Introduction

Newcastle Investment Corp. (NCT) is a real estate investment trust (REIT) with a bit of an identity crisis. It's in the midst of transitioning from a commercial REIT (think CDOs and other forms of r

Historical Background

Newcastle Investment is an externally-managed REIT (managed by Fortress Investment Group - FIG) that has been nothing short of a juggernaut for shareholders in recent years. Through financial engineering and prudent investing strategies, NCT has consistently delivered above-market returns for its investors. Here's a two year chart (spin-off adjusted, but not including dividends):

(click to enlarge)

New Residential Spin-Off

Earlier this year, on May 16, Newcastle completed the spinoff of its wholly owned subsidiary, New Residential. New Residential (NRZ) is primarily a mortgage servicing REIT, although it also holds some residential mortgage paper (agency and non-agency). As part of the spin-off, Newcastle shareholders received one share of NRZ for each share of NCT that they owned.

Up to this point, NRZ's share price has largely disappointed, but its dividend has met or beaten exceptions in each quarter this year. I suspect that, as the market continues to get comfortable with the stability of NRZ's dividend stream, its share price will find its footing and may even start to appreciate. Investors have also been incorrectly lumping it in with traditional mREITs, further adding to the frustrating price action. NRZ's dividend for the last two quarters was $0.175, giving the stock a close to 11% yield. It also recently announced a special dividend of $.075, which predictably sent the stock higher. Here's a YTD chart on NRZ:

(click to enlarge)

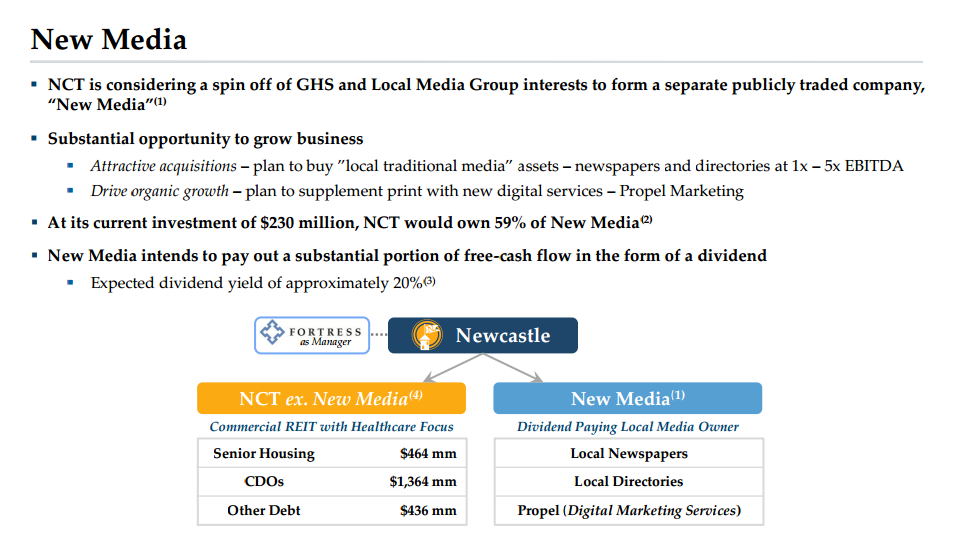

New Media Spin-Off

Following its NRZ spin-off, Newcastle announced in September 2013 that it would also be spinning off its media division, New Media. The spinoff is expected to be completed in Q1 2013, meaning that, if you purchase shares today, you will still receive New Media shares when they begin trading. Newcastle shareholders will again receive one share of New Media for each share of NCT that they hold.

New Media is a collection of media assets, primarily newspapers. The division is composed of two media investments: Dow Jones Local Media Group and GateHouse Media, which each own several local newspapers and digital marketing servicers. Local media assets are actually in vogue with investors, including Warren Buffett, as they tend to be less prone to disruption by social media. In Buffett's 2012 annual letter, he wrote "[p]apers delivering comprehensive and reliable information to tightly-bound communities and having a sensible Internet strategy will remain viable for a long time." This makes sense; after all, you can't go on Twitter and see who is holding a yard sale in your neighborhood.

The icing on the cake is that management seems content on using New Media as a cash cow for NCT shareholders, guiding towards a 20% dividend yield upon inception. I don't care what the business is -- if it yields 20%, I'm interested. The slide below from Newcastle's New Media investor presentation gives you a better look into the business and projected dividend yield.

(click to enlarge)

Coming up with a value for New Media, I arrive at a back of the envelope valuation of $230-690 million, which translates to a share price of $0.65-$1.3. This value is derived using NCT's post-secondary share count of 351 million (remember NCT shareholders will receive one share of New Media for each NCT share they hold) and New Media's projection of $46 million in annual dividends upon inception. This translates to dividends of $0.13/share per year and a share price of $0.65 at a 20% yield. The table below shows the valuation for New Media:

Dividend | Yield | Share Price | Equity Value | |

Bear Case | $0.13 | 20% | $0.65 | 230 million |

Base Case | $0.13 | 13% | $1 | 531 million |

Bull Case | $0.13 | 10% | $1.3 | 690 million |

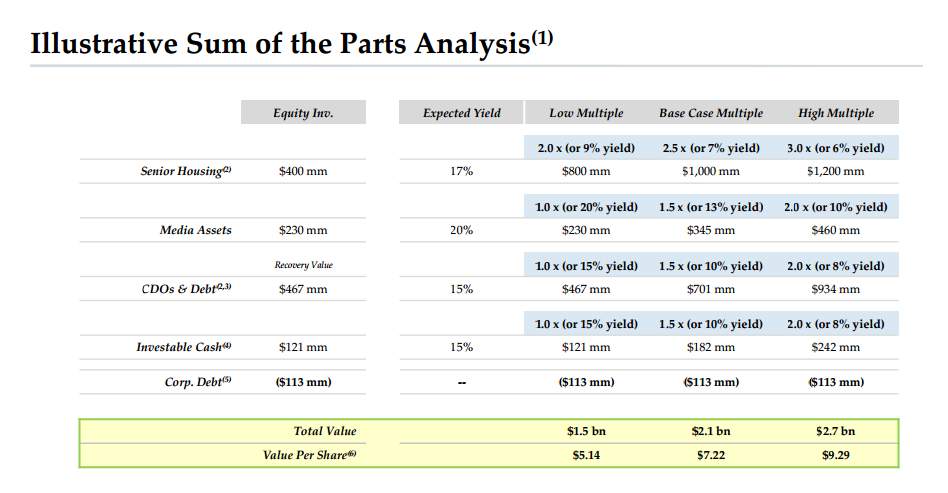

These three scenarios come straight from Newcastle's Media presentation. Specifically, from slide 15 which provides a sum of the parts analysis of the company. The slide is reproduced, in part, below:

(click to enlarge)

For what it's worth, the New Media spin-off is merely a secondary benefit of owning NCT. The real story here is the metamorphosis into a Healthcare REIT. As such, I look at the New Media shares as a free call option on an arguably marginal business that has a chance to do well. If it does, great. But, if not, the thesis remains fully in-tact. Put another way, you can ascribe absolutely no value to the New Media spin-off and still earn a fantastic return by buying NCT. Nevertheless, given the seal of approval by Warren Buffett and the bullish guidance by Newcastle's management, I like the idea of getting a piece of this dividend-paying business.

The Transition

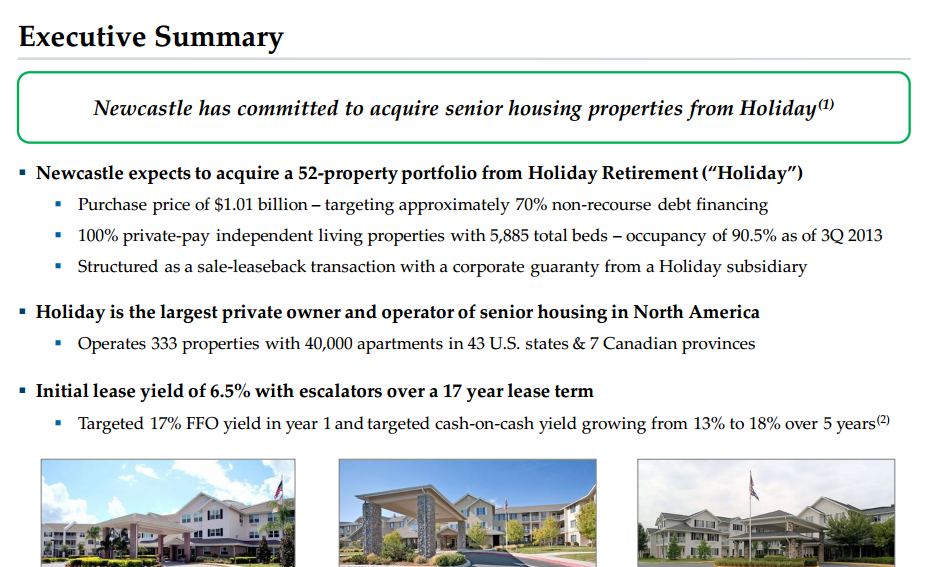

After announcing two spin-offs, NCT has continued its transition into a pure Healthcare REIT, with its acquisition of a 52 property senior living portfolio from Holiday Acquisition Holdings LLC for ~$1.1 billion. (For full disclosure, Holiday is actually owned by Fortress, NCT's external-manager, but does not trade publicly). NCT has held senior living assets for quite some time, but never in this kind of size. This acquisition will put more than half of NCT's investable assets into senior living properties.

On the same day that the Holiday acquisition was announced, NCT also announced a secondary offering of 50 million shares, which priced at $5.25 and gave the company roughly $250 million in gross proceeds which were used to help for pay for the acquisition.

Interestingly, shares barely budged after news of the secondary. The stock stuck around the offering price for a few weeks, but now trades firmly higher. This should be interpreted as confidence in NCT's strategy by its shareholders.

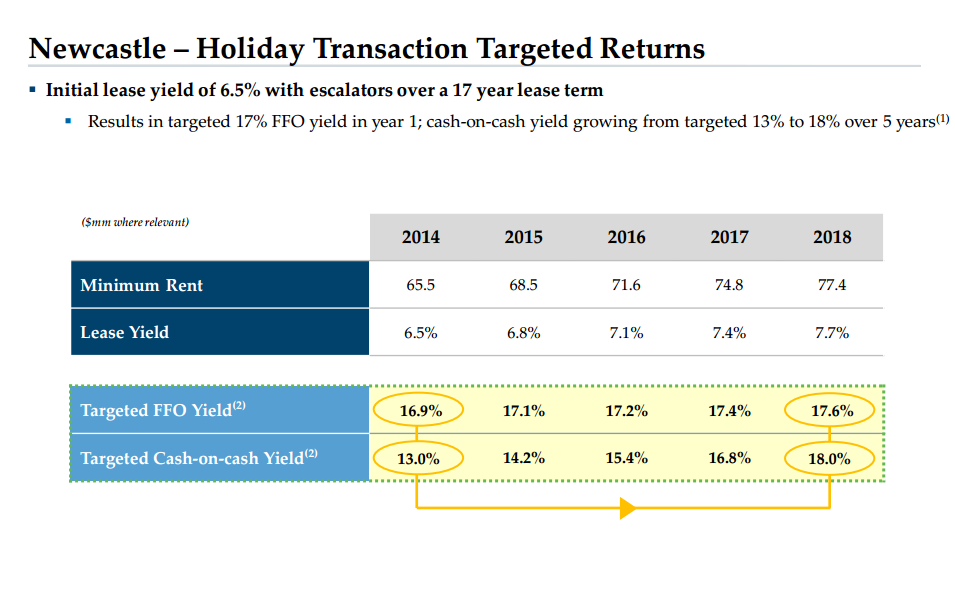

The following week, NCT published an Investor Presentation on its strategy regarding Senior Housing. In short, it looks great and the market is either not yet convinced that NCT can pull it off, or is has yet to fully appreciate the opportunity. On the Holiday assets, NCT is targeting a funds from operations (FFO) 16.9% yield in 2014 on its equity investment, with an increase to 17.6% by 2018.

(click to enlarge)

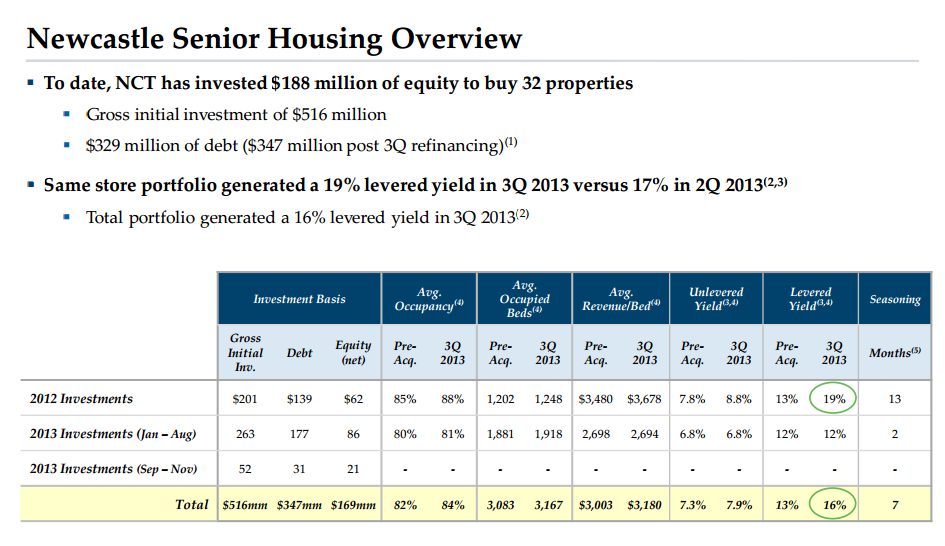

This sort of yield may seem lofty, but NCT has actually already proven that they can achieve these levels of returns (albeit at a lower scale). NCT's existing portfolio of senior housing came with an $188 million initial investment, and generated a 16% levered yield last quarter.

(click to enlarge)

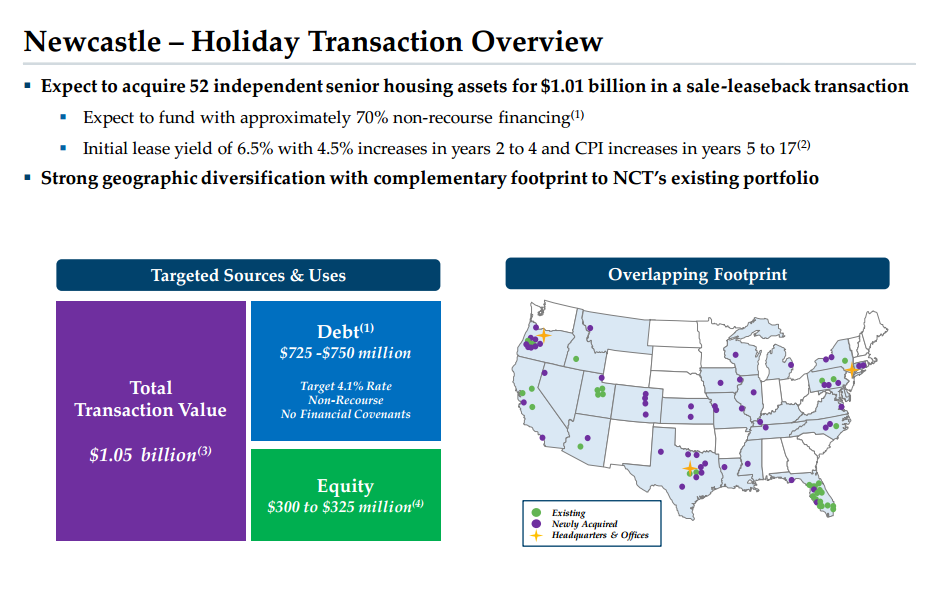

One could also argue that returns would be lower as the business grows, but I personally don't see it. The 52 properties that Newcastle acquired from Holiday are nothing short of high quality. They have a 90.5% occupancy rate on 5,885 total beds, and are "private-pay" operators which means they command higher rates than Medicare/Medicaid. They have generated 15% annual NOI growth over the past three years, and are geographically diversified in a way that complements NCT's existing portfolio very well. What's not to like?

(click to enlarge)

(click to enlarge)

Even better, the investment still works even if management's projections prove to be a bit too optimistic. NCT's fair value is so far depressed from its market price that there is substantial wiggle room in the return assumptions. This is shown in further detail in the valuation section provided later in this analysis.

The Opportunity

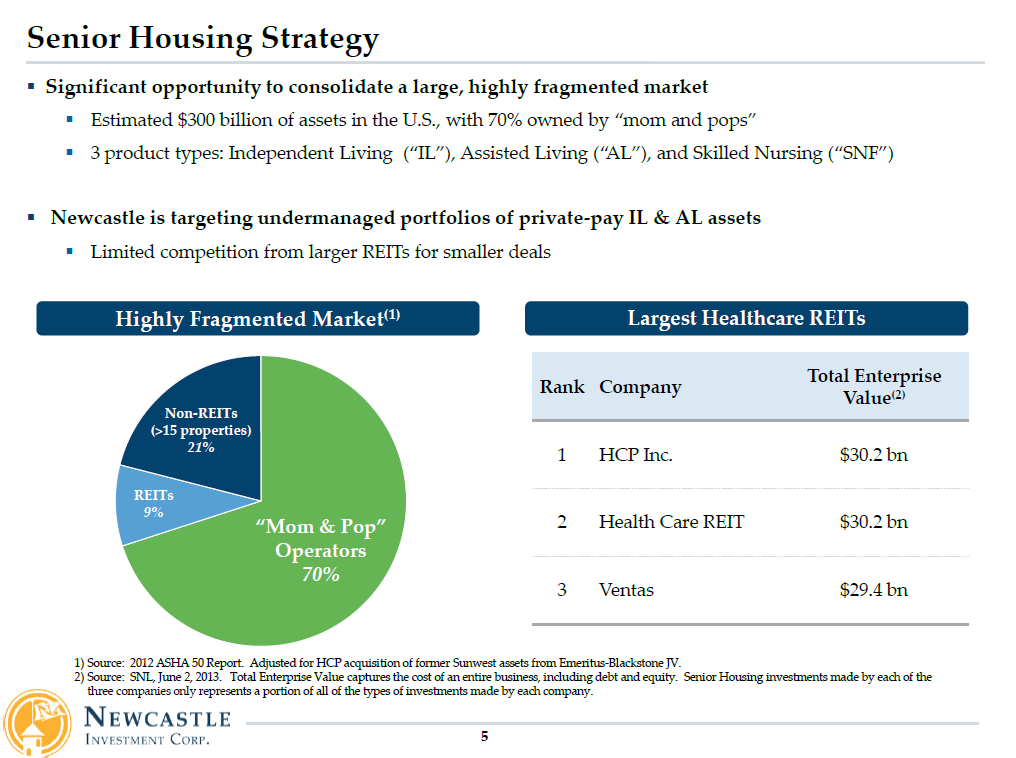

Of course, an investment in NCT only makes sense if this senior living strategy is viable over the long-term. If the Holiday deal were a one-off, then it wouldn't be terribly exciting. Fortunately, as Newcastle has recognized, the senior living market is ripe with opportunity. It's a huge market--to the tune of $300 billion--and is terribly fragmented, with 70% of the assets owned and operated by "mom and pops." NCT's acquisition of these properties brings increased efficiencies, synergies, and ultimately operating income.

(click to enlarge)

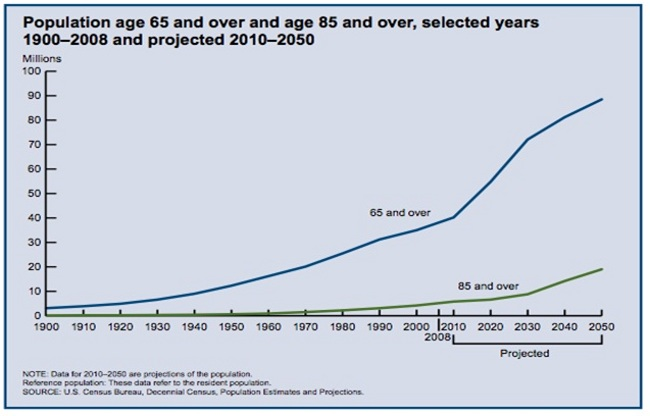

It's also no secret that America is facing a retirement crisis, as millions of baby-boomers begin retiring and need senior living care. Each day, more than 10,000 baby-boomers hit the retirement age, a trend that will continue until 2030. I won't dwell on this point--or the obvious political arguments that logically follow--but it seems pretty clear that senior care is a service that will be needed for quite some time, giving NCT plenty of opportunities to capitalize.

(click to enlarge)

As an additional point, NCT has guided towards a senior living pipeline of $800-900 million, with $300 million of that coming in the next twelve months. This was confirmed by Andrew White, Newcastle's Managing Director, in his discussion on the opportunity in senior living:

Andrew White - Managing Director

...We continue to feel very good about our strategy in the context of the overall market. This continues to be a large and highly fragmented space and so we feel very good about our prospects for continuing to source accretive deals.

The industry continues to be supported by favorable supply demand dynamics, so we also feel very good about our prospects for continued NOI growth. There has been a fair bit of conversation around new construction nationwide, but I think it's worth commenting on the fact that this is really something that needs to be evaluated market-by-market.

The reality is that the majority of construction activity is concentrating in the handful of markets like New York and Boston and Houston. And in our existing portfolio, we have very little exposures to the markets that are heating up with new construction. We're also being very selective about the markets where we're making new investments.

...Looking forward, we continue to build our pipeline. We've invested a little under $200 million of equity thus far, $163 million net of refinancings. And we have $300 million of assets in contract now, which represents an incremental $100 million of equity investments, which would take our total equity invested to a little under $300 million and $255 million net of refinancings.

We also have a near-term pipeline of over $1 billion in transactions. And as we have previously stated, this includes a mix of both large deals and single-asset deals, so it's a bit hard to predict the timing, but we feel good about the progress.

The Valuation

Valuing a REIT is always tricky because it largely depends on what kind of dividend yield the market is willing to give the security. This is typically highly dependent on risk-free rates. Additionally, the yield appropriated to REITs varies by the nature of the operating income. For instance, Healthcare REITs typically receive a lower yield than most because of the stability and consistency of the income stream. This is very positive for NCT, given that it is currently priced as a high-yielding mREIT.

Using the "big 3" Healthcare REITs--Ventas, HCP, and Healthcare REIT--as comps, I arrive at an average industry yield of around 5.57%. This compares to NCT's current 7.5% yield. (There is further upside in NCT if the typical yield of Healthcare REITs compresses).

Share Price | Annual Dividend | Yield (%) | |

Ventas (VTR) | $56.03 | $2.9 | 5.17 |

HCP, Inc (HCP) | $35.99 | $2.1 | 5.83 |

Healthcare REIT (HCN) | $53.45 | $3.06 | 5.72 |

Average | 5.57 |

Applying this new yield to NCT, we get a share price range of $7.18 based on the current dividend of $0.10/quarter. But, I actually believe this dividend level to be the floor, creating even more upside. With the Holiday transaction being accretive to the tune of 5 cents/share, and several new deals in the existing pipline, there is plenty of room for dividend increases in the next 12 months. I think management can get it up to 15 cents/quarter by the end of next year. Even better, if you add-back the New Media dividend that you will be getting, you could be looking at a 15 cent dividend as early as the first half of next year. The table gives three scenarios for the dividend (ex-New Media) next year:

Dividend/quarter | Yield (%) | Share Price | Current Upside (%) | |

Bear Case | $.1 | 5.57 | $7.18 | 33 |

Base Case | $.125 | 5.57 | $8.98 | 66 |

Bull Case | $.15 | 5.57 | $10.77 | 99 |

The Dreaded Taper and Interest Rate Risk

Any prudent REIT investor knows that interest rates, especially now, are a significant factor in the decision to commit capital. The ability of rising rates to destroy an investment thesis (see e.g., NLY, AGNC) is a very real risk that all should consider. Unfortunately, NCT isn't really any exception and will remain vulnerable to sudden interest rate changes that lead to REIT re-pricings.

What's nice about NCT, and other healthcare REITs, is that their income stream should actually increase along with higher interest rates. Most long-term leases contain escalation provisions that are greater than or equal to the pace of inflation. Although I can't confirm it, I expect that NCT as a prudent landlord would do the same. Healthcare prices also routinely increase each year, making it easier to raise rents and adding to the predictability of NCT's income growth.

Additionally, the market reaction to the Fed's $10 billion taper on 12/18 may prove to be instructive on how the stock will react as the taper unfolds. Like most REITs, NCT traded up close to 2% when the Fed minutes hit the wire. Other Healthcare REITs traded up as well. It nevertheless remains to be seen how NCT will behave long-term with the dreaded taper finally beginning, but hopefully the market's initial reaction proves to be prescient.

In any event, however, so long as rates only climb modestly over time, I suspect that they won't have a significant impact on the NCT investment thesis. There is also so much upside in this situation that, even if higher rates put a damper on NCT, investors should still be able to make out with a sizable profit. I see this as a "heads I win some, tails I win a lot" situation. Those are coin-flips you should take every time.

The Risk of Dilution

Dilution is another serious risk that prudent REIT investors should consider. Because REITs must pay out 90% of their taxable income (in the form of dividends) to retain preferential tax treatment, they often issue additional shares to fund new investments. As I mentioned previously, NCT recently completed a large secondary offering and raised ~$250M in proceeds.

Nevertheless, at this point, it seems unlikely that NCT will near-term need to raise more capital to fund its aggressive growth agenda. This is because NCT's capital is actually coming from its CDO business. As it continues to collapse its CDO holdings, it raises new cash that can be deployed into senior living acquisitions. New equity would only be issued in the event of a large purchase (probably a net-positive for NCT anyway) -- which is what happened with the recent Holiday acquisition. As such, if you see a large NCT secondary, you are likely to see it quickly followed-up with a large purchase of senior living real estate. NCT's Chairman, Wes Edens, confirmed this financing strategy on their Q3 2013 conference call:

Wesley Edens - Chairman of the Board

Well, we expect to fund the ordinary course investments on the senior housing business through cash on hand as well as from incremental capital coming out of the debt business. And it's not a precise walk forward that when we run our numbers out for the next couple of quarters we've got sufficient capital to fund everything that we've got in the pipeline right now. And I expect that that will continue.

What will change that a little bit is if we were able to buy one of these larger portfolios, we'd probably have to go and raise capital, if that was something that came in the past, it'd be a happy day because it would be a chunk of capital at very, very attractive prices. But we have done a good job, I think the company, has done a good job of managing both the flow of capital out of the debt business and in the deployment of it on the senior housing side. And maybe you can walkthrough with John at some point as you like, but those numbers look like they're going to be fine to us.

The "Re-Rate"

So, I've mentioned that I expect the market to eventually re-rate NCT as a Healthcare REIT and compress its yield to trade more in line with its peers. These types of trades can be frustrating because they seem like a "hurry up and wait" strategy. You hurry to go out and buy the stock, only to start waiting for the market to finally "get it." This can definitely test your patience, and could very well be the case with NCT.

As a potential solace, look to the New Media spin-off as the catalyst that ignites the market's re-rating of NCT. Again, this is expected to take place in Q1 2014. With the spin of New Media complete, investors will simply have no choice but to look at NCT as a Healthcare REIT. Recall that its only other business segment is the CDO business, which we know is being collapsed to fund senior living acquisitions.

In my experience, these types of events often transpire when you least suspect them. Take comfort in NCT's enormous yield in the interim, and I can assure you that one day you will wake up and be pleasantly surprised at the share price. Hopefully it is sooner rather than later. My money is on March 1, 2014 at the latest.

Conclusion

NCT is a fantastic coming of "age" story. It is undergoing an incredible transformation into a Healthcare REIT and will soon derive substantially all of its income from senior living properties. This income is predictable and stable, and should have the effect of compressing NCT's yield to be more in line with its Healthcare REIT peers--a yield significantly lower than where it is currently trades. If management can execute the transition successfully, and I have no reason to believe that they cannot, there is considerable upside in the next twelve months with very little downside risk. The best part is that, while you wait, you can continue to collect its 7.5% yield and perhaps earn additional upside from the New Media spinoff. The risk/reward trade-off is one of the best I have ever seen, making it my best idea for 2014.

Disclosure: I am long NCT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire