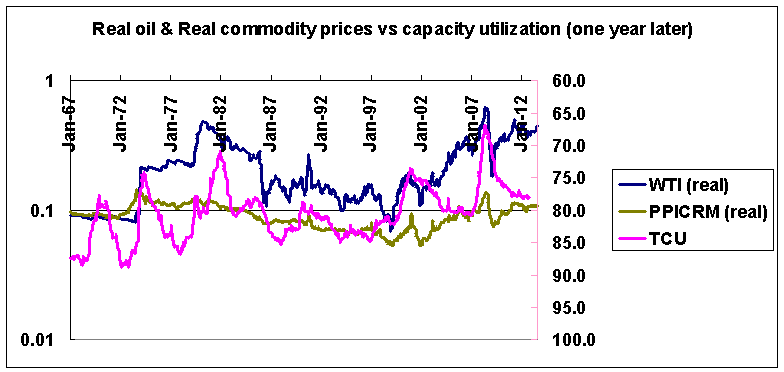

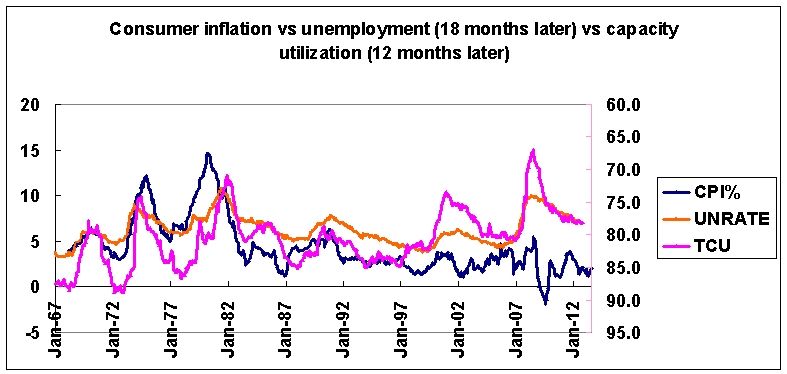

In any case, prior to the shift described by Friedman, according to the Phillip's Curve, inflation and unemployment tended to have an inverse relationship, but since the Curve exploded, inflation (and real commodity prices) has tended to foreshadow the rate of unemployment by two years. In other words, unemployment tends to track the earnings yield at the secular level. One could make a similar statement regarding capacity utilization.

(click to enlarge)

(Source: All data here on out from St Louis Fed)

Although capacity utilization has shown a long-term tendency to fall, if we separate the long-term trend and the cyclical ups-and-downs, it seems to exhibit a similar sort of pattern to the earnings yield, commodity prices, unemployment, etc.

(click to enlarge)

Painting in broad strokes, we can say, therefore, that rising stock prices can be associated with falling commodity prices, disinflation, falling unemployment, and falling interest rates. That is certainly a simplification of things at the secular level, but not a terrible oversimplification.

(click to enlarge)

In other words, the SKH hypothesis suggests that insofar as these financial bubbles and employment have failed to lead to "overheating" in terms of inflation and GDP, we should consider trying to burrow further beneath the subzero natural rate of interest in the hopes of rejuvenating a consistently stagnant economy. More simply, in light of this perennially falling natural rate of interest, stimulus can be amplified and/or maintained for much longer than we had previously thought. And remember, Summers was, relative to Janet Yellen, considered hawkish on stimulus.

This brings us, of course, to the hot topic of QE. Depending primarily on a given analyst's bias, it seems, QE is credited with propping up this or that market or economic variable. At present, popular opinion seems to hold that equity markets are being propped up by QE, although others insist that QE has or is or will once again reflate the prices of gold and silver or inflation more generally. For his part, Summers credits QE with warding off another Great Depression.

My personal opinion is that this is all pretty idle speculation, but let's suppose that the broad consensus is right: QE is propping up asset markets and preventing the economy from keeling over and dying in a deflationary seizure. If the connections I drew between the stock market (more precisely, the earnings yield) and the real economy are right, however, there is something slightly wrong with this.

If QE is propping up stocks, it is also pulling down inflation. To repeat: the relationship between the earnings yield and inflation, whether strictly causal or not, is pretty clear. "High" P/E ratios have always coincided with low inflation or deflation at the secular level. So, if QE is going straight into the stock market, it is almost certainly going to push inflation down.

That would likely result in a feedback loop. As long as inflation is weak, QE can be expected to remain intact in some form or another, pushing up stock prices. Rising stock prices would then push inflation down. Falling inflation would invite continued easing, pushing stocks higher, thus bringing down inflation, and so on.

The cyclical factor would come in at some point, assuming a larger structural factor didn't bring that sort of madness down first. A cyclical rise in inflation will have to occur sooner or later. It is difficult to say at this point, but one imagines that it will tend to be relatively weak, and if the Great Stagnation way of thinking becomes the theme of economic orthodoxy over the next decade, it would probably ignore this signal in favor of keeping the throttle open. Why?

As I have written about in previous articles, changes in the secular disposition of the earnings yield, commodity prices, and inflation come about with little warning or explanation. If we assume that there is a lower bound to that yield (or, an upper bound to the P/E ratio), at some point it must reverse, perhaps back up to levels last seen in the late 1970s.

If the Fed's default mode were to regard a bout of inflation as cyclical until proven otherwise, it could sit on its hands for quite some time before realizing that the market mode had switched from "secular stagnation," as Summers puts it, to some other secular disposition. Just look at how long it has taken for economists to acknowledge the importance of the secular. Summers is being applauded for being the first to identify a trend that he says has been in place for decades. What are the chances that the smart people (and Summers is purportedly one of the smartest) will be able to distinguish a cyclical jump in inflation from a secular one when it occurs? What are the chances that they will know which tools to use to keep it from becoming another Great Stagflation? What are the chances they will know how to use those tools in a timely and efficient manner? What are the chances that these secular shifts are completely beyond the realm of their control?

The good news about Professor Summers speech is that it may bring greater awareness of the importance of the secular aspect of markets, but it could also be a great opportunity for misadventure when we eventually move back into a future of falling P/E ratios, one imagines no later than 2020.

For now, though, what does this mean for markets today? I think it means that when people say there is a "bubble" in stocks (SPY, DIA, QQQ) because weak inflation, commodities (GSC, GLD, SLV), emerging markets, and GDP tell us the real economy is stagnant, they might have things perfectly backwards. This inverse relationship may be artificial and unsustainable over the long run, but over the course of a secular run, a bull market can go on for years and years.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1861581-summers-and-krugman-on-bubbles-and-the-great-stagnation?source=feed

Aucun commentaire:

Enregistrer un commentaire