It is my belief that shares of Imagination Technologies (OTCPK:IGNMF) are meaningfully undervalued. While the shares are down on near-term weakness (in particular, the slowing growth in high end handsets and share-loss at the lower end of the GPU IP market), it is my belief that the shares are at or close to a bottom and will trade meaningfully higher over the next 6-12 months. While you can find my full thesis here, there is one particular aspect of the Imagination story that I would like to focus on that could prove to be the long-term "game changer" from a market share/unit perspective, at least in its core graphics business.

The Graphics Share Problem: Qualcomm, ARM, and Apple

Some of the biggest overhangs to Imagination's business have been the following key drivers:

- The exit of several licensees from the mobile SoC space in light of Qualcomm's (QCOM) (which does not use Imagination GPU IP) increasing dominance (e.g. Texas Instruments (TXN), ST-Ericsson).

- Competitive pressure from ARM Holdings' (ARMH) Mali GPU IP, particularly at MediaTek.

- The signs that Apple (AAPL) - one of the largest licensees of high end Imagination IP (and Imagination's second largest shareholder) - is developing its own GPU putting 200-250 million royalty-bearing units at risk longer-term.

- The slowdown in the growth of the higher end smartphone market (where Imagination participates more fully than it does in the low end)

However, it is my belief that these headwinds are now priced in and set to reverse over the next 6-12 months.

Intel: The Heaviest Hitter

While Intel develops its own GPU IP, the company will ship its next generation high end smartphone platforms (Merrifield and its mid-life kicker, Moorefield) with Imagination Technologies Series 6 IP (an interesting fact to note is that Intel is Imagination's largest shareholder with a roughly 15% stake). Longer term (i.e. beginning in 2015), Intel's high end tablet/phone SoCs will feature Intel GPU IP, but it is my belief that the company's lower end (and much higher volume) SoFIA products targeting mass-market phones will continue to use Imagination Technologies IP.

The reasoning behind this is actually simple. Intel's GPU architectures are designed to scale from high end phones/tablets all the way through very beefy PC processors with increasingly sophisticated integrated graphics. The trade-offs that Intel is likely to make from a performance, power, and area perspective to support higher end, higher margin parts are likely to not fit quite perfectly with a very cost-optimized, smaller-die solution. This leads me to believe that Intel will continue to use area-optimized versions of Imagination's IP for the lower end of the space.

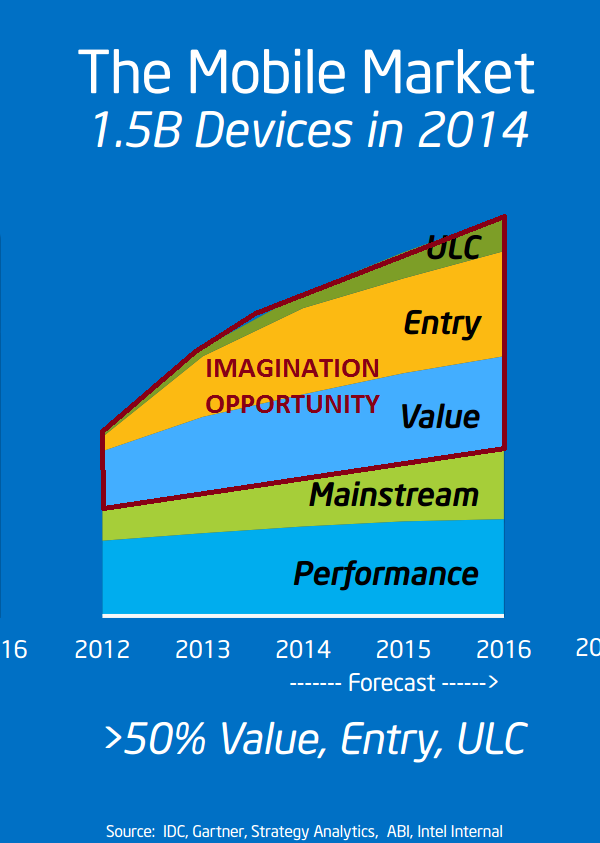

Not only does this save Intel the development effort (the royalty rate here is on the order of $0.20 - $0.25 per chip), but this will allow the company to avoid making trade-offs in its GPU architectures that lead to compromises to higher end performance. What's interesting here is that while Intel's own IP will go into its high end devices, Imagination GPU IP will likely dominate the vast majority of Intel's unit shipments over the foreseeable future if this chart is any indication:

Broadcom: Another Interesting Opportunity

With the acquisition of Renesas Mobile, Broadcom (BRCM) is finally set to ship credible LTE-capable SoCs into the mainstream mobile market (the same market that Intel's chips are gunning for). Broadcom, unsurprisingly, is leveraging Imagination's GPU IP for these chips and is very likely to continue to use Imagination IP going forward (particularly given how aggressive Imagination has been about creating a whole stack of IP for various segments).

What's interesting here is that while both Broadcom and Intel are gunning for this space, it really doesn't matter who wins as long as - in aggregate - they gain back share against Qualcomm which uses internally developed GPU IP as well as MediaTek which appears to be shifting over to ARM's Mali IP.

The Samsung Connection

So, while I've spoken about "share gains" on the parts of both Broadcom and Intel, one thing that's worth mentioning is that Imagination really doesn't have a lot of penetration at Samsung these days. Samsung's own Exynos chips tend to ping-pong between ARM and Imagination IP (and right now, ARM has the win), but only 10-20% of Samsung's products (according to Imagination's CEO) use Samsung's own chips; the rest are sourced elsewhere (primarily Qualcomm).

With Broadcom announcing an LTE win over at Samsung, Imagination is set to gain some pretty decent share over there. Further, on the most recent earnings call, Imagination's CEO Hossein Yassaie made the following remark,

Intel has pretty significant connections into Samsung

It seems pretty clear that Intel will begin to win some meaningful handset designs over the next 6-12 months with its Merrifield/Moorefield products which should bode quite well for Imagination's share in the mobile GPU market.

The Apple Fear

The biggest risk to Imagination at this point is a potential loss of Apple as an IP licensee. Apple has been quite obvious about its intent to build its own GPUs, as shown here,

(click to enlarge)

It's not clear when Apple will announce that its A-series chips have moved to an internally designed GPU (I would guess that the A9 or A10 will have Apple-grown GPU IP), but when it does, it could have a material financial impact on Imagination depending on how broadly and deeply Apple pushes its own GPU.

Conclusion

With Imagination set to gain back some meaningful mobile GPU share, the sell-off in the stock seems wildly overdone. As Intel and Broadcom ramp their next generation platforms over 2014 and 2015, Imagination should see a nice uptick in royalty revenues. The only "ticking time bomb" here is Apple, which represents about 200-250 million units per year. Whether Apple will license Imagination's patents or its video decode/encode blocks or if it'll do its own is unclear at this point, but I am expecting this to be the biggest headwind to what is otherwise a compelling story on the GPU side.

Oh, and the MIPS story is only just beginning, but that's beyond the scope of this note.

Disclosure: I am long INTC, BRCM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: I plan to purchase shares of IGNMF as soon as possible.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire