As an income-driven investor who doesn't mind the occasional conservatively-yielding dividend play, I've decided to shift my focus to the quick service restaurant sector and highlight several of the reasons behind my decision to remain bullish on shares of YUM! Brands (YUM).

#1: Recent Performance & Trend Behavior

On Friday, shares of YUM! Brands, which currently possess a market cap of $33.25 billion, a forward P/E ratio of 20.28, and a dividend yield of 2.02% ($1.48), settled at a price of $73.39/share. Based on their closing price of $73.39/share, shares are trading 1.92% below their 20-day simple moving average, 2.89% above their 50-day simple moving average, and 4.53% above their 200-day simple moving average. These numbers indicate a short-term downtrend and a mid-to-long-term uptrend which generally translates into a near-term selling mode for traders and a moderate buying mode for longer-term investors.

(click to enlarge)

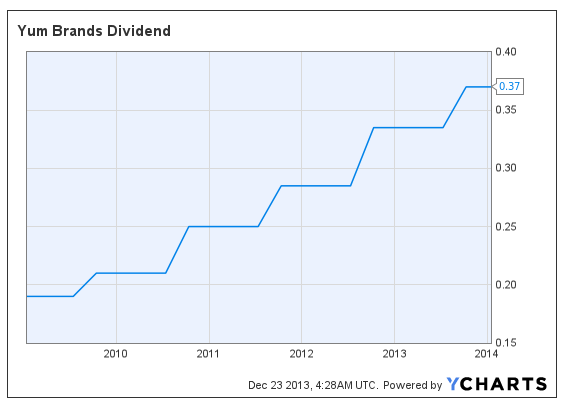

#2: 5-Year Dividend Behavior

Since October 15, 2008, the company has increased its quarterly distribution five times in the last five years, with the most recent increase having taken place in October of this year. The company's forward yield of 2.02% ($1.48) coupled with its ability to maintain its quarterly distribution over the last five years, make this particular restaurant play a highly considerable option, especially for those who may be in the market for a conservative stream of quarterly income.

(click to enlarge)

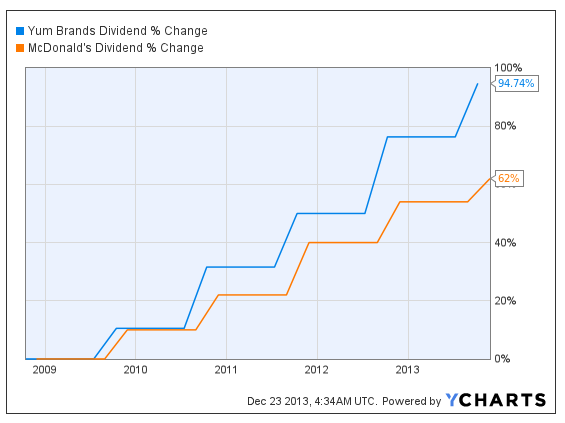

#3: Comparable Dividend Growth

Not only does the company's 2.02% dividend yield and 5-year dividend behavior make this particular stock a highly attractive option for most income-driven investors, its dividend growth over the last five years versus one of its sector-based peers is also something investors should almost certainly consider. From a comparable standpoint, YUM! Brands' dividend has grown a solid 94.74% over the past five years, whereas the dividend growth of its sector-based peer McDonald's (MCD) has only increased 62% over the same period.

(click to enlarge)

#4: Looking Ahead To Q4 Earnings

If we begin to look ahead to the company's Q4 earnings estimates, in which analysts are calling for YUM to earn $0.81/share in terms of EPS (which is $0.04/share lower than the company had reported during Q3) and $4.28 billion in terms of revenue (which is $730 million higher than the company had reported during Q3), I suspect most investors would like to see an improvement over the company's Q3 results which came in at $0.85/share in terms of EPS and $3.47 billion in terms of revenue.

If the company can demonstrate an increase of at least 1.25%-to-1.50% in terms of same-store sales at both its U.S. locations and its Yum Restaurants International locations, and find a way to improve on Yum China's operating profit which was down 11% on a year-over-year basis for Q3, I see no reason why such EPS and Revenue estimates can't be met or even slightly exceeded when the company announces its Q4 results.

Risk Factors (Most Recent 10-K)

According to the company's most recent 10-K there are a number of risk factors investors should consider before establishing a position Dunkin Brands. These risk factors include but are not limited to:

#1 - Yum! Brands Chinese operations subject the company to risks that could negatively affect its business.

#2 - The company may not attain its target development goals, and aggressive development could cannibalize existing sales as well as future operating results.

#3 - The company's failure to drive both short-term and long-term profitable sales growth through brand relevance, operating excellence, and the opening of new restaurants under its numerous brands could result in poor financial performance over the next several years.

Conclusion

For those of you who may be considering a position in Yum! Brands I'd keep a watchful eye on a number of things over the next 12-24 months as each could play a role in both the company's near-term and long-term growth. For example, near-term investors should focus on the recent performance and trend behavior of the company, while longer-term investors should focus on the company's upcoming Q4 earnings as well as its ability to continuously increase its dividend on an annual basis as has been the case over the last five years.

Disclosure: I am long YUM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire