Editors' Note: This article covers a stock trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Bottom Line Up Front

Most do-it-yourself investors have little say in the political policy that they are subjected to. If you are like me, you lack the charisma it takes to convince others of your political positions, no matter how much time spent in heated debate over roasted foul and jellied bog fruit. Point being, you are subject to the whims of the masses, whether they produce sound decisions or not. But every decision has an impact, and wherever the general populace ignores the consequences of their decisions, opportunity knocks. I think that current calls for minimum wage hikes are creating value in companies that manufacture automation products, such as RFID (Radio Frequency Identification), robotic hardware, and software. I discuss why to focus on automation and not macro results here.

Current Situation

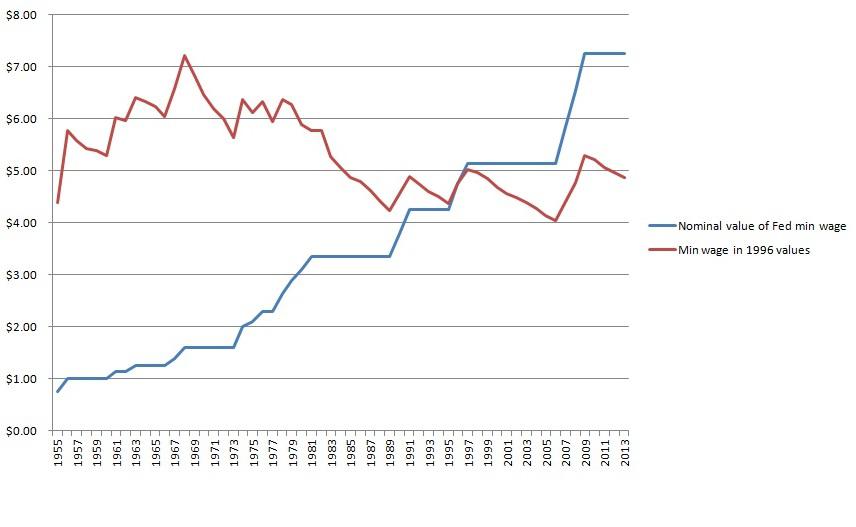

As I'm writing this, President Obama is proposing a raise in the federal minimum wage to $10.00 an hour from its current $7.25 (for more read here, and here). Adjusted for inflation, this would be somewhat below its peak in 1968 (roughly 16% lower). However, this rate would be in line with most of the other rates of the 1960s and 1970s, and well above what has been paid in the past 3 decades. California recently raised its minimum wage to $10, enacted over the next two years, and Washington State, already leading the nation in minimum wages, recently made news when a Seattle suburb, SeaTac, raised their minimum wage to $15.00 an hour. The higher proposed figures far outpace any minimum wage rate mandated in U.S. history. Here's a graph I included in my instablog that sums up recent federal minimum wage history:

(click to enlarge)

I built the graph from data provided by infoplease.com here.

Because the graph doesn't show minimum wages prior to 1955 (minimum wage passed its last legal hurdles in 1938), it seems as if today's rates are near their lowest. In fact, they are much higher in terms of purchasing power than much of the law's history. Still, rates depicted on the graph go back far enough to cover discussions relevant to this article.

Where's The Beef?

From my perspective, there is little reason to expect macro benefits from the currently proposed minimum wage hike. Nor do I predict any kind of economic disaster. Since no new value is being created, prices and wages are likely to find a new equilibrium and things are likely to proceed, more or less, as they have in the past. Most likely, there will simply be fewer entry level jobs. The remainder of the new labor burden will be covered by moderate price increases, which will, ironically, hit those who are employed, or used to be employed, in low wage positions. But what's important for our today's discussion is to realize that when the hand of Washington reaches down and takes from one pocket to put in another, there are bound to be effects. We need to identify where business investment dollars will flow in reaction to the new costs.

The first clear winners will be companies that provide the solutions to low wage industry's labor cost problem. One industry that may benefit in particular is RFID (Radio Frequency Identification).

For those who are not familiar, RFID uses radio-frequency electromagnetic fields to transfer data, which can be used to rapidly (almost instantaneously) identify and track objects via tracking tags. Pertinent information is stored electronically on the tags, depending on the purpose of user's desire. Useful distances vary based on the transmission device and wavelength (magnetic fields, microwaves, or UHF radio). Because the tag and reader don't require line of sight, and range can be significant, RFID is much more versatile than standard barcodes.

Furthermore, RFID technology is already proven and in use. Utilization is expanding rapidly. Some of the ideas thrown around for RFID have remained cost prohibitive and technically problematic. But faced with a 15% jump in labor costs, Wal-Mart (WMT), for instance, may make the leap from tracking inventory with RFIDs to installing an automated checkout system. Once Wal-Mart does so, other retailers/grocers will follow. Three publicly traded companies which may provide exposure to RFID expansion are Gaming Partners International (GPIC), Checkpoint Systems Inc (CKP), and Hewlett-Packard Co (HPQ). All three companies appear somewhat healthy and moderately cheap. All three cover various aspects of the market (from casino/gaming to retail use, to commercial data management). Hewlett-Packard, not strictly an RFID company, has invested millions in both improving its own logistics and distribution through the use of RFID, and producing data management products for businesses and agencies such as the Veteran's Administration. Still, if HPQ can leverage its expertise on RFID usage to retail customers, they may benefit from an overall industry surge. Data below on each company was kindly provided by Finviz.com.

Gaming Partners International Corp. | |||||

Valuation | Health | Growth | |||

Quick Ratio | 4.1 | EPS | 0.43 | ||

Dividend | - | Current Ratio | 5.1 | EPS this Y | 66.70% |

Dividend % | - | Debt/Eq | 0 | EPS next Y | 138.89% |

Book/sh | 5.77 | LT Debt/Eq | 0 | EPS next 5Y | 25.00% |

P/E | 19 | ROE | 7.40% | ||

Forward P/E | 19 | ROI | 12.40% | ||

PEG | 0.76 | ||||

P/FCF | - | ||||

Checkpoint Systems Inc | |||||

Valuation | Health | Growth | |||

Quick Ratio | 1.5 | EPS | -0.64 | ||

Dividend | - | Current Ratio | 1.9 | EPS this Y | -108.70% |

Dividend % | - | Debt/Eq | 0.24 | EPS next Y | 81.14% |

Book/sh | 8.99 | LT Debt/Eq | 0.15 | EPS next 5Y | 45.00% |

P/E | - | ROE | -12.70% | ||

Forward P/E | 18.03 | ROI | -26.10% | ||

PEG | - | ||||

P/FCF | 20.75 | ||||

Hewlett-Packard Co. | |||||

Valuation | Health | Growth | |||

Quick Ratio | 1 | EPS | 2.63 | ||

Dividend | 0.58 | Current Ratio | 1.1 | EPS this Y | 140.90% |

Dividend % | 2.16 | Debt/Eq | 0.83 | EPS next Y | 2.97% |

Book/sh | 14.22 | LT Debt/Eq | 0.61 | EPS next 5Y | -2.40% |

P/E | 10.23 | ROE | 20.80% | ||

Forward P/E | 7.12 | ROI | 11.50% | ||

PEG | - | ||||

P/FCF | 7.06 | ||||

Each company has its strengths and weaknesses, and this list serves as a cursory glance at some potential investments. As always, I recommend your own due diligence. Simple metrics like those above don't expose many of the pitfalls that might be hidden away in a company's operations.

Of the three, I plan on analyzing Hewlett-Packard and perhaps Checkpoint Systems as potential long positions. I like Hewlett-Packard's current pricing and expertise in RFID, but Checkpoint is a more direct play on the thesis, and when growth is accounted for, may still prove to be currently underpriced.

Other companies that may benefit are retailers who have less employee interface with their customers and have an easier road to automation than their competitors. Companies such as Google (GOOG) and Amazon.com (AMZN) are two companies whose automation dreams have been in the news lately. Both of them are likely to benefit from a surge in labor costs, even if recent public announcements and speculation prove to be more buzz than reality.

Amazon's Octocopter (what's that?) isn't likely to end up a reality… at least, not as currently envisioned. But Amazon serves as a useful example for two reasons.

- They don't have armies of sales personnel and checkout attendants to maintain, unlike their brick and mortar competitors. While minimum wage hikes (and the corresponding rise in low wages above minimum wage levels) are likely to hit Amazon somewhat, they are almost certainly less vulnerable than their 20th Century style competition. Anything that helps Amazon establish lower prices than its competitors will obviously help bolster revenues, and may even allow Amazon to garner profits where it has been unable to do so recently.

- Amazon.com, and retailers like it, won't face the enormous conundrum that brick and mortar retailers face. While Best Buy (BBY) or Wal-Mart may automate checkout lines to mitigate high labor costs, they will do so at a cost. They must convince customers that automated checkout lines are secure, and ultimately desirable. They must maintain enough employee presence or risk losing customers who preferred human interaction over a streamlined online experience. Amazon doesn't have to convince its customers to forgo employee interaction, its customers are already the ones willing to do just that.

It's hard to justify Amazon's current nosebleed valuations, but rising labor costs for traditional retailers could bolster Amazon longs' hopes that their company's profit margins will improve, thereby delaying or preventing any sharp drop in prices.

Google's advantages in a rising low wage labor cost world are long-term plays. But with Google valuation bordering on cheap (for a tech company), waiting for long-term investments to pay off seem like a better bet than hoping Amazon's advantages eventually justify share-price. Finviz.com lists Google's forward P/E as 20.6 and its P/FCF as 29.91.

Google's robot delivery service is currently vaunted by the media, but its purchase of 8 small robotic companies this year offer more lucrative opportunities. First, Google can leverage robotics to reduce the costs of assembling products its subsidiaries produce, such as Moto-X. But such advantages are more of a keep up game, and Google's real aim may be a bit more in line with its core competency; dealing in data. Recent purchases, such as Boston Dynamics, which builds robotics for the U.S. military seem to support my theory that Google aims to capture the market on robotic software, developing the protocols that run not only any hardware they manufacture, but perhaps the robots that other companies manufacture as well. Essentially, Google is positioning itself as a leader in some of the most important drivers of future economic and scientific development. It will most likely be Google hardware and software inside the robot manufacturers building our goods and delivering them, and it will be Google robots exploring and mapping space and the deep oceans.

Conclusion

Minimum wage hikes are, in all probability, coming soon. "Money to help our nation's downtrodden straight from the pockets of greedy fat cats" is a strong narrative, and one the general public is probably willing to buy into without much thought towards who it will really affect or what effects it will ultimately have. As investors, we do not have that luxury. Opportunities and risks are the winds and currents we navigate towards profitability, and they are often driven by national policy changes. While the ultimate benefits and costs of such a contentious policy can be hard to calculate, predicting near term reaction of those affected shouldn't be more manageable. Raising wages will raise labor costs. Automation options have been on the table since the industrial revolution, but one could argue there have never been as many options on the table as there are today. Raising the cost of labor simply means options that are just outside the realm of "worth doing", suddenly appear viable. Increased use of automation at the margins mean costs for other forms of innovation should fall. If we want to benefit from the gold rush, we should invest in the shovel makers.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in GOOG, HPQ, CKP over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire