Fellow Seeking Alpha contributor Itinerant, wrote a recent article titled "Sorry Gold Miners...You Are Not Putting A Floor Under The Gold Price" in which he made the argument that there is no floor beneath the gold price when it comes to miners costs. Additionally, he stated the following:

- Gold prices are falling, but so are costs.

- Gold mine output is actually rising despite the falling gold price.

- The gold price does not give a rat's neck about mine supply.

We wanted to take this opportunity to provide the alternative argument, respectfully disagree with the thesis of the article, and correct some issues we find with the logic of the article.

Gold Prices are Falling, But So Are Costs

This argument is essentially based on the reported All-in Sustaining Costs (AISC) and All-in Costs of the miners in Q3FY13. Now, we won't get into the details of why AISC is not an accurate measure since that deserves a separate detailed post, but investors should remember that AISC still leaves out such things as taxes and financing costs, but perhaps more importantly, it leave much leeway for individual miners which may make the calculations a bit subjective depending on the miner. Even Barrick Gold (ABX) acknowledges this in its third quarter financial report with the following:

These measures are not representative of all of our cash expenditures as they do not include income tax payments, interest costs or dividend payments.

But regardless, let's assume that we live a world without financing costs, taxation, and that individual miners are honest and straight-forward and would never pretty-up their results for investors and analysts.

Itinerant is absolutely right, and according to his post they dropped from $1187 per ounce in Q2FY13 to $1006 in Q3FY13. We may dispute those exact numbers, but we do not dispute the fact that they did drop from Q2FY13 to Q3FY13 - that's shown up in our own true all-in costs which we will publish in the next couple of days. So it would be fair for someone looking at the industry to say gold costs are dropping - but we believe that just like many things you have to really peel off the layers of this onion to see what's really going on.

Remember for almost a decade miner costs have been rising every year, but the argument goes, that with a snap of a finger they could cut costs by 10% without any long-term consequences to their operations. We find that extremely hard to believe, and the fact that almost all miners have cut costs in unison from the second quarter to the third quarter supports this belief - industry wide cost cutting to such a large degree points more to cutting exploration costs and high-grading their mines than anything else. Both of these are quite destructive to the long term viability of the industry as cutting exploration means future gold supply is being cut, and high-grading destroys the lifespan of existing mines.

So Itinerant may be right that costs did fall over the last quarter - but this is absolutely not a signal that costs are falling on a permanent basis, and instead it suggests that future costs are going to be much higher. This is hardly a strong argument when analyzed with a more detailed look.

Mine Output Increasing

Itinerant states:

2013 is forecast to become another record year in terms of gold production; and despite calls to the contrary 2014 is set to surpass this year's output yet again. While only a few mines have actually been put on care and maintenance in 2013, output has actually increased at many other mines due to high-grading and other practices designed to reduce costs per ounce.

There are no cited numbers here by Itinerant but we will do that for him by citing Thomson Reuters GFMS, which forecasts 2013 gold output of 2,920 tonnes for 2013 versus 2,861 tonnes in 2012. We're going to publish our own analysis of production statistics for 2013 based on the production of the major mining companies and we have a feeling that their predictions are a bit high, but even if we take the GFMS numbers at face value that means that production is increasing by a massive 3% or about $2.4 billion dollars at current gold prices. That's less than two days of US Federal Reserve Quantitative Easing ("money-printing") after their recent $10 billion dollar cut. So the estimated increase in gold production is equivalent to less than two days of what the Fed is printing - hardly an increase that would run the street rich with unwanted gold bars.

This also neglects the point that the author mentioned in his own article that much of this is due to high-grading, which would REDUCE future mine supply as we've explained earlier.

Finally, all gold investors should take a look at a chart from our earlier article based on a speech by the Barrick Gold CEO.

(Click to enlarge)

What you'll see is that as gold rose 400% or so, mine production rose a mere 6% - and that was in the greatest bull market in gold over the last 30 years where gold rose in price every single year. What do investors think will happen when gold actually falls in price? Production will increase significantly? We highly doubt it and think that many of these brokerages will be adjusting their gold production reports downwards over the next 6-12 months. But then again anybody taking Econ101 could make that same prediction that as the price drops output will also drop so we can't take all the credit here.

The floor that never was

Finally, Itinerant closes with the following argument:

As we have argued in the past gold does not vanish from the surface of the earth once it is mined. It may be stored in vaults, worn around necks or minted into coins but it is rarely "consumed" like most other commodities are. Almost all of this gold can be considered for sale under the right set of circumstances or for the right price. Any newly mined gold merely adds to the overall above ground stock. And this addition is a mere drop in the ocean.

Gold price and gold mining are only interacting in one direction: the gold price has an immense influence on the financial well-being of miners; but not vice versa. Gold miners are presented with a price for their goods by the powers that be, and need to make do as best as they can.

This is perhaps the most misunderstood concept in the gold market - the facts are correct but the conclusion is wrong. Yes gold mine production is a mere drop in the bucket of total existing gold stocks, but that doesn't mean that it is not a significant contributor to the gold supply picture.

We've dealt with this issue extensively in a previous article, so investors wanting the details can refer to that article, but we will briefly summary it now. This argument is based on the premise that the total amount of existing gold is around 171,000 tonnes (we and others have questions about the accuracy of this number, but we will use it since it is probably the most cited amount), while according to the USGS, new mine supply is around 2700 tonnes per year. That means that total newly mined gold only adds 1.5% to total gold inventories, and thus can have little impact on the price.

The problem with this argument is that the great majority of the above-ground gold stock is not up for sale. Sentimental jewelry, heirloom artifacts, central bank gold reserves, industrial goods with gold content, forgotten/buried gold, and even everyday jewelry is not gold that is up for sale except in exceptional circumstances. For example, the gold reserves of the top 40 central banks make up around 30,000 tonnes (a little less than 20% of all existing gold), this is gold that exists but cannot be counted as gold supply because it is not available to the market.

It may be better for investors to think of total existing gold supply similar to the way we think of shares of stock in a company. Total existing gold is like outstanding shares, gold actually available for sale is like the stock's float, and newly mined gold supply is like new share issuance. Holders of gold who have no intention to sell (whether for political, economic, or investment reasons), are shareholders but their shares are not part of the current "gold float" and are thus not able to satisfy demand.

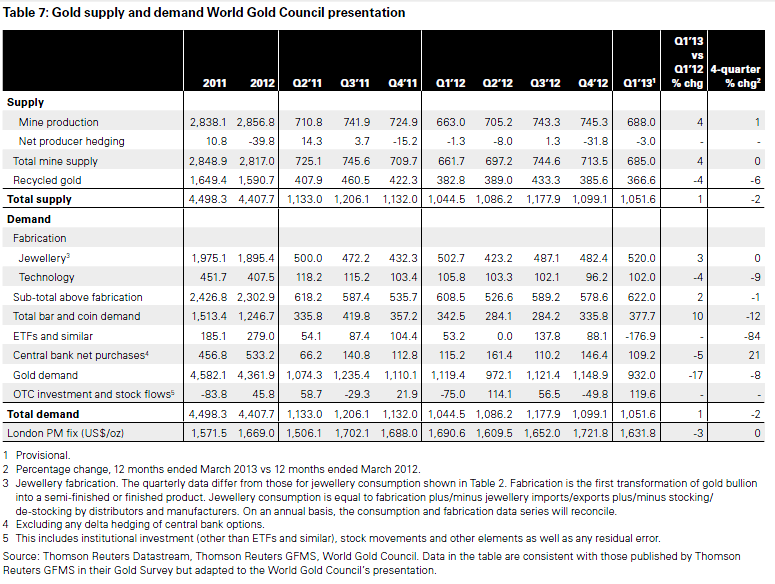

Nobody knows for certain what "gold float" is available to satisfy demand, but we can take supply data from the World Gold Council (WGC) to give us an idea. According to the WGC, gold supply for 2012 was 4408 tonnes as shown in the following table:

(Click to enlarge)

As you can see, newly mined gold supply makes up a great majority (about two-thirds) of annual gold supply.

The big flaw with the above-mentioned argument, is that it assumes that all existing gold stocks are on the market at current prices -- which is simply not true. As we have mentioned, some gold is not available to the market at any price (try offering the US Treasury a nice premium for its gold bars and see how many get sold to you), while other gold is only available at much higher prices. If prices rise to much higher levels then of course "gold float" will increase, but in the absence of significant price shocks then gold supply from existing gold stocks is a relatively small percentage of existing gold. As we can also see, mined gold supply makes up a large percentage of the gold available to market and thus it is very relevant to determining price.

Understanding the difference between "total gold stocks" and "gold available for sale" is critical to a true understanding of mine supply. Throw in the fact that recycled gold stocks are plummeting because investors that bought physical gold have no desire to sell their gold at current prices, and you have to give mine supply even more importance to the current gold supply picture.

Investors don't need to look any further than India, which is arguably the country with the largest above-ground gold stocks, yet the premiums for gold approach 25% over the current spot price. A lot of gold but very little available for sale, so it's not a question of how much gold exists above ground, but rather what portion of that is available for sale - and that portion is declining significantly with the gold price.

Conclusion For Investors

With the gold price dropping the sentiment amongst many commentators and newly minted gold bears is decidedly negative. Many arguments explaining why basic economic theory doesn't hold for gold and how the price will drop way below costs of production are emerging - which is what always happens when an investment rises or falls significantly (and also shows which side of the bandwagon most people are on).

We think gold investors should be a bit more prudent and really take a hard look at the gold picture. We believe that our reasoning shows that those calling for a much lower gold price or how mine production costs are completely irrelevant, are simply jumping on that sentiment bandwagon and using the price action to justify their reasoning. But this is very dangerous because as Ben Graham, the father of value investing stated:

In the short run, the market is like a voting machine -- tallying up which firms are popular and unpopular. But in the long run, the market is like a weighing machine -- assessing the substance of a company.

We couldn't agree more and in the long-run we believe that the basic fundamentals of economics, gold, and money supply growth will assert themselves. We stick with our call that even though it is difficult to buy (it always is hard to buy during bottoms - that's why most people miss them), but gold investors should hold tight and even accumulate more physical gold and the gold ETF's [SPDR Gold Shares (GLD), PHYS, CEF). For investors looking for higher leverage to the gold price, they may want to consider miners such as Goldcorp (GG), Agnico-Eagle (AEM), Newmont (NEM), or even some of the explorers and silver miners such as First Majestic (AG)].

We don't believe the gold bull-run is over and we do believe that miner costs do put a floor under the gold market in the medium to long-term. Current gold prices will not be sustainable for gold miners and we will see even more mine closures, bankruptcies, and production cuts if they stay below $1200 or $1300 for more than a few quarters. We shudder to think what will happen to the gold industry under $1000 as some are calling for - they simply have no understanding that gold is more than a symbol trading on the market to be technically analyzed and prognosticated and that physical gold has to actually support these paper-market instruments.

In the meantime we will be accumulating physical gold and mining equities because as Brent Johnson of Santiago Capital says, "If you believe in math buy gold." We can't say it any better.

Disclosure: I am long SGOL, AG, GG, SIVR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire