by Ramsey Su

Back in June of 2012, I wrote about "The New and Improved Real Estate Investment Model":

The new and improved model is simple. Just like a subprime pool of loans, buy up as many properties as possible, put some lipstick on the pig (aka glossy brochures) and let Wall Street sell it as REITs. They can also securitize the income and voilà, a new round of derivatives is born. Once the fees are made and the syndicators collect their share of the profits, Wall Street can now prosper off the derivatives with no regard to the underlying properties.

Bloomberg recently provided an excellent piece of visual data entitled Blackstone's Big Bet on Rental Homes. It provided a simple, yet concise explanation on how the grand scheme is working so far.

The accumulation phase is over, at least for now. Blackstone's (BX) 41,000 homes portfolio is large enough to move on to the next stage, creating insanely profitable (for Blackstone) derivative products and dumping them on the suckers via Wall Street investment banks. The first offering is just testing the market, with a pool of just 3,207 homes.

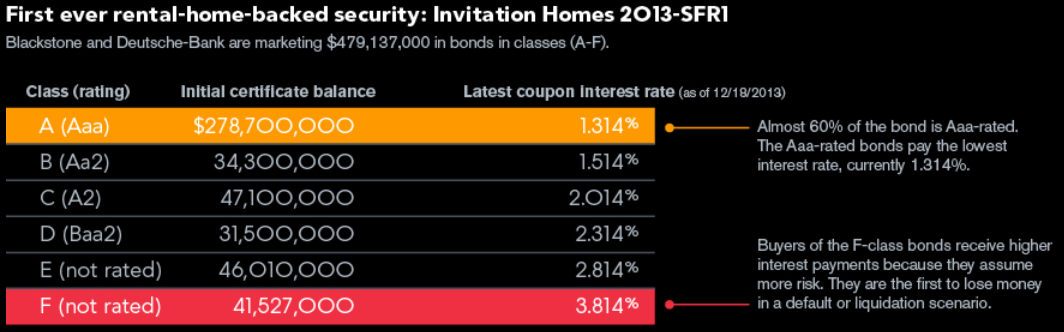

Here is the basic deal as reported by Bloomberg:

Type - Rental-home-backed security

Name - Invitation Homes 2013-SFR1

Amount of offering - $479,137,000 in 6 classes

Security - Rental income from 3,207 single family rentals.

Average Value of Rentals - $199,200

Average Size - 3/4 br, 2+ bth, 1,700 square feet.

Gross Rent - $50,888,889 or $1,322 average per unit per month.

Rent net of 10% vacancy - $45.8 million.

Expense factor - $21.2 million or 46.3%.

Here is Blackstone's generous offer:

(click to enlarge)

Blackstone gets out so that you, dear hoi-polloi, can get in - table by Bloomberg

Here is the way I see it:

1. 1.824%. 58% of the offer pays only 1.314%. There is only an 8.7% unrated tranche, or $41.5 million, that pays 3.8%. The entire offer will cost Blackstone the equivalent of 1.824%.

2. How risky are these bonds? Only $227 is needed from each property each month to service this debt. This is around 17% of scheduled rent. In addition, collateral homes can be sold to cover payments. The securitized amount is 75% of value (LTV). For these bonds to default, the real estate market would have to collapse. It would be the end of the world as we know it.

3. Rating agencies are still prostitutes. Just like with subprime mortgage-backed securities, the rating agencies are once again prostituting themselves for a fee. The Blackstone offering is sliced into 6 tranches, 2 of which are unrated. Just imagine if Blackstone were to use a conventional method to finance these houses, it would be one loan and one rate. The slicing and dicing allows Blackstone to essentially borrow $391 million of the $479 million at just under 1.5%. I will discuss this some more in the conclusions further below.

4. True LTV. These properties are valued at $638.8 million, per brokers' price opinions. However, we know Blackstone paid less, probably substantially less. If we use cost basis as value, the true LTV is most likely greater than 100%.

5.…. and that is not all. This pool of rentals supposedly generates a net cash flow of $24.6 million, or a 5.1% return. The income takes into account a 10% vacancy and 41.7% expense factor. These are quite reasonable assumptions. So Blackstone is receiving a 5.1% return and paying out 1.824% in bond payments. What a healthy spread!! Wait, that is not all. Blackstone also gets to pocket all appreciation on the underlying assets.

6. A bubble is born. The subprime bubble was inflated by the acceptance of subprime mortgage back securities from 2002 till their demise. If these rent-backed securities prove to be successful, then Blackstone and others with Wall Street connections will revamp their acquisition strategies. In other words, if Blackstone's cost of funds is 1.824% for financing, they can go buy properties yielding as low as a 3% cap rate and still make a 1.18% spread for free, on top of the management and junk fees they have and will continue to collect. As soon as there are enough of these bonds, then they can move on to the even more exotic and lucrative derivative products. May be we will see an RDS - a rent default swap?

In conclusion, this is an excellent example of how ill-conceived Fed policies result in the transfer of wealth from everyone else to the 1%ers. Bernanke and the FOMC do not understand that keeping rates low does not apply across the board. As illustrated above, Blackstone can borrow at less than half the cost that mom and pop have to pay, who are competing with Blackstone for the same houses. Blackstone pays 1.824% interest, mom and pop are lucky with 4.5%, plus mortgage insurance. Was that Bernanke's intent? What about smaller investors? Financing is even harder to come by for them. So they can only pursue purchases with non-leveraged cash.

With indefinite ZIRP policies, households have few investment options and are forced into giving their savings to Blackstone for these paltry returns, while Blackstone parlays these low cost funds into fortunes. Households that cannot compete with Blackstone end up being the tenants, forever contributing to the 1%er's well being.

A healthy housing market is one with a balance of qualified buyers and sellers, supported by sound financing programs that are readily available to the creditworthy. The markets and policy makers mistakenly assume price appreciation equals recovery. How can 20% appreciation be considered good? It is a speculative bubble largely created by the Fed. If the Yellen Fed continues down the same path as its predecessors, the Blackstones are likely going to be able to reload their war chests and resume their buying sprees once more. The wealth and income gap will continue to widen. Not a good thing.

Disclosure: No positions

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire