Alternate asset managers such as Kohlberg, Kravis and Roberts (KKR), Blackstone (BX) and Carlyle (CG) have been on a tear over the last two years for multiple reasons. First is the desire for large investor (read Pension Funds) to diversify beyond stocks and bonds into alternate investments that include Private Equity and Hedge Funds. The second is that this asset class provides both healthy growth and healthy distributions.

(click to enlarge)

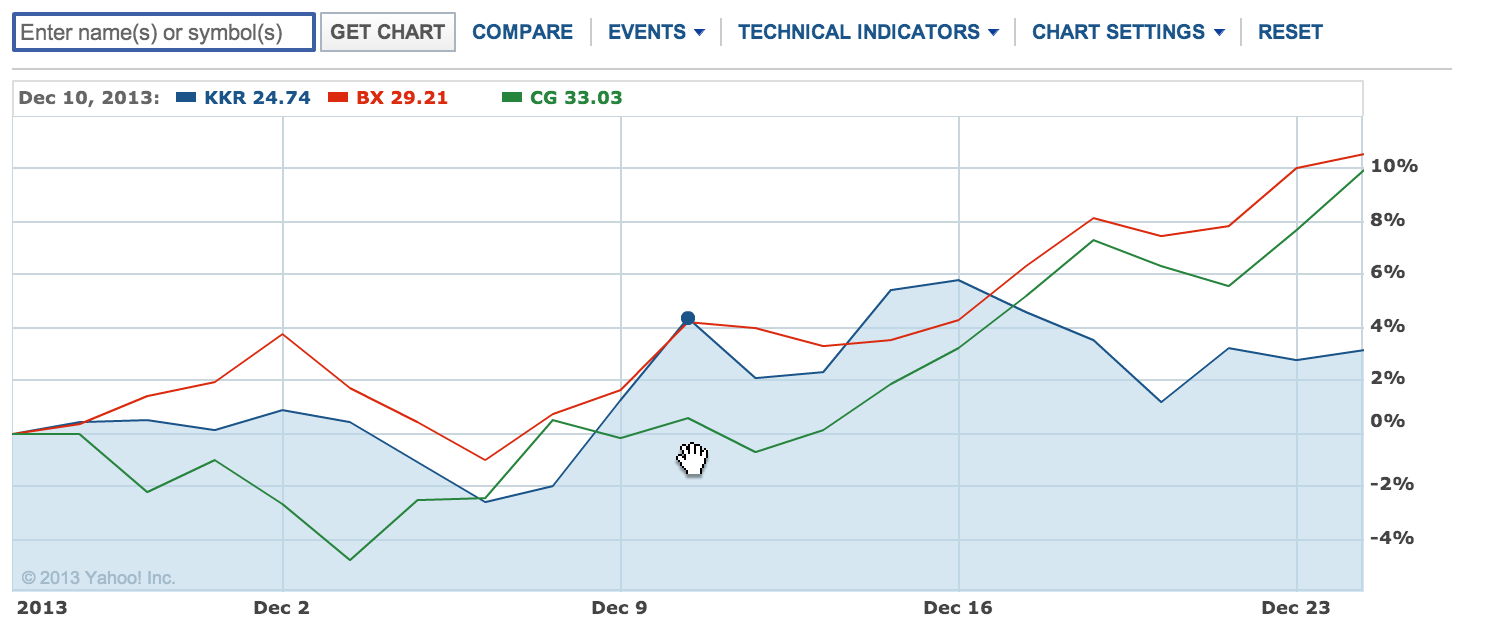

All the stocks in this asset class have been largely in lock-step, but for some reason the recent acquisition announcement from KKR has put a damper on that particular stock (see stock chart above). For those unfamiliar with KKR Financial Holdings (KFN), KFN is a specialty finance company that operates in the leveraged debt space, and aims to generate total returns via a combination of income and capital gains. Think of it as more income focused than KKR, but nevertheless with a 'spicier' risk profile than traditional asset managers. KFN is a separately traded subsidiary of KKR that has been under KKR management since 2004. KKR is intimately familiar with the strategy and investments of KFN, and the two companies have shared deals and know how in the past. With that as background, here are 4 reasons why the proposed KFN acquisition makes KKR more (not less) attractive than its peers.

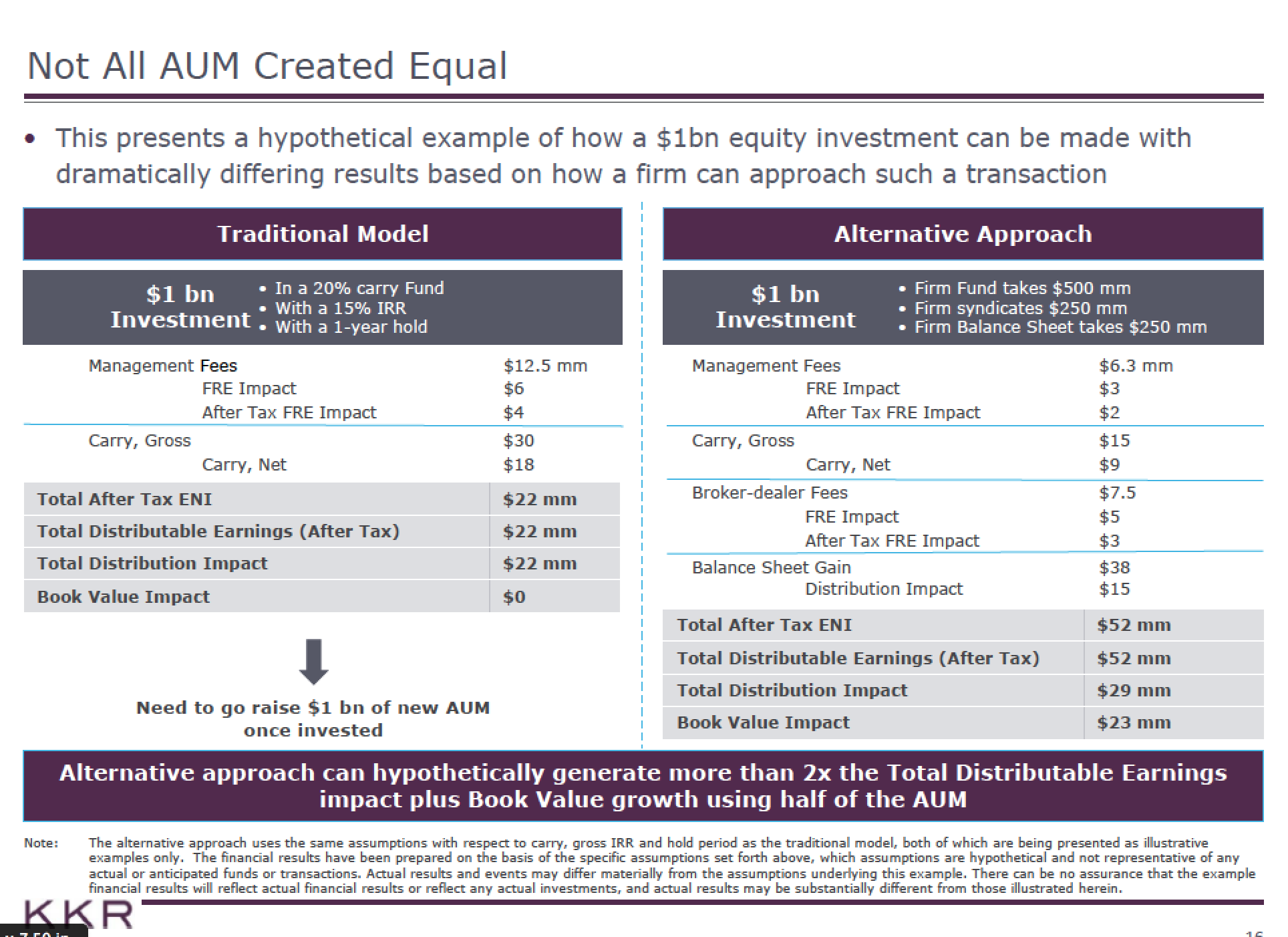

Win-Win. KKR has very strong investment skills but is challenged to generate the kinds of distribution growth looking forward, that it has generated over the last 2 years. KFN has done a good job of generated income (to the tune of about 8%) but has been marked down by investors because it needs growth to keep to its promise of a T+10 investment (i.e. total return of 10% over and above 10-year treasuries). KKR argues from the slide below that it can generate more leverage from the KFN income streams in a combined KKR-KFN company. This statement has credibility given a) KKR's 30-year record of investing through thick and thin, b) KFN's proven ability to maintain an income stream thru the worst years of '09-10 and c) the unique quality of debt income streams that KFN has, that are hard to replicate in a platform that starts from scratch today.

(click to enlarge)

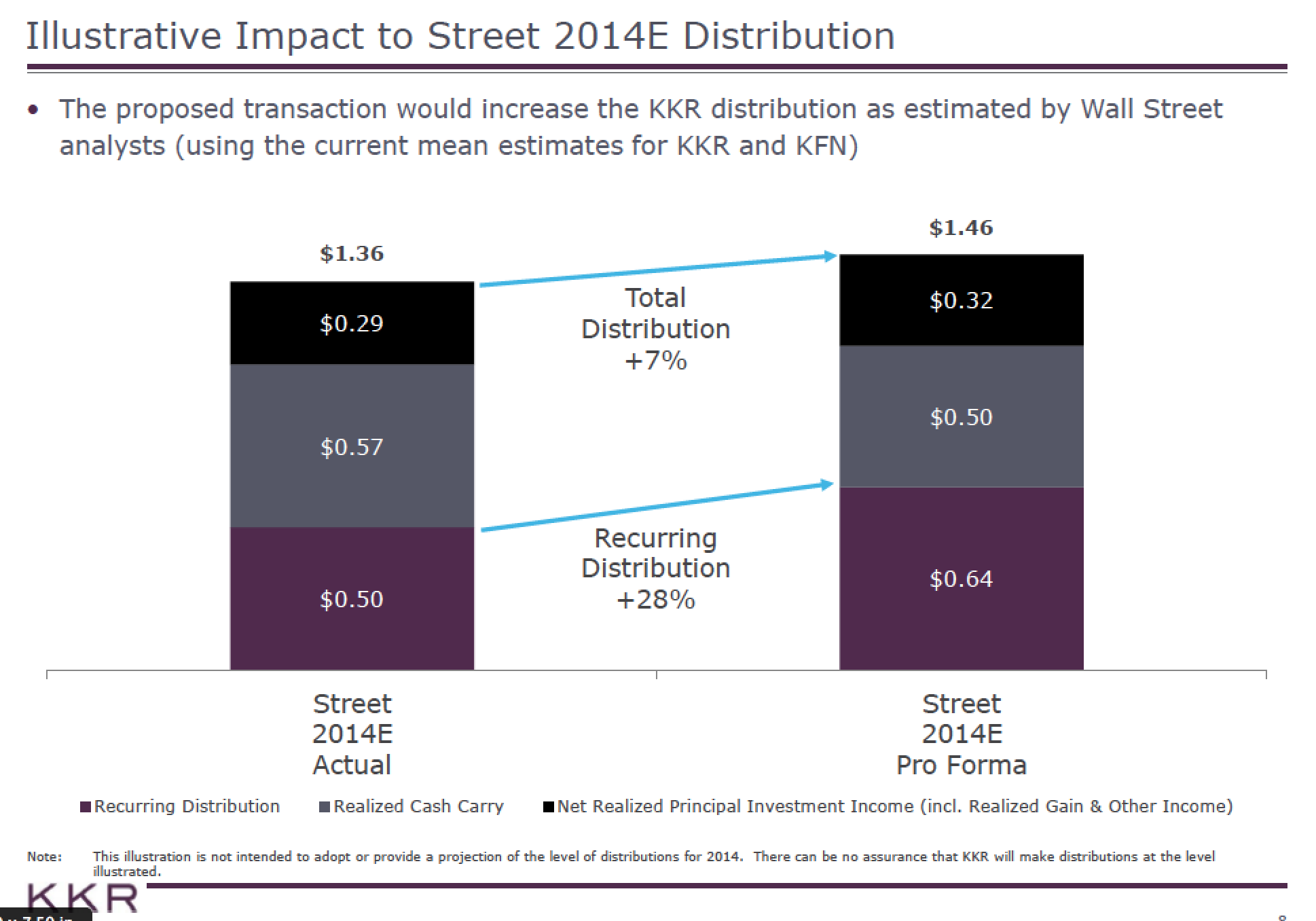

Positive Impact on Income Stream. Sites such as Yahoo Finance, incorrectly state KKR's dividend as 3.80% (or 92 cents/yr) due to the variability of income streams on a per quarter basis. As the figure below indicates, the KFN acquisition revises KKR's distribution upwards about 8% to $1.46, which equates to a roughly 6% dividend at its current stock price. 6% dividend on a growth stock like KKR is an unusual total return combination indeed.

(click to enlarge)

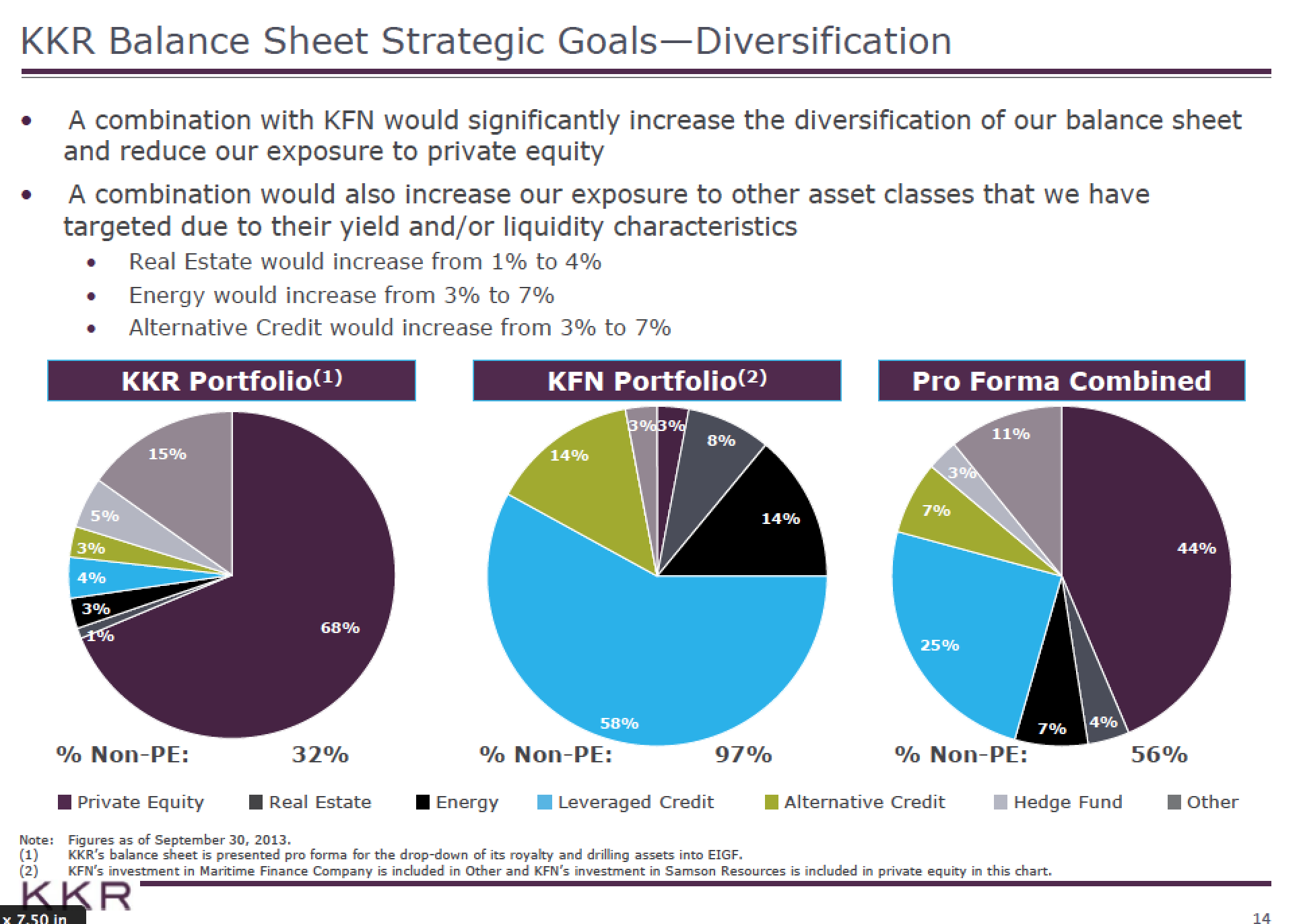

Diversification. I started investing in KKR it's one of the few ways that ordinary schmucks like us can get a piece of the private equity pie. But KKR had become increasingly concentrated in PE, and I wanted exposure to real estate a la Blackstone and other forms of credit that would do well in an inflationary environment. The merger begins to moderate KKR's PE portfolio (from 69 to 44%, see figure below) and increase some of the other bits. Equally, I believe it is the beginning of KKR's go at a real estate platform, that will give it some of BX and CG's positive attributes as it comes to real estate.

(click to enlarge)

Analyst Upgrades. All in all, I won't argue that any of the alternative asset managers are cheap. But I will argue for two things - a) that 'alternates' will continue to deliver for some time to come and b) that KKR's diversity makes it the preferred alternate asset manager for me (although BX and CG are pretty good in that order) and c) the KKR-KFN merger makes KKR more (not less) attractive on both a relative and absolute scale. Most analysts who have upgraded KKR's target price to the $28 to $31 range seem to agree with me. Add that potential 15% capital gains return with 6% distribution and you get a potential 20% return that is nothing to sneeze at.

As always, do your due diligence and trust your instinct.

Disclosure: I am long KKR, BX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire