Dividend Growth Investing has become a popular retirement strategy which helps investors focus on consistently building up income streams instead of trading volatile share prices. While some typical dividend investors focus on finding the largest possible yield, dividend growth investors look for stable companies with a history of annual dividend increases - and such dividend hikes are even more attractive when exhibiting high relative growth.

The strength of such a strategy, in my opinion, has little to do with the total returns or even the sustainable retirement income. I have modeled hundreds of strategies and many of these can compound your investment capital quicker; at which point you can simply buy these same 'dividend growth' stocks at retirement with a larger total income stream than someone who didn't stray from the DGI strategy throughout their entire investment period. No doubt, doing this would be a topic of debate amongst the dividend growth community.

The power of dividend growth investing, I feel, is that it helps an investor to invest with discipline in bad markets when stocks are cheap. Focusing on income and dividends when share prices drop, particularly the attractive yields of stocks which have a history of increasing dividend payments (as opposed to a high trailing yield that dissipates at the first sign of trouble), is just plain smart.

That being said, the question needs to be asked: are dividend growth investors holding the reigns too tight? Are they being overly strict with their stock selection?

Is Dividend Growth Investing Too Strict?

One of the basic principles of dividend growth investing is that each year the dividends must increase. But what if we slackened the rule so that we would also have stocks which may have held the dividend between years - but never lowered it? By demanding that companies increase the dividend every year, even when it may not be economically advisable, are we being too strict with our stock selection?

To test this, I will use the Portfolio123's stock screening and backtesting software to determine whether we should be including this group of stocks or not.

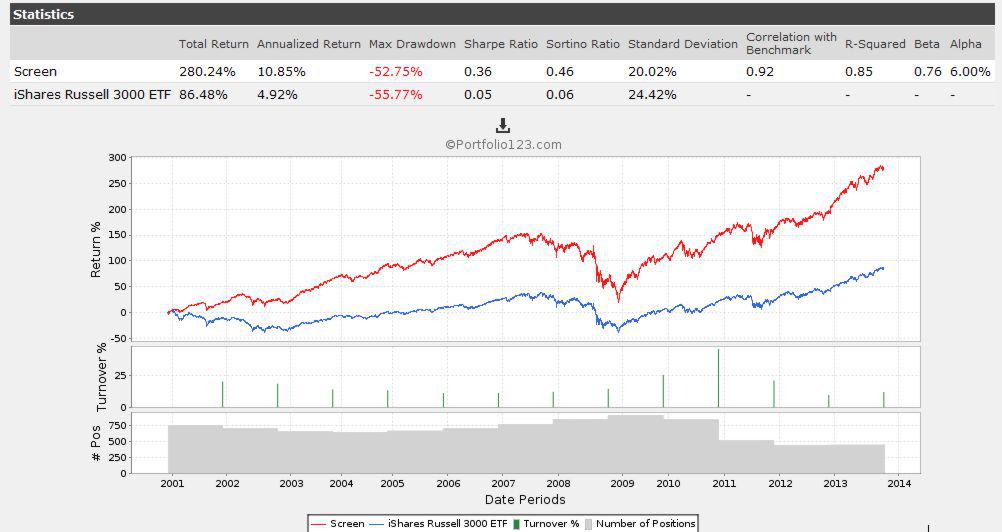

Dividend Growth Benchmarking

In order to test this, we will first create a couple of DGI benchmarks. The first is to test stocks with at least 4 years of dividend growth and the second is for at least 9 years of annual growth. We will rebalance one every 52 weeks. This will be charted in red. The blue line will be the iShares Russell 3000 ETF (IWV).

Dividend Growth Stocks (4 years +)

(click to enlarge)

Dividend Growth Stocks (9 years +)

(click to enlarge)

From here we can deduce that dividend growth investing has slightly less downside risk than the market. The maximum drawdown of the dividend growth portfolio was roughly 3% less than the selected benchmark. The returns in both instances (4 and 9 years of growth) were greater than the benchmark. As well, it seems that buying into these dividend growth stocks earlier (4 years of increasing dividends) is better (than 9 years of increasing dividends).

To test this theory we will run another screen that will hold stocks with more than 4 years of dividend growth but less than 9.

Dividend Growth Stocks (4 - 9 years)

(click to enlarge)

We see the long-term CAGR rises significantly. On closer inspection, however, there is little change between the above 3 charts when looking at the period from 2010 to current. The question could be asked if the additional alpha of the '4 to 9 years of dividend growth' is being masked in a bull market or whether there is no additional alpha between the various subsets of dividend growth and the extra return was an anomaly limited to 2001 - 2008. That is a question beyond the scope of this article to be considered in the future.

Discarded Dividend Growth Stocks

In these three charts below we will compare dividend stocks which either held or increased dividends annually, where at least one year had a dividend that stayed the same. This subset of dividends stocks will have no overlap with the traditional dividend growth universe as these would be in the 'discard pile'.

We will consider this group with at least 4 years, 9 years and only 4 to 9 years of dividend history where no subsequent year paid out less than a previous year.

Non-Decreasing Dividends (4 years +)

(click to enlarge)

Non-Decreasing Dividends (9 years +)

(click to enlarge)

Non-Decreasing Dividends (4 - 9 years)

(click to enlarge)

It is not surprising that we find the maximum drawdown increasing. Some may take this as a lack of management confidence in the ability to pay such dividends going forward. There is likely weaker companies in the mix which often fall harder in bear markets.

On the other hand, was this increase in drawdown warranted? The overall returns of this subset of dividend stocks is greater than the stricter dividend growth universe. There may be some discarded gems in this pile that, once removed, may actually improve our downside risk in bear markets.

Discarded Gems Strategy

Next, I will create a strategy rebalancing every 26 weeks that selects the 'best 15' stocks from the discard pile that had at least 4 years of dividend history... where no year had a decrease, but where at least one year held the dividend the same.

The 'best 15' stocks is built on a ranking system that I developed which grades value based on as earnings yield, dividend yield, price to sales, price to cash flow, price to book and total enterprise value including half a dozen other metrics.

If you are using the Portfolio123 screener, similar results can be had using the All-Stars: Greenblatt or the Comprehensive: QVG (Quality/Value/Growth) ranking systems which are provided. I will add a 0.20% slippage factor to simulate some market impact. Below is the simulated returns since 2001 holding 15 stocks equal-weight.

(click to enlarge)

Let's have a quick look under the hood to see two stocks this model is recommending.

ConocoPhillips (COP) - This stock is listed by some dividend growth investors as having 13 consecutive years of dividend growth. The dividend history of COP suggest that dividend growth was flat from 2011 to May 2013, which would have broken their dividend growth record. On closer inspection, the spin-off implications may still keep this as a dividend growth stock after all. Note the comment David Fish made on a COP spin-off article:

"Whenever a company has a spin-off, I apportion the dividend history at the same rate as the pro rata distribution of share price, which is generally finalized in accordance with the first day's trading. So, for example, if a stock priced at $50 had a dividend of $1 per share and the spin-off is pegged at 25% of the investors' basis, then the main company would be priced at $37.50 with an immediately prior dividend of 75¢ and the new company would get a basis of $12.50, with an immediate prior dividend of 25¢. So if the parent declared that it would be paying $1 the next quarter, it would represent an increase from the 75¢ previous payment."

At any rate, most screeners programmed for dividend growth will disallow this stock whereas loosening the restrictions will add let this gem in. ConocoPhillips is a buy in with my 'Discarded Gems' model.

Hewlett-Packard (HPQ) - Hewlett-Packard had a decade worth of paying 32 cents per share in annual dividends until mid-2011 when it changed its policy and increased dividends. This stock has 2 or 3 years of dividend growth and would not make any long-term growth list, but the long-term dividend record without annual decreases would make this a candidate for the 'discarded gems' model.

What might make this a stock worth considering? The consensus expectation for FY 2014 is listed at $3.66 per share (Yahoo Finance) which gives the stock a forward earnings yield of 7.65, which seems a bit low despite some softness of late. I would put HPQ on your radar as a potential 'discarded dividend growth' value play.

Beware Of Value Traps

Below is one dividend stock that has a history of dividends that did not decrease annually. It did not make it into my 'top 15 model' for the reasons below.

Windstream Holdings (WIN) - I wanted to highlight this stock because of its whopping big dividend yield. But a second look will show you why this never made it into my model. First off, the payout ratio is at a whopping and unsustainable 526%. This puts the forward dividends in question as does the trailing PE ratio of more than 38. Despite the big sounding dividend, shares are down over 30% over the past 2 years while the S&P 500 ETF (SPY) rose over 46%.

Then you look at depreciating book value from December 2011 which was around $1.5 billion to today which is $854 million and add to this that quarterly capital expenditures have fallen from $307 one year ago to $193 million now - and add in strongly negative trailing and forward 5 year earnings growth - I would call this a dividend value trap.

Conclusion

It is my view that dividend growth investors should widen the net to include stocks that have not decreased dividends annually. There may be good stocks getting thrown in the wastebasket alongside the not-so-good. The higher annual returns show this to be true, although the larger drawdown also shows that many undesirable stocks are in the mix.

It is my opinion that investors considering stocks which have not decreased dividend payments annually need to be much more judicious about which stocks they will and won't accept and should have some sort of fundamental ranking or scoring system to weed out bad stocks and retain the ones with higher potential.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire