Fifth Street Finance (FSC) is a business development company or "BDC" that invests in a wide range of industries through both debt and equity. These investments often provide the company with high yields as well as capital appreciation which it then uses to pay shareholders a very generous monthly dividend.

Since companies in this sector typically pay out a high percentage of earnings, there can be an above-average risk of a dividend cut if earnings do not come in as high as expected. This is a downside risk to consider when investing in BDC's. These companies also announce secondary stock offerings with a (relatively) fair amount of frequency, which is another potential downside risk. However, these risks appear limited for Fifth Street Finance now because it already did a secondary offering earlier this year and because it tends to do these offerings only when the stock is trading above book value. This stock currently trades well below book value which is around $9.75 per share, indicating it is undervalued.

Furthermore, this company recently announced a $100 million share buyback and the CEO just bought shares so it seems like a secondary is off the table with the stock trading at such cheap levels. The risk of a dividend cut is also not likely at this time because the company already recently reduced it to 8.33 cents per share on a monthly basis. It also does not seem likely because the company recently stated that it expects earnings to meet or exceed the current payout.

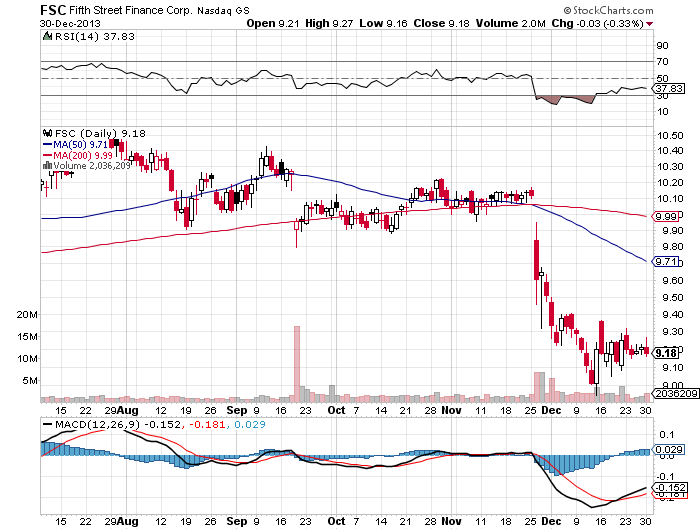

In another article I noted that the yield now appears sustainable and that this viewpoint is shared by JP Morgan (JPM) whose analyst called the dividend "secure". The analyst gave the stock an "overweight" rating and set a $10 price target. Naturally, the dividend cut caused the stock to drop and I believe that since it happened to push the shares towards 52-week lows at the end of the year, that the decline was then further exacerbated by tax-loss selling. As I have been recently highlighting, it can be very rewarding to buy beaten-down stocks at this time of year since many are able to rebound in what is known as the "January Effect Rally". This strategy can pay off big in a short amount of time. To read more about this and hear about another cheap stock that is a top pick for a January Effect Rally, read this article. Let's take a look at the chart below for more details on where this stock has been and where it might be going:

(click to enlarge)

As the chart above shows, this stock was trading for just over $10 in November, but then the dividend cut and ensuing tax-loss selling put a significant amount of pressure on it. If this stock is trading at about $9.24 per share in the midst of tax-loss selling season, (which is not far from the 52-week low of $8.94), it makes you wonder where it might trade once that strong selling pressure is over. I believe the answer is that it could rebound to about $9.75 in January for two reasons: First of all, the 50-day moving average is nearly $9.75 (the 200-day average is slightly higher) and secondly, the book value is $9.75 per share. The 50 and 200-day moving averages are typically key support levels and in a rebound, those levels might act like "magnets" taking the share price upward, especially since the book value also supports this level. The decline caused by the dividend cut and tax-loss selling seems excessive, especially when you consider that the shares yield about 11%.

The cheap valuation on this stock seems to be what caused the company to recently announce a $100 million share buy back and it also appears to have sparked some bargain-hunting on the part of the CEO. On December 13, Leonard Tannenbaum bought 20,000 shares in a transaction valued at roughly $180,000. This is a significant buy in itself, but what's also impressive is that it follows up on a number of other insider buys made throughout 2013.

In summary, the combination of a cheap (below book) valuation, tax-loss selling pressure (which will soon reverse and potentially lead to a January Effect Rally), a still generous yield of nearly 11%, and repeated insider buying, all seem to indicate that this stock is worth buying now. Furthermore, the company will be paying its next monthly dividend of 8.33 cents per share to shareholders of record as of January 15th, so investors won't have long to wait to get paid.

Here are some key points for Fifth Street Finance

Current share price: $9.24

The 52 week range is $8.94 to $11.13

Earnings estimates for 2014 (fiscal year): $1.03 per share

Earnings estimates for 2015 (fiscal year): $1.07 per share

Monthly dividend: 8.33 cents per share, which yields about 11%

Data is sourced from Yahoo Finance. No guarantees or representations

are made. Hawkinvest is not a registered investment advisor and does

not provide specific investment advice. The information is for

informational purposes only. You should always consult a financial

advisor.

Disclosure: I am long FSC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire