On July 6th 2013, the Economist published the article: "An Inferno of Unprofitability: The world's overcapacity in steelmaking is getting worse, and profits are evaporating," which described the abysmal state of the steel industry at the time. It attributed the industry's struggles to overcapacity, razor-thin profit margins, and reliance on iron ore, a volatile commodity essential in steel production. The article also predicted that European and American steel manufacturers would struggle more than their Asian and Latin American counterparts because of the lackluster demand in home markets. However, ironically after this article was published, most of the world's major steel producers' stocks shot up, with American and European firms boasting the largest gains. Given the article's sound thesis, this turn of events was unexpected and doesn't appear to be attributable to the slightly improved economic outlook in the developed world. Although I believe the steel industry will eventually succeed, the current rally is premature. Demand is not projected to increase much in the next year and there is still too much overcapacity in the industry to achieve strong profit margins. Based on this thesis, and I Know First's algorithmic stock predictions, I would recommend shorting the steel industry in the medium-term horizon (3-months) in anticipation of a market correction, and then going long the steelmakers in the long-term horizon (1-year) in anticipation of an industry turnaround.

Comparison to Aluminum Market

The issue of overcapacity has long plagued the aluminum industry as well, as I explained in my article, Alcoa And The Future Of The Aluminum Production Industry from last August. Aluminum producers similarly had to operate unprofitable plants and were often losing money for years on end. Additionally, Chinese aluminum producers were also outproducing their Western counterparts and claiming most of the vast Chinese market. However, now that the major aluminum producers are cutting back production, the industry has already started to rebound.

There are many differences between the two industries; most important, the aluminum production industry is dominated by a few big firms while no steel producer controls more than 6% of the market and the steel industry is much more dependent on volatile commodity prices. However, the negative profits due to overcapacity makes the aluminum industry the perfect foil for the steel industry and demonstrates the potential for a true steel turnaround. Only after the major aluminum producers approached profitability did their stocks take off; the fact that most of the steel producers are still far from profitability shows that their current rally is premature.

Steel Production and the Industry's Competition

Iron ore is the principal component of steel and its extraction is dominated by four huge mining companies. Since 2010, steelmakers no longer pay fixed prices for iron ore, but rather pay the volatile market value for the ore. The Economist article describes the mining business as a seller's market because its consolidation allows it to set prices and not have to negotiate with buyers. The steel manufacturing business, on the other hand, is a buyer's market because the various buyers can negotiate favorable deals with the 60 steel suppliers who produce upwards of 5 million tons. Ultimately, steel producers pay top dollar for iron ore and often are forced to sell their steel at a loss.

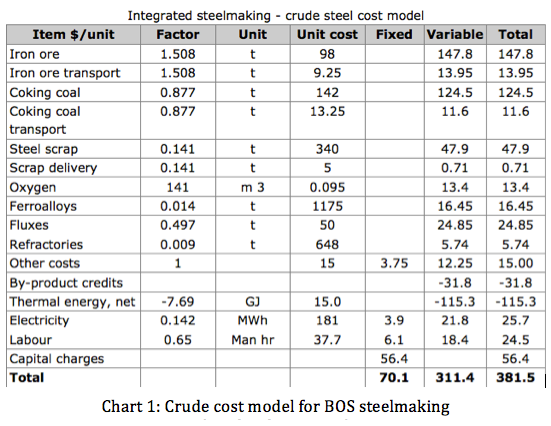

Basic Oxygen Steelmaking (BOS) is currently the primary process of producing steel. The crude steel cost model in Chart 1 shows a breakdown of BOS costs, estimating that it costs only $381.5 to produce a metric ton of steel.

(click to enlarge)

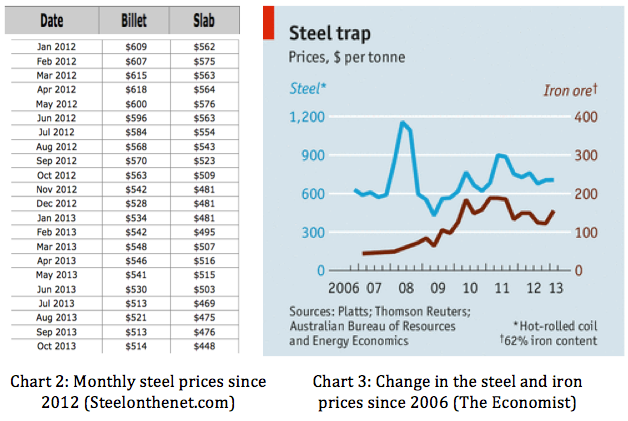

However as competition and overproduction have become more prevalent in the steelmaking industry, the price of steel has been decreasing relatively steadily as demonstrated by Charts 2 and 3. Even though there still appears to be a relatively large margin between production costs and selling prices, this can be illusory because of the negotiating power of the steel buyers.

(click to enlarge)

Additionally, China has been continuing to expand its steel production capacities despite the fact that there is already tremendous overcapacity. Therefore, even as Western steelmakers shut down unprofitable plants and scale back their operations there will still be a glut of steel on the market. As China's economy has begun to slow down, it has been exporting its excess steel, further decreasing the global price of steel. On top of decreased steel prices, Chinese producers have driven up the cost of iron ore in recent years, decreasing manufacturing margins even further, as demonstrated by Chart 3. If the major steelmakers don't find a way to decrease overcapacity then the industry will be doomed to continue to brave many more years of negative profits.

China and The Effects of Economic Growth on Steel Production

Rising steel demand has always been a good indicator of rapid economic growth; however, once countries finish updating their infrastructure their demands tend to decrease rapidly. This phenomenon can be seen in Charts 4 and 5, which show how US steel consumption and production reached a peak in 1975 and have been falling relatively steadily ever since. As China has almost finished urbanizing and as it has already built much infrastructure that is not even being used, its steel consumption is bound to take a nosedive.

(click to enlarge)

(click to enlarge)

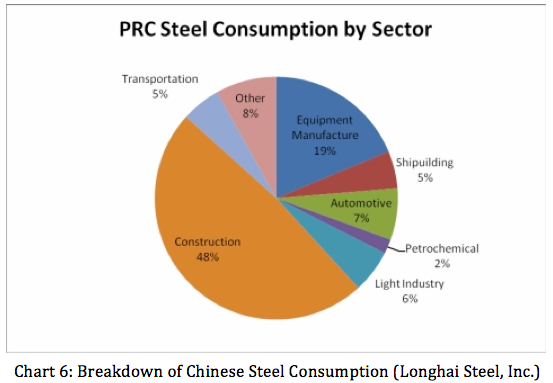

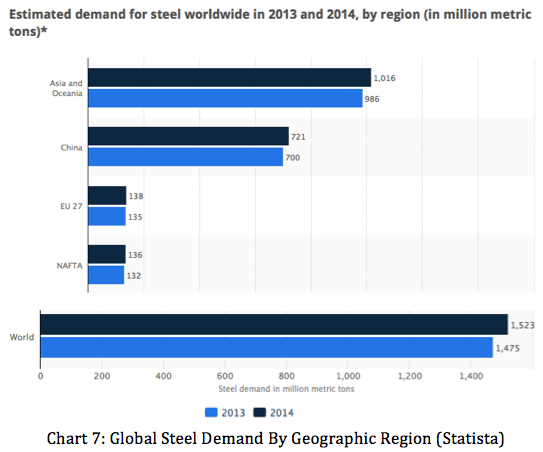

The Chinese government is trying to combat a real estate bubble by placing curbs on building and owning real estate; however, these efforts seem to be in vain as construction continues to increase. Chart 6 shows how nearly half of Chinese steel is used by the construction industry; so when China inevitably experiences its real estate bubble and construction comes to a halt, China's steel demand will plummet. As China comprises about half of the world's steel demand (Chart 7), the global steel industry's overcapacity problem will exacerbate.

(click to enlarge)

(click to enlarge)

Analysts from the Japanese financial conglomerate, Nomura, argue that Chinese steel consumption won't increase in the near future even assuming a faster and more steel-intensive urbanization than before. They also argue that had the central government not heavily subsidized construction in recent years, steel consumption would have already begun to fall. Once China's government stops subsidizing construction and its rapid urbanization starts to subside, its construction will inevitably decrease and it will drastically cutback its steel consumption.

The Effects of an Improving Economy on Steel Production

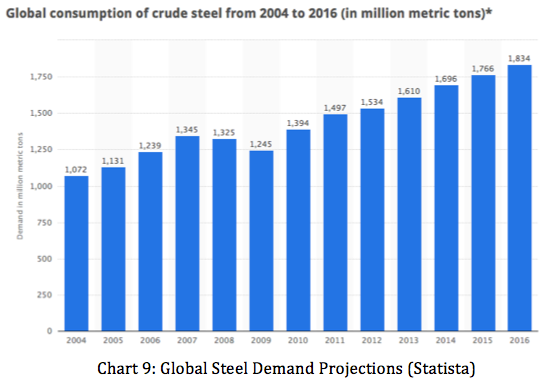

The resurgent developed world's economic recovery will partially offset the decrease in global steel demand resulting from China's economic slow down and construction saturation. ArcelorMittal and Tata Steel, Europe's biggest and second biggest steel producers, expect demand for steel to increase tepidly in 2014. The Chief Executive of Tata Steel's European division said: "The worst...is behind us. [We] see clearly signs of improvement in Europe of a modest level." Additionally, both American and global steel demand is predicted to increase in upcoming years (Charts 8 and 9).

(click to enlarge)

(click to enlarge)

Some analysts from such firms as Goldman Sachs, Morgan Stanley, and Cowen have been quick to upgrade steel companies after their incredible 6-month rallies because "strengthening demand and an accelerating global economic recovery should enable producers with excess capacity to capture latent earnings" (Cowen's Anthony Rizzuto). However, improving American and European economies will not boost steel demand enough to counter a decrease in Chinese demand or the current glut of supply. Before the major steel producers can take advantage of a growing global economy, they have to return to profitability by combating their oversupply problems. I believe that the steelmakers' current stock price increases are premature and will soon face major corrections.

Necessary Steps for a True Turnaround in the Steel Industry

In the 1990's American steel producers struggled to remain profitable for numerous reasons including not adopting lower cost production methods and increased vulnerability to economic downturns. By 2003, even though the economy was picking up and steel demand was slowly increasing, most steel companies remained unprofitable. Steel prices only began to increase once antiquated, unprofitable plants were closed and unprofitable firms went bankrupt or were acquired.

Since no steel producer currently controls more than 6% of the market, it is difficult to manage the oversupply problem. This problem will only subside when the steel industry consolidates and closes down its unprofitable factories as it did in the early 2000's and as the aluminum industry is now in the midst of doing. The current steel rally would seem to be shortsighted because few of these structural changes have occurred so far.

Analysis of the Weak Financials of U.S. Steel and ArcelorMittal

Both U.S. Steel (X) and ArcelorMittal (MT) are currently earning negative profits and are unlikely to see profits in the future. Ironically U.S. Steel's stock only took off once its profit margin greatly deteriorated, falling to -$1.8 billion from -$78 million three months earlier. Its EPS decreased from -0.59 a year ago to -0.97 and is expected to decrease further to -1.28 this coming year. Its debt-to-equity ratio of 2.22 is higher than the industry average of 0.87, its debt ratio has been increasing, and its return on equity is incredibly low compared to the steel industry and S&P averages. Additionally, its growth rate is much lower than the industry average perhaps attributable to its relatively low spending on investment activities. The Motley Fool says that U.S. Steel's stock is 25 times more expensive than analysts' generous expectations for next year's earnings. It further argues that its enterprise value to free cash flow ratio of 86 is inconceivable, especially due its weak growth rate.

Although analysts expect ArcelorMittal to grow faster than U.S. Steel, it has taken on much more debt. ArcelorMittal's debt-to-equity ratio has risen from 1.22 in 2012 to 1.33 this past quarter, which is also higher than the industry average of 0.87. Its enterprise value to free cash flow ratio of 51.5, is not as bad as that of U.S. Steel but still pretty abysmal. ArcelorMittal's return on equity is also lower than the industry and S&P averages.

Both of these Western steel producers have worse financials than the industry average. Coupled with the inherent problems in the steel industry of overproduction and lack of market power, U.S. Steel and ArcelorMittal should brace for a large market correction. These Western firms' rallies were much more vigorous than those of their Asian competitors such as the Japanese Nippon Steel & Sumitomo Metal Corp and the Korean POSCO, despite the fact that the Asian steelmakers are profitable and have much more robust balance sheets.

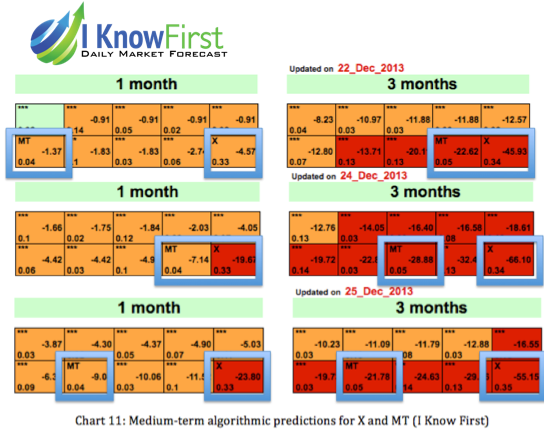

I Know First's Predictions for U.S. Steel and ArcelorMittal

I Know First uses a unique algorithm to predict the stock market. The stock algorithm constantly updates itself as it processes new information and averages many independent models to output a continuous stream of signals that project the direction and magnitude that each particular stock will move. (To learn more about the algorithm, see my article on Citigroup). In the past the algorithm has done a good job predicting equity corrections such as it did for gold and the Japanese Yen.

I Know First's algorithm predicts that U.S. Steel and ArcelorMittal will break their current rallies and perform very poorly in the short-term (14-days) and medium-terms (1-3 months) The red colors of these two stocks in Charts 10 and 11 denote a negative outlook. Interestingly, however, the algorithm expects both stocks to rise in the long-term (1-year), as the green colors in Chart 12 denote; perhaps due to real, healthy growth after a correction in their current irrationally high valuations.

(click to enlarge)

AK Steel Holding and Specialty Steel Companies

Some smaller steel producers, such as AK Steel Holding (AKS), focus on manufacturing specialty steel products such as stainless steels, electrical steels, and crash barriers. Because there are fewer specialty steel producers, these firms have greater marker power and are thus are able to charge value added surcharges. AK Steel Holding has been performing extraordinarily well recently and has announced that it expects to return to profitability by the end of the year despite falling sales prices and that it expects shipments to increase by about 13% due to stronger demand in carbon sales. AK Steel is a good example of a lean steel producer that has a defined and focused market.

I Know First's Prediction for AK Steel Holding

Even though I Know First currently has a negative stock outlook for the major steel producers, it is still bullish on AK Steel Holding in both the medium and long-term time horizons. I Know First's algorithm had been rating AK Steel Holding as a strong buy as early as November 6th as evidenced by its dark green background in Charts 12 and 13. Perhaps I Know First's algorithm expects that AK Steel Holding's relatively specialized market will buck the general downward trend of the steelmaking industry.

(click to enlarge)

How Pair Trades May Be Good Investment Strategies

Since it is difficult to time the market, it would be a very risky decision to short U.S. Steel and ArcelorMittal in the midst of their current rallies that have lasted for the past six months. To hedge some of this risk, I would suggest opening a pair trade where an investor would go long a more stable steel producer such as Nippon Steel or POSCO (PKX) while shorting weaker steel producers such as U.S. Steel and ArcelorMittal. This way even if the steel industry does continue to rally, some of the losses from shorting the Western steelmakers will be offset by the gains from the Asian steelmakers. Though, if the steel industry does in fact experience a correction, the gains from shorting the Western steelmakers will be slightly offset from the losses from going long the underperforming Asian steelmakers. It may also be a good idea to pair AK Steel Holding with U.S. Steel and ArcelorMittal as I Know First predicts that AK Steel Holding will continue its rally while the other two stocks will experience corrections.

Conclusion

The Steel industry is currently plagued by excessive competition and overcapacity, causing most steelmakers to be unprofitable or to run plants that are unprofitable. As China's steel demand stabilizes and eventually decreases due to its decelerating economic growth and its slowing rate of urbanization, global steel demand should decrease putting further stress on steel prices. Despite anticipated steel demand from an improving global economy, the fundamental state of the steel industry is too troubled to justify its current rally in the stock market. Instead, we should learn from the turnaround of the American steel industry in the early 2000s and the current turnaround of the aluminum industry, that steelmakers have to shutdown unprofitable plants and firms to decrease their overcapacity problems before they can grow and earn consistent profits.

Though the general steel industry is due for a correction, U.S. Steel and ArcelorMittal are in particularly bad shape. Since the Asian firms and the smaller American firms, AK Steel Holding, seem to be better equipped to handle a slump in the steel industry, it may be a good idea to execute a pair trade by going long the more sound steelmakers and shorting the weaker steelmakers.

Though I Know First's algorithm is predicting a short/medium-term decrease in both U.S. Steel and ArcelorMittal, shorting either is a risky investment because they are both in the midst of a prolonged rally and it is nearly impossible to time the market perfectly. Perhaps it would be prudent to wait until these stocks begin to plateau or even slightly decrease before actually placing short positions. It is also important to consider that though I Know First's algorithm predicts that U.S. Steel and ArcelorMittal will decrease in the 1-month and 3-month time horizons, it also predicts that they will actually increase in the 1-year time horizon. In other words, I Know First believes that the steel industry will experience an authentic, robust recovery after undergoing an imminent correction.

Disclaimer: I Know First Research is the analytic branch of I Know First, a financial startup company that specializes in quantitatively predicting the stock market. This article was written by Ethan Fried (Harvard College '16) one of our analysts. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.

2

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire