During the spring and early summer of 2013, the Federal Reserve began discussing its plans for "tapering" its future purchases of bonds. This set off a wave of selling pressure in a range of interest rate sensitive and yield-oriented sectors ranging from long term Treasury bonds to utilities to municipal bonds to mortgage REITs. Along the way, the fixed-income closed-end fund universe was also hit by selling pressure. What makes this potentially an opportunity is that there is a wide variety of fixed income (FI) closed-end funds (CEFs) and that they do not all have the same sensitivity to interest rates.

Perhaps within that inefficient oriented sector, there may be some value, as retail oriented investors reflexively sold everything that looked like a bond, whether or not it was exposed to the risk of long-term interest rates rising or not. It is reasonable to believe that even if the economy continues to expand, and rates rise, that is still a large group of the investing universe which needs to earn yield from their investments -- and perhaps these issues may play a role in that mission. Below are three FI CEFs that may offer value (in terms of a sustainable current yield), without excessive exposure to the risk of rising rates, and a margin of safety if events do not pan out as we forecast.

Apollo Tactical Income Fund (AIF)

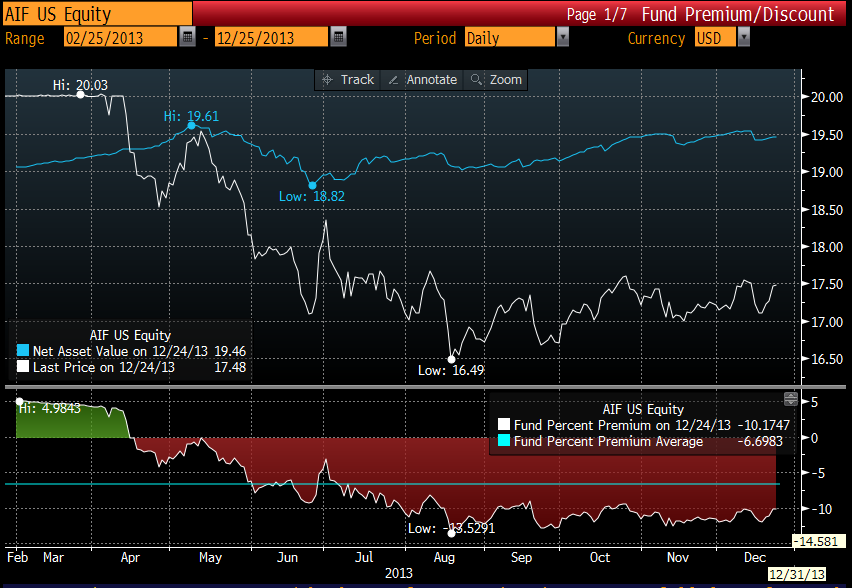

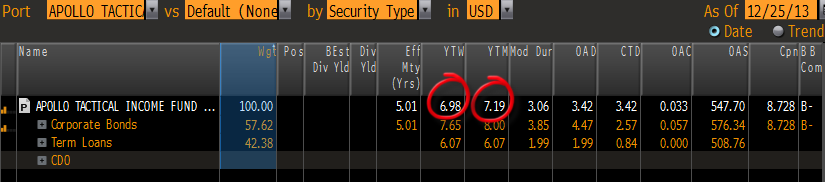

AIF was one of the wretched class of 2013 Fixed-Income Closed-End Fund IPOs, that was swiftly orphaned by tapering fears. AIF offers a near 8% yield with a 9%-10% discount to net asset value (NAV), which is about 3% cheaper than its historical average. There are lots of funds with comparable yields, so what makes this interesting? The portfolio is about 45% High Yield Bonds, 45% Floating Rate Loans, and 10% Collateralized Loan Obligations (CLOs), so when the summer rates squall hit, NAV was hardly dented at all. NAV volatility is unusually low for the yield -- this is a rare feature in a bond fund, and is a function of Apollo's portfolio allocations to floating rate obligations.

Of the universe of 400+ FI CEFs, AIF had one of the very best (lowest) realized sensitivity to interest rates. From May 1 to July 1 its empirical duration was a little over 1. This means that for investors who may fear rising rates, AIF is unusually well protected, and NAV may drop less than other bond funds if the future portfolio behavior is similar to the past. And when combined with the current yield of ~8%, AIF offers one the best metrics for carry per unit of any risk. One can observe in the graph below that the NAV drop when U.S. long rates started rising was minor, especially when compared to core bonds. (click to enlarge)

The portfolio is more concentrated than the typical peer, which is a mild negative, if one didn't think Apollo had some skill in working on the other side of the Chinese wall to make creditor outcomes better, in a way that broadly syndicated loan investor doesn't. If something goes wrong at one of their internally originated credits, Apollo has a chance to work things out that more passive investors don't have. Earnings at the fund cover the dividend, per the last semi annual, but I would not place much weight on that since it was a ramp up period after the IPO. Instead look at the underlying portfolio from their filings which I estimate has a yield to worst/maturity of ~7%, so after leverage of 30% I think a portfolio yield of 8+% is very achievable, so I think the distribution level is safe. A special year end dividend was recently announced which also confirms that the existing portfolio investments are covering the current distribution.(click to enlarge)

There is some leverage (32%) here which is a risk factor. Management states duration (the sensitivity to interest rates) is 4ish, although that didn't seem to hit NAV when 10 year rates (10Y) moved. Another consideration is the portfolio credit quality and the nature of the assets. The investments are primarily in junk bonds and unrated loans, which can become illiquid during times of market stress, and may default during recessions/depressions. The closed-end fund structure is one way of addressing the liquidity issue, but this portfolio will have exposure to recession and economic growth risks. This fund might be considered in replacement of some equity risk; it will not diversify it as much as more traditional, core bond funds would.

Between the robust NAV behavior during the summer, healthy yield and margin of safety in the discount, perhaps the next group of shareholders will look on AIF with more cheer than the IPO investors, who paid full retail price, and have been booking tax losses in recent months.

- Benefits: Yield, Margin of Safety, Low sensitivity to interest rates

- Considerations: Portfolio credit quality, and recession exposure

- A fund card is on the sponsors site

Brookfield Mortgage Opportunity Fund (BOI)

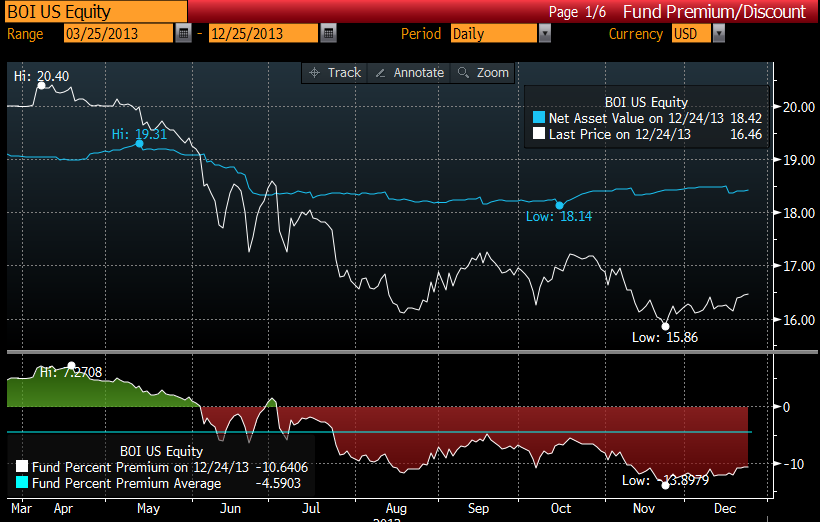

BOI is Brookfield's newest mortgage fund that IPO'd in 2013, and like so many of its classmates, wallows at a discount as the initial wave of investors books tax losses against this name. The fund currently distributes 9.2% and offers a discount to Net Asset Value of 9%-10%, which is about 6% cheaper than normal.

(click to enlarge)

This fund is currently unlevered, but has the ability to lever up its holdings and is slowly doing so. Current holdings are mostly non agency residential mortgage securities and commercial mortgage backed securities; there is also a small sliver of high yield corporate bonds. Recent additions include commercial real estate whole loans, which are less liquid than mortgage securities but may offer better yields and covenants. Duration according to the sponsor's fact sheets is a meager .13 but during the early summer swoon NAV was off about 3%, so I consider the fund to have an empirical duration of 3ish. This suggests that a 1% rise in long term interest rates may cause the portfolio NAV to drop by 3%. Mortgages have had a tough summer as credit spreads widened at the same time rates were going up.

One strength of the fund, in an environment of slowly rising rates, has been its very stable NAV, which can be observed in the graph above. Compared to the mortgage REITs, BOI offers a significant amount of yield without the same level of interest rate risk. For comparison another mortgage vehicle like Annaly (NLY) has had a range in book values from 15 to 12 in the last year, while offering a 12% yield, while BOI's NAV (essentially the same as book value) has been stable, and the yield is 9%. On a risk adjusted basis (yield/book value volatility) BOI seems compelling for those who might consider mortgage REITs at these levels.

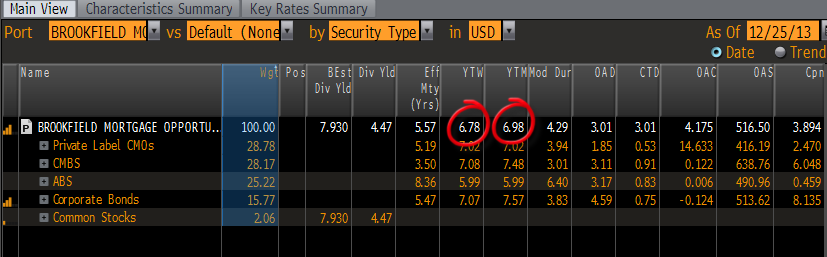

The major negative here are the earnings -- as of the last semi annual -- Return of Capital comprised 1/3 of the distribution. Some of that is due to the ramp up period post IPO when investors cash had been collected, but not yet deployed into an earning portfolio. But also some is due to the fact that a levered distribution was offered when the portfolio is not currently levered. Based on BOI's N-Q filings I think the existing portfolio is earning 7% yield to worst/maturity.(click to enlarge)

Perhaps the fund can grow into the dividend by levering up, or gathering higher yielding assets (they just added a pair of whole loans, which are probably 9% or 10% run rate based on what levels these kinds of loans transact at). The second negative is simply Brookfield, a less than ideal sponsor of CEF's with habits of rights issues, secondaries, etc. The management company doesn't need to be heroes for this to be an adequate investment -- just roll mortgage paydowns into newer higher yielding paper, lever up to peer group levels (most funds are 20%-30% levered) and avoid dilutive actions at the fund level. This is not a widows and orphans vehicle, but perhaps the discount and yield impound the visible problems. Management has been buying in recent weeks which is a bullish signal.

- Benefits: Yield, Margin of Safety, Low sensitivity to interest rates, Possibility of levering up the earnings at some point

- Considerations: Current visibility of dividend coverage, Sponsors history of rights offerings

- A fund card can be found on the sponsors site

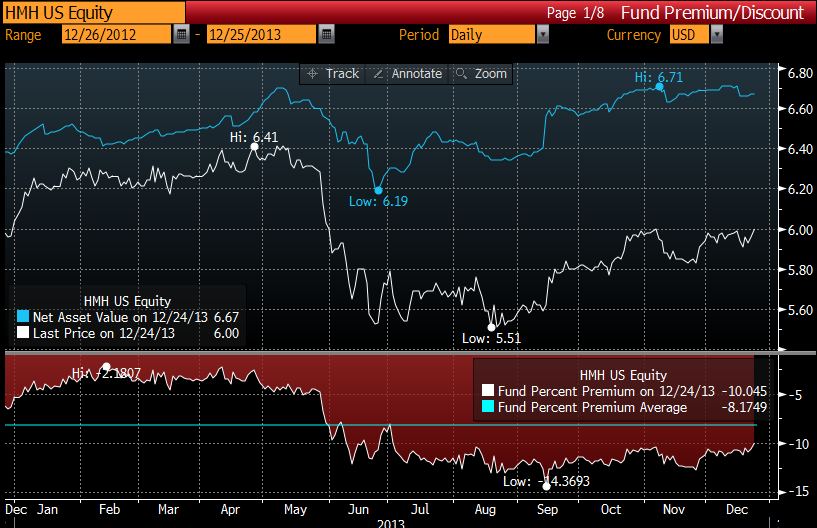

Helios Multi Sector High Income Fund (HMH)

The history of this fund is sad (read this long history of Morgan Keegan Regions Financial ) as they suffered a disastrous loss of capital during the financial crisis. The prior management was sacrificed to the bond gods, and the portfolio was restructured into a conventional levered junk bond portfolio (which might suggest how insane it was before). The fund (sporting a new ticker symbol) is now run by the Boston Brookfield office, which is an improvement over the Morgan Keegan collateralized debt obligation (CDO) specialists from before. The main point to understanding the history is to taste some of the bile that the investor universe has when considering this name, which may account for some of revulsion this fund's deep discount suggests. That being said, dwelling on the past may blind us to future opportunity.

(click to enlarge)

HMH is at an 9%-10% discount currently and offers a monthly 5.25c dividend, which was literally just raised from 4.25c before Thanksgiving 2013. Now here's what makes it interesting -- many of the major data providers are not annualizing the new dividend number, which doesn't seem to be propagated into all the major data feeds. (Morningstar for example is annualizing the old dividend number) The difference is that some data vendors show this as an 8% yielding fund, with an 10% discount, with high fees, and thin trading (so investors rightfully take a pass) However, if one annualizes the new dividend, it looks like a 10.4% yield, with a 9-10% discount. With that blend of yield and discount, investors may find that thin trading and higher expense ratios are a little more tolerable.

The yield on offer is high, so is it sustainable? Going back to the history, the fund was a plaintiff in a range of CDO lawsuits pending from the financial crisis, and they just paid off, to fundholders benefit. So rather than push out a special distribution, management has bumped up the dividend, to dribble it out over time. Perhaps their view is that a higher earned yield will tighten the discount, while a special dividend might just get gobbled up by investors and ignored on a go forward basis. There is a chance that activists could do something here (most of the top holders are all "smart" CEF money) and/or combine this with the other smaller high yield Brookfield offerings run in similar fashions. Their expenses on professional fees, etc. could easily be tightened up without hurting the management company.

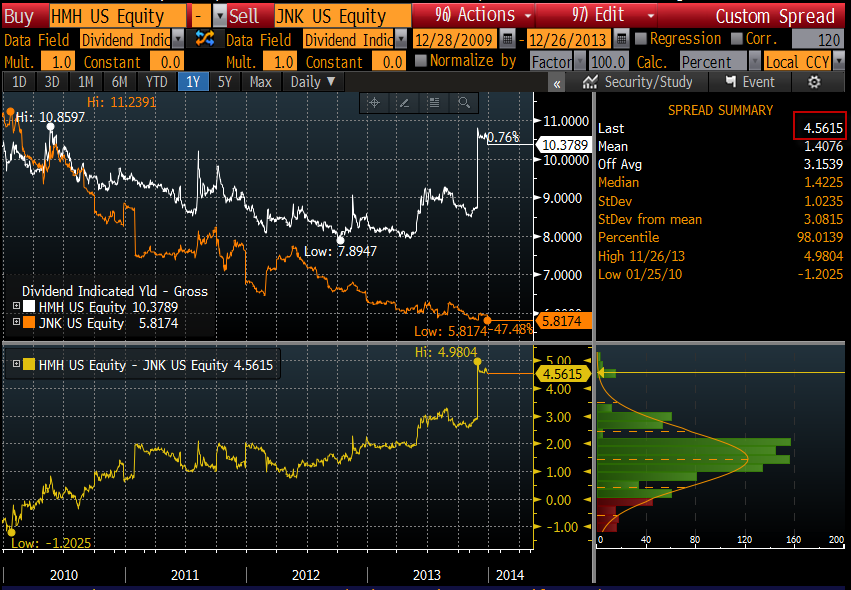

Other smaller Brookfield/Helios funds have been merged in recent years, so this is not outside the realm of possibility. The other Brookfield small sized HY CEFs trade at around 9.5% yields, which is where I think this ought to be, with its new annualized dividend. In comparison to JNK, HMH is trading at wide spreads, relative to its own history. HMH is difficult to trade, so limit orders will be needed, and position sizing is difficult. Here's a historical comparison of HMH vs JNK yield spread, which appears to be wide relative to the past. (click to enlarge)

- Benefits include a high yield, a hefty discount to NAV, a spread to comparable junk bonds, and a slight chance of some fund consolidation (which would tend to reduce the expense ratio)

- Considerations include the sponsor, and the temporary boost from the lawsuit judgments supporting the dividend wearing off in mid 2015. Trading in HMH is illiquid, so use care for entry/exit

- There is a fund card available

Disclosure: I am long AIF, HMH, BOI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire