The fragile five or shortly BIITS, consists of Brazil, India, Indonesia, Turkey, and South Africa. These five economies have some vulnerabilities in common: High inflation, weakening growth, large external deficits. Some of them are more dependent on China's economic success, some on Fed's printing process.

In this article, my aim is to focus on macroeconomic outlook for these countries, how troubled the currencies are, and the markets in general. I prefer to go country by country.

Brazil

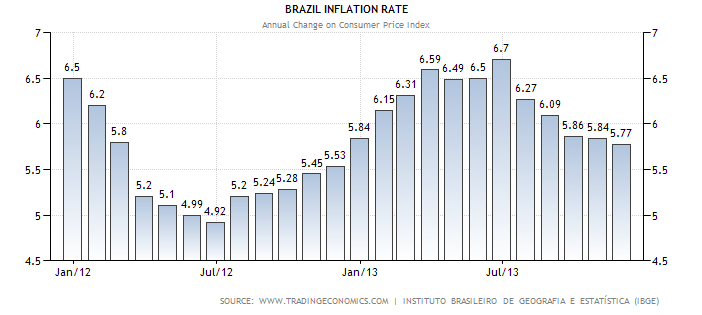

Brazil has been a consistently growing economy throughout the 2000s. Excepting the global recession era of 2008, the economy grew at a average pace. However, since 2010 the economy has apparently turned into a more volatile one. Being ranked 6th in the world in total GDP, Brazil was absolutely a success story but unexpectedly concerns around its sustainability began to rise.

The GDP in Brazil contacted by 0.50% in the third quarter over the previous quarter meanwhile the annual growth is 2.2% which is an unsatisfying number for an economy that averagely grew by 3.11% fro, 1991 to 2013.

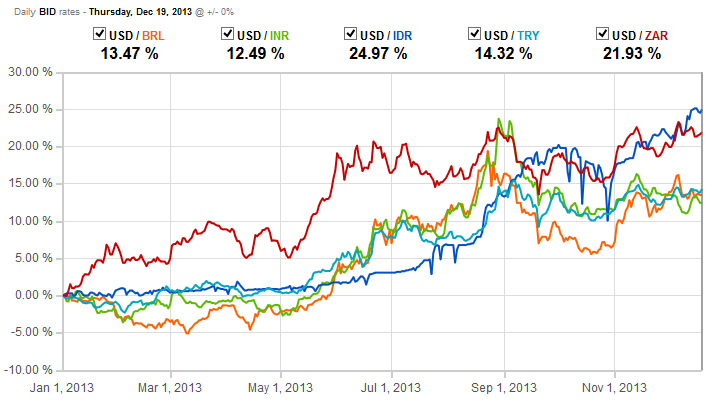

The biggest challenges for the economy is the inflation and the widening current account deficit. Consumer prices index hit the record highs in the middle of year, then showed the tendency of cooling down. On the current account side, the numbers began to deteriorate following late 2000s financial crisis. As a result, the Brazilian real has depreciated by 14.7% against US dollar year to date. This is important when you invest in an asset in Brazil, because you may suffer a remarkable loss even if the asset you invest in gains value in term of local currency.

(Click to enlarge)

(Click to enlarge)

Another alarming point is that the FX reserves of the country is melting, which dropped to $362 billion in November from $379 billion in April. It is generally accepted that a decline in FX reverse to current account deficit ratio is pre-indicator for the currency crisis. In Brazil, I see a progress on inflation but the current account developments is worrisome, as the Real remains weak despite the sale of FX reserves.

India

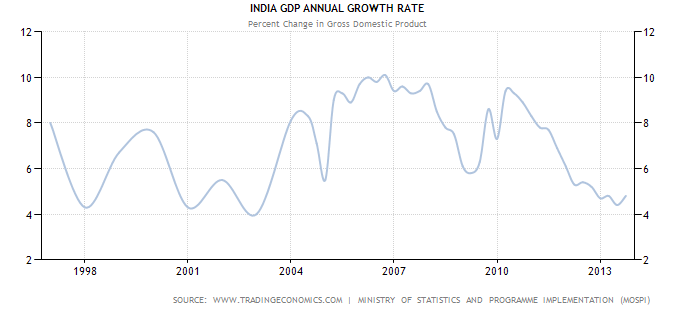

India is another success story and with no suspect it deserved to be one of the component of BRIC, when investors were more optimistic on emerging markets in the beginning of 2000s. The economy could sustain its positive growth rates even during the global recession.

(Click to enlarge)

But the picture darkens when we focus on the economic performance of the country during the recent periods. Firstly, I would like talk about the weakness of the currency. India was the country that hurt most because its depreciating current among emerging markets this year, the rupee is down by 25% year to date. This is what an investor should consider fist while investing in Indian assets. India's central bank sold US dollars directly to the market and raised the interest rates to prevent the depreciation of its currency.

In fact, India's problems has structural drivers that we should pay attention. With a population over one billion, the current policy by the government is kind of a ride that hardly end well. Therefore, I think a change is needed in the political environment. I guess the pro-reform president candidate Narendra Modi's winning the elections could a pretty story to buy.

Indonesia

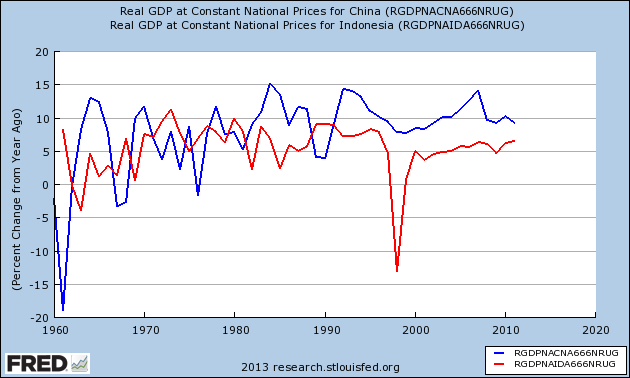

Talking about Indonesia, it is necessary to talk about the macroeconomic model. The local manufacturing companies are dependent on imported capital and intermediary goods from China to expand their business. This interdependence relationship is really strong between two countries from a business cycle perspective. GDP figures of both countries suggest a nice correlation as shown below.

(Click to enlarge)

In my opinion, this dependence is such a weakness, however, it is reasonable to be bullish while China continues to grow at a fast pace.

A currency depreciating by 12.5%, real GDP growth rate of 5.6%, consumer prices annually increasing over 8%, and current account deficit to GDP ratio of %3.2. This is the simple quantitative summary of Indonesia. The Indonesia central bank has helped much to prevent the rupee from depreciation by raising interest rates this year. Being backed by imports to China, the Indonesian economy won't slow down.

Turkey

Turkey is a consumption-driven economy, and like every other consumption-driven economy, it has vulnerabilities arising out of widening current account deficit. The Central Bank of Turkey is running an unorthodox policy to put some pressure on consumption through its impact on credit growth. Financing the current account deficit is a major concern in the economy. The compositions of flows is particularly dependence on portfolio and short-term debt flows rather than foreign direct investments.

(Click to enlarge)

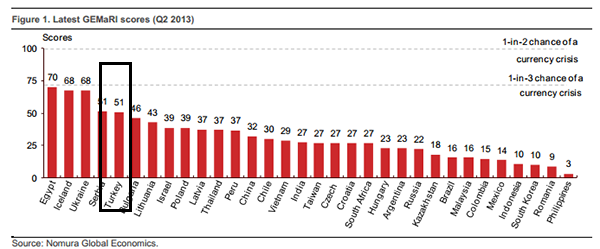

Nomura is publishing Global Emerging Markets Risk Index scores, which casts light on the underlying fragility of each emerging market (see the chart above). What the index is showing that Turkey is the closest economy to a currency crisis among the fragile five.

Another issue is the political risk. Turkish politics may become the top focus for the country's investors. Recently sons of three ministers in cabinet, CEO of a state-owned bank were detained in a corruption (and this is why iShares MSCI Turkey ETF (TUR) collapsed). Good quality management, respectable corporate governance, good corruption rankings were making investors prefer Turkey.

Turkey has a good potential to be a key market in the future, however, it is a good idea to stay away for a while.

South Africa

The final member of the BRICS demoted and join the club of fragile five. Like its peers, its flaws got more clear.

Mining industry is the main driving force behind its economy. Under these circumstances, the prices of industrial metals are coming into prominence. Trade balance of country breaks down amid the weakness in prices of industrial metals. This connection makes South African rand vulnerable.

One reason to stay positive, South Africa's central bank is the only one that hasn't raised rates on the fragile five. It has still room the raise the interest rates that may keep the currency strong.

The Bottom Line

(Click to enlarge)

There always will be lucrative opportunities in emerging markets (EEM). On the other hand, the ones who invest in these markets, should never forget that they are risky. And after Fed stops easing, they are even more riskier. Then it is being more selective time.

Above, I shared my ideas to form opinions about the markets that the market call "fragile". Finally, I think India (OTC:IHDUF) and Indonesia (EIDO) are the best picks among them and sentiment towards to Brazil (EWZ), Turkey(TUR) and South Africa (EZA) is likely to sour even further.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire