This is Part 1 of the series: Asset Allocation: What's Right for 2014 and Beyond

It's the time of year when investors and investment managers alike plan on how to position their portfolios for success in 2014. Part of the value that wealth managers deliver to clients is advising them on proper asset allocation. In fact, it's a very important part - research has shown that about 90% of return and risk for a balanced stock-and-bond portfolio comes from asset allocation1.

In this series, I focus on the biggest asset allocation decision - equities vs. fixed income. A typical recommended allocation for individuals who are between 45 and 60 years old is 60% stocks, 40% bonds. Most pension plans and endowments also hold a similar 60/40 aggregate asset mix. This Part 1 article covers mainly fixed income.

Not so boring in the last 30 years!

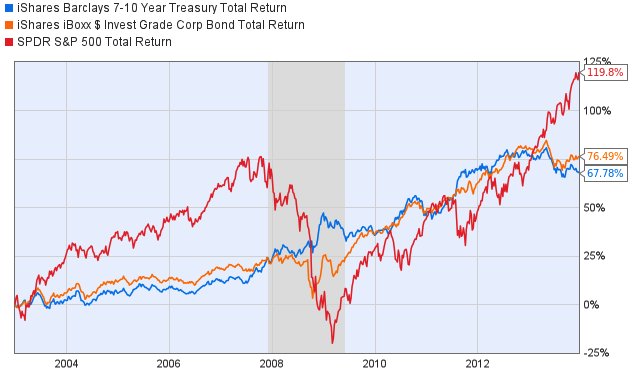

Let us start with the "boring" part - bonds - which are generally considered low-return, low-risk asset class. But bond returns were not so low in the last 30 years. U.S. bonds experienced a 30-year bull run as interest rates were falling from their peak in the late 1970s. That's because long-term fixed-rate bond prices move in the opposite direction to interest rates: as rates fall, bond prices rise, and vice versa. For example, the iShares Investment-Grade Corporate Bond index ETF (LQD) returned 80.4% in 10 years ending Dec 31, 2012, or 6.1% per annum! This return was higher than the S&P 500 (SPY) for the same 10-year period (5.45% p/a). Although corporate bonds experienced significant volatility in 2008, they ended that year with a positive 2.4% return (iShares 7-10 year Treasury bond ETF (IEF) gained 17.9% that year).

U.S. Stock and Bond Returns, 2002-2013

(click to enlarge)

The bond party ended in 2013. According to Bill Gross's famous May-10th tweet,

The secular 30-yr bull market in bonds likely ended 4/29/2013

He is right so far, and with incredible precision at that! The 10-year Treasury yield hit the low of 1.63% on May 1st, and has been rising ever since, to 2.9% currently. Corporate bonds delivered -2.2% YTD total return, and Treasuries returned -5.4%. If rates keep rising, as most investment managers expect (and I agree), bond returns will be close to zero or negative in the next few years.

Source: Department of the Treasury

Numbers part (may be skipped with no loss of meaning)

The sensitivity of bond prices to rates is known as duration, and is higher for longer bond maturities. Duration for both 7-10 Treasuries and corporate bonds is about 7.5 (see table below). This means that if rates rise by 1%, bond prices will fall by roughly 7.5% = 1% x 7.5 (though the true price sensitivity is less than that due to what's called "convexity"). We then add coupon interest to obtain total return. That's what happened to Treasuries this year - as 7-10 year rates rose by about 1%, their price dropped by 6.9%, plus interest, to give -5.4% total return. Corporate bonds lost less than Treasuries as they benefited from additional gains as a result of tightening in credit spreads, and from higher coupon.

Zero expected return

Suppose we think that interest rates had most of their initial rise this year, and we expect them to rise by just 0.5% in each of the next 2-3 years. If corporate spread to remain constant, we would then expect the total return for corporate bonds to be close to zero, and for Treasuries to be negative (because of their lower yield). If rates rise by more than 0.5% in any year - a scenario with significant chance - the total return on corporates will likely be negative as well. Significant risk with zero expected return - clearly not an asset class to be in. We recommend reducing most long-term Treasury and corporate bonds, or avoiding them altogether if you can.

Sources: iShares, SPDR, PowerShares

But where would we allocate this portion of the asset mix? Our answer for listed assets consists of three parts:

- Strategic asset allocation - reduce fixed income, increase U.S. equities

- Within fixed income - reduce (or eliminate) long-term fixed-rate bonds, increase loans

- Devote a portion of portfolio to tactical asset allocation (TAA)

Part of the answer is TAA - actively managing portfolio allocation between stocks and bonds, instead of a static asset mix. We think that TAA, done properly, has significant potential to improve return and reduce risk. At this point, we are really positive on U.S. equities, both over the short-term (3-6 months) as part of TAA, and for SAA (2-3 years) - more on this will be coming up in Part 2 of this Asset Allocation series - please stay tuned.

Fixed income, not fixed rate

Alternatives are quite limited, as the Fed brought short-term rates near zero, and is likely to keep them there - even the 2-year Treasury yield is just 0.32% (see the yield curve chart above). Short-term 2-3 year corporate bonds (SCPB) have low duration, but will earn you only 1%.

As part of the reduced fixed income allocation, we recommend holding bank loans and floating rate corporate bonds. Senior secured bank loans (BKLN) pay a floating coupon (Libor plus a fixed spread), and are therefore not exposed to the rise in long-term rates - in fact, they would benefit from eventual rise in Libor (though not likely in next 1-2 years). The spread is currently wide enough to give the total current yield of about 4.1%.

Note that "senior" loans must not be confused with high credit quality. In fact, these loans are rated below investment grade ("junk") by Moody's and S&P, and therefore come with associated credit risks. Similar to high-yield bonds, they are appropriate for investors who are comfortable with this type of credit risk. However, their security of collateral, and the senior position in the issuers' capital structure mitigate the credit risk to some degree.

1. Significant work include research papers by: Brinson et.al. (1986, 1991); Ibbotson & Kaplan (2000)

Disclosure: I am long SPY, BKLN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire