2014 is almost here and if you are looking to adjust or find some stocks to make an impact to your portfolio, then why not consider some small caps? 2013 was a great year for both small and large caps, but as the market continues to go up and gives the impression of improvement, expect more people to start plowing their money into the stock market. That's where choosing wisely and looking where others are ignoring will be an advantage. After all, the winning investors are those who flip over the most rocks in search of value.

Over the past several months, I've been making my way through America's Best Small Companies and each of the three stocks you see here have the following characteristics.

- strong sales and earnings growth

- publicly traded for at least a year

- generates annual revenue between $5 million and $1 billion

- stock price no lower than $5 a share

Let's get started.

1. Synaptics (SYNA)

You've encountered Synaptics so many times in your everyday life already. They are the ones that make touchpads on laptops and touchscreens on phones, tablets and touch screen computers. Synaptics is a company with technology and products entrenched in our daily lives. It isn't a flashy non-profitable software or social media tech company. The company has some great stats as a value play which I get to below. To add to that, the valuation isn't over the top, which makes things even more interesting.

First a quick brief.

Quick Stats

- Market Cap of $1.7B

- Sales Growth: 11%

- EPS Growth:26%

- TTM ROE of 24%

- Cash Adjusted PE: 13.6

- EV/EBITDA: 9.5

Quick Discussion

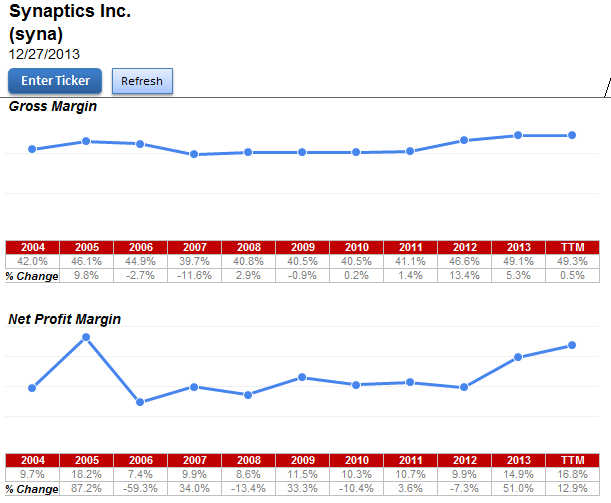

The main highlight that jumps out at me is that Synaptics is a profitable tech company, growing revenues, increasing margins and virtually no debt. Yet, it is priced priced attractively. Revenues have increased by 14.4% in the TTM and at the same time, Cost of Goods Sold has decreased leading to an increase in gross margins to an all time high of 49.3%. This has trickled down to net margins, where it is sitting at 16.8% in the TTM.

(click to enlarge)

Mobile phone adoption continues to increase and phone manufacturers will churn out more phones in 2014.

Synaptics is set to benefit and this industry growth is what has forced the company to spend more on R&D which is now also at peak levels in the 20% range.

Fundamentals and Valuation

Synaptics has some awesome numbers. The balance sheet is healthy with only $2.3m of long-term debt which is nothing compared to the cash on hand of $331m and free cash flow generating ability. The cash conversion cycle increased in 2013 to 45 days compared to 40 days in 2012. While a 5 day difference may not seem like much, when you break it down and compare the differences, days in inventory went from 54 days compared to 40 days the prior year. In other words, inventory is sitting in the warehouse for a longer period before it is sold. Although business is good at the moment, inventory is always something to watch for.

When it comes to valuation, the multiples are enticing. Since SYNA is currently in its Q2 of fiscal 2014, a better proxy is to look at the 2013 multiples.

(click to enlarge)

SYNA Valuation Multiples

If you take the stock price out of the picture, by looking at the above numbers, you would think that it is priced similar to 2011 when it was in the $25-$30 range. But the stock price is at $50 and sounds a lot more expensive when you begin to anchor on price. However, the numbers show that the fundamentals have been driving the stock price instead of speculation and hope like a lot of stocks.

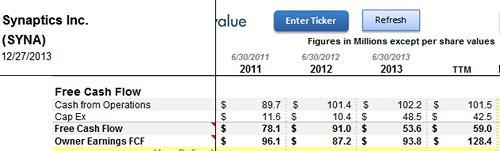

Also, take a look at free cash flow. Capital expenditure increased 3x and accounts receivables increased by 42% compared to 2012. But when you take a look at Buffett's owner earnings which ignores the effects of working capital, it is on a tear.

(click to enlarge)

SYNA FCF vs Owner Earnings

With these two sets of numbers, I can quickly come up with a price estimate based on two different cases by checking what the market expectation is via the reverse DCF method. Then after adjusting the FCF/owner earnings based on a bearish, normal and optimistic case, I get the following numbers from my stock analyzer.

- Base case estimate: $45

- Normal case estimate: $62

- Optimistic estimate: $75

With a margin of safety, I'll be more than happy to pick up shares of Synaptics if it drops below $40.

2. Syntel (SYNT)

Syntel is an outsourcing company and the company gets 75% of its revenues by building applications for other companies. Application outsourcing includes everything in the product cycle. Development, maintenance, testing, building the infrastructure and hosting too.

Its other businesses include

- Knowledge Process Outsourcing (KPO) which is a lot like Business Process Outsourcing, where back office tasks and administration is outsourced.

- e-business is focused on advanced technologies and data analytics to solve business problems

- and teamsourcing is more of a consulting gig for companies looking for advice and help

Not all companies have the luxury of being able to afford and maintain such specialized teams and so it's better off to outsource these tasks. Previously, I highlighted ExlServices (EXLS). Like most companies in this space, Syntel uses the strong Indian IT industry to deliver quality products at a cheap price.

Quick Stats

- Market Cap of $3.8B

- Sales Growth: 17%

- EPS Growth: 20%

- TTM ROE of 32%

- Cash Adjusted PE: 16

- EV/EBITDA: 13

Quick Discussion

When I think of outsourcing companies, the first thing I think of is the switching cost. It's a thorn to switch to another company. That's why the outsourcing industry is very fragmented but all players survive and do well. Once a company gets big, it starts facing issues of being slow, inefficient, and wanting to cut costs. That's where an outsourcing company will win a few contracts here and there. It then leverages that experience to other businesses, building credibility and a steady customer base from there.

The biggest company in the industry that I can think of is Cognizant Technology Solutions (CTSH), which has a market cap of $30b-- 10 times the size of Syntel. I bring this up because size doesn't matter in this space and from the numbers below, you can see why as Syntel is very profitable.

Fundamentals and Valuation

The balance sheet is healthy with a current ratio of 6.71. The company took on $140m of debt in the latest quarter, but seeing how the interest rate they are paying is only 1.51%, getting money that cheap is a good move. Paying 1.51% in interest is close to free. How they spend it is another matter, but there is more than enough FCF to pay the loan payments and as long as the return is greater than 1.51%, it is a smart decision.

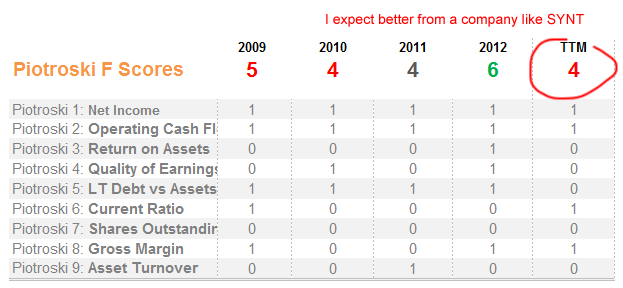

The only point I want to nitpick is the low Piotroski score.

(click to enlarge)

SYNT Disappointing Piotroski Scores

A score of 4 is low compared to the type of return this business is generating.

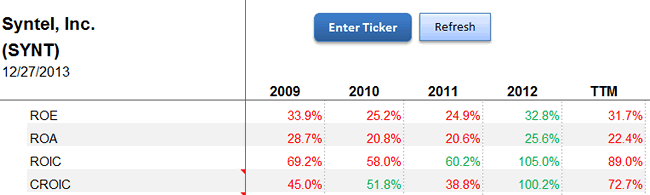

(click to enlarge)

SYNT ROE ROA ROIC and CROIC

Using the reverse DCF again, the market expects SYNT to grow at around 11-13%. Profitability and competitive advantages don't matter in this space. The way you read the chart below is to see how strong the earnings power of a company is. If the EPV (Earnings Power Value) is greater than the cost to replace the value of the business, then a competitive advantage exists.

SYNT Competitive Advantage Exists

A cash adjusted PE of 16 doesn't sound too high, but historically over the past 10 years, it has averaged 14 with the peak being 18 in 2007. Although outsourcing companies are very profitable, the current price requires some sitting and watching.

Here are some valuation estimates.

- Base case estimate: $50

- Normal case estimate: $65

- Optimistic estimate: $100

3. IPG Photonics (IPGP)

I wrote about IPG Photonics early last year and it was another case of me being too cheap to pay for quality. The founder is still running the company, owns a huge chunk of the company via shares and also through his trust. The founder actually escaped from the Soviet Union where he worked on lasers his whole life.

Gapontsev's family was evacuated to the Ural mountains in the darkest days of World War Two, relocating to the Ukraine after his father was freed from a Nazi-run POW camp and then raised in the Soviet Union. Educated as a researcher in lasers, Gapontsev launched his own laser business with the fall of the Soviet empire, only to move it to Germany and then rural Oxford, Massachusetts in the late 1990s when doing business in Russia became untenable. - Forbes

The company product is also best in class as they pioneered fiber laser technology.

Quick Stats

- Market Cap of 3.94B

- Sales Growth: 26%

- EPS Growth: 45%

- TTM ROE of 19.2%

- Cash Adjusted PE: 23

- EV/EBITDA: 14.5

Fundamental Analysis and Valuation

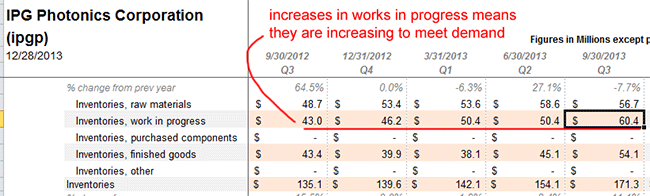

Although growth has slowed in the past couple of years, fiber laser technology is still young so there is room for growth as customers seek to find cheaper and efficient equipment compared to the standard gas or YAG lasers. For companies that manufacture products, one way I like to determine whether there is future demand is to analyze the inventory. To get a full explanation you can see my earlier article on inventory analysis.

For a short explanation, first look at the below image.

(click to enlarge)

IPGP Inventory Analysis

You first need to break down inventory.

The OSV analyzer gets this data automatically to make things easier. For the rest of you, you'll have to dig through the SEC filings to get the breakdown. All inventory isn't the same. The main line to look at is "works in progress". Every quarter, works in progress is increasing. This is a very healthy sign. No company will make more products unless orders are coming in or to meet demand.

Although the total value of inventory has also increased, which makes it look like inventory is getting bloated, by comparing with the works in progress, you get a sense of the demand it is seeing. On another note, shares are regularly diluted which is eating away the intrinsic value every year.

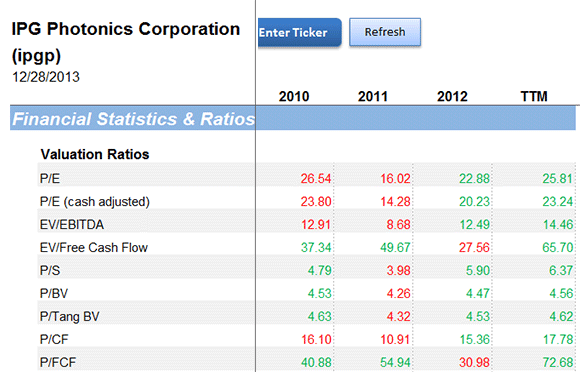

Compared to historic levels, its current multiples are slight above average. Here's just the last 3 year view though.

(click to enlarge)

IPGP Valuation Ratios

A simple rule of thumb is to buy below an EV/EBITDA of 15. It's hitting 14.5 so it's up there.

Here's my intrinsic value estimate.

- Base case estimate: $50

- Normal case estimate: $70

- Optimistic estimate: $95

Include a margin of safety and IPGP will have to come down to around $40-50 before I start thinking about loading the truck.

Disclosure: No positions.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire