Have you seen the headlines lately? It seems that your plan to try to drive up the share price by claiming that your foundries are open to "anybody who can use leading edge technology" has backfired. Indeed, after spending the last several years trying to prove that you guys have what it takes to really win in the mobile market with IA, you essentially admitted that your plan may not work.

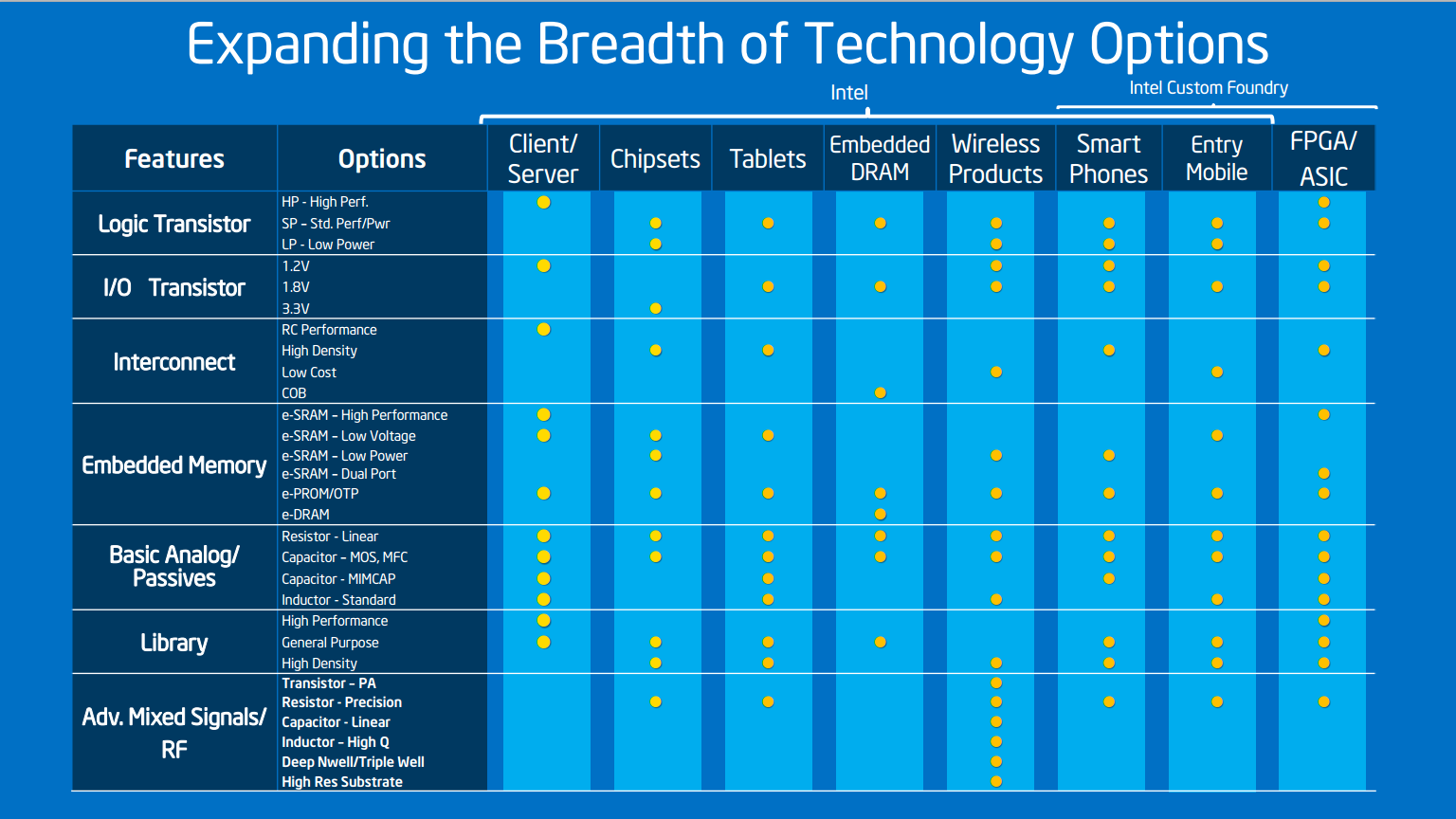

Now, it'd have been easy for me to dismiss this as posturing to shut-up the bears (who don't want to see Intel (INTC) strong and powerful) who just want you to be a foundry since they don't believe in your product design teams, but Mr. William Holt presented a slide that I simply could not ignore:

(Click to enlarge)

With this slide, you are essentially admitting that you would be willing to build smartphone/entry mobile chips for other players. By definition, this means that you would be willing to build chips for competitors to the absolutely brilliant design teams that you have in-house.

Now, I realize that you may simply be trying to attract Apple's attention since it is unlikely that Apple will drop its own ARM (ARMH) based chips. Indeed, building chips for Apple would probably be a nice piece of business that would immediately drive up the share price. However, in the Q&A session, Mr. Brian Krzanich made it clear that he'd be open to a deal with just about anybody if it made sense for the shareholders.

That's The Rub, Isn't It?

Surprisingly enough, you have very few truly vicious competitors in the smartphone space: MediaTek and Qualcomm (QCOM). Every other player is either weaker than you are in this space, or simply irrelevant. Indeed, according to Strategy Analytics, the top five apps processor vendors by revenue were the following:

| VENDOR | MARKET SHARE |

| Qualcomm | 53% |

| Apple (AAPL) | 15% |

| MediaTek | 11% |

| Everyone Else (including you) | 21% |

It's clear that if you were to do smartphone foundry business for anybody, and for it to actually move the needle, you'd need to either do work for Qualcomm or Apple (since MediaTek isn't likely to pay for premium-priced wafers). Further, most of Qualcomm's volume is at the low/mid-range, which means they're not going to pay a premium for wafers when they're trying to do battle with MediaTek, Allwinner, and Spreadtrum. For Qualcomm's high end smartphone parts, leading edge node would make sense, but then that would encroach upon the "tablets" portion of your chart. Ditto goes for Apple and its A-series processors.

The real problem here is that by even hinting at this, you've signaled that Intel isn't confident that it can take meaningful market segment share in smartphones. Now, I don't actually believe that, but think about how easily the Street is fooled into thinking things?

How hard was it to convince them that "X86" wasn't a barrier to a low power micro-architecture or Android based devices? How hard has it been to convince them that you can do competent graphics processors? There are still sell-side analysts who don't believe that you have what it takes to win in this space and now you've given them more reason to doubt you!

There Was No Need - Your Roadmap Looks Excellent

Perhaps I am more bullish than even you seem to be, but the roadmap that you presented was highly compelling in phones. I don't want to rehash what I already wrote in my piece, "Intel's Mobile Roadmap Is Incredibly Strong", but the bottom line is that the roadmap suggests that you could have smartphone apps processor leadership by 2H 2014 and certainly by the time Broxton comes out in mid-2015.

While I believe that your architecture guys are top-shelf, they are given an enormous advantage thanks to your 14 nanometer process which, according to Bill Holt, should be an entire generation ahead of the foundries' "16nm" processes. The laws of physics cannot be broken, and in the hands of a capable design team, Intel should finally achieve leadership here.

Why give up on the cusp of victory? If your roadmap is on target, then handset and tablet OEMs will have no choice but to use your processors. You are clearly aware that every high end handset uses Qualcomm today (because its products are the best), but those orders could all be going to you if your product is superior. In a highly crowded market, no handset OEM is going to want a sub-par chipset.

Stay The Course

Stay the course. I realize that Intel's business is uncertain as the PC continues its decline, but Intel will make it through this as it has made it through many other transitions in the past. You have the engineers, you have the sales teams, you have the brand, and you've got the process technology and software secret sauce. The ingredients for victory are all here.

Don't give up your IDM advantage to pursue low margin foundry business. I can understand if - as David Wong pointed out - you want to get a "fruit in your foundry" in order to boost investor sentiment, but if you do the math, you'll realize that you can make a lot more money by having the world's best applications processors and modems. Heck, you can make more money selling RF/baseband to Apple than you would building Apple's A-series chips. Of course, Qualcomm will be tough to displace, but the point is that Apple is just ~15% of the smartphone market and shrinking.

Go for the other 85%. Playing foundry may seem lucrative, but selling chips that you build yourself is even more profitable. You can have Qualcomm's design margin as well as Taiwan Semiconductor Manufacturing's (TSM) foundry margin. Your investments over the last several decades have made it so that you can have your cake and eat it, too. Don't throw this away to satisfy short-term traders who don't understand your business or long term investors who don't understand just what it is that makes Intel one of the greatest companies on this planet.

Disclosure: I am long INTC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

from SeekingAlpha.com: Home Page http://seekingalpha.com/article/1861301-open-letter-to-intel-stay-the-course?source=feed

Aucun commentaire:

Enregistrer un commentaire