Quick Overview - Wirecard AG (OTCPK:WRCDF)

Wirecard (OTCPK:WRCDF) has two main businesses: (1) Providing an outsourced solution for e-commerce payments - including payment acceptance, payment processing, and risk management (e.g. fraud prevention). (2) Providing customers with a white label credit or prepaid debit card solution - issuing, managing accounts, and processing payments. They are moving into the mobile payments area in both of their business lines. Wirecard is headquartered in Ascheim, Germany and trades on the Frankfort stock exchange and on the OTC Pink market. Market Cap = $4.35 B, PE (TTM) = 41.3 (at closing price of $38.8 on 12/20/2013).

Recommendation - Buy WRCDF

Wirecard has established partnerships with leading European mobile phone providers - Vodafone (VOD), Telefonica Germany (OTC:TELDF), and Orange (OTCQB:FNCTF) and is well positioned to grow rapidly as the European mobile payments market begins to take off. They are benefiting from strong long term growth trends in e-commerce, credit/debit card payments, and mobile payments. Recurring revenues based on transaction volume provide a stable base for growth. Goldman Sachs sees strong growth ahead for Wirecard and has put it on its conviction buy list.

Sell targets for different investment timelines are listed below. Sell targets are based on the Risk Based Valuation (see details below). Returns are based on the closing price of $38.80 on 12/20/13.

- Investors with a < 6 month timeline should sell above 44.6 for a 14.8% return

- Investors with a 1 year timeline should sell above 50.3 for a 29.7% return

- Investors with a 3 year timeline should sell above 68.5 for a 76.4% return

- Investors with a 5 year timeline should sell between 74.9 and 144.2 for a 100.7% to 266.6% return

Investment Thesis

The investment thesis for Wirecard is based on three key points:

#1: Investments in mobile payments products will give Wirecard a strong position in a market that is poised for take-off.

The mobile payments market is in its early stages and is expected to grow rapidly through 2017. "We expect global mobile transaction volume and value to average 35 percent annual growth between 2012 and 2017, and we are forecasting a market worth $721 billion with more than 450 million users by 2017," said Sandy Shen, research director at Gartner. Wirecard has invested in product development creating a mobile wallet solution that supports peer to peer money transfers, mobile phone internet purchases via apps, and in-store purchases. They are also leveraging their core payment processing & debit/credit card outsourcing in the mobile payment arena. They have established strategic partnerships with 3 leading European mobile phone providers - Vodafone, Telefonica Germany, and Orange.

#2: Long term growth trends in e-commerce and debit/credit card usage.

Wirecard's core business is payment processing for e-commerce transactions (~69% of revenues). Consumers are shifting more of their spend online. The IDC projects rapid growth in global e-commerce sales through 2017:

"E-commerce sales for physical goods, like clothes and consumer electronics, will grow 18 percent annually on average over that period, outpacing U.S. growth of 7 percent. The figures don't include online sales of items like movie tickets, software or travel bookings."

Roughly 31% of Wirecard's revenues come from its white-label debit/credit card business. Transaction volumes in this business will grow as consumers continue to shift to debit & credit cards instead of using cash or checks. According to the 2013 World Payments Report, growth in non-cash transaction volume is in a strong upward trend:

"Our estimates for 2012 indicate that non-cash transactions will maintain a steady upwards course, though down slightly on 2011 rates, with an increase of 8.5% to reach 333 billion transactions."

#3: Recurring revenues provide a stable base for growth.

As an outsourced services provider, Wirecard generates a continuous stream of revenue based on the customer transactions that it processes. Outsourcing relationships tend to be long term in nature and there can be substantial switching costs for Wirecard's customers. This leads to a relatively stable on-going book of business that Wirecard can continue to grow as it adds new customers.

Risk-Based Valuation

The risk-based valuation for Wirecard estimates a worst case, expected, and best case investment return over a 5 year time horizon.

Stock Price = (Revenue * Net Margin / Shares Outstanding) * P/E … based on 5 year forward projections

The waterfall chart below shows the relative impact that projected changes in revenue, net margin, shares outstanding, and P/E have on Wirecard's estimated valuation (expected case, 5 year forward view). Revenue growth has the greatest impact, driving 101.1% price appreciation. Net margin growth drives a 59.5% positive return, increase in shares outstanding decreases return by 24.6%, and P/E contraction reduces return by 35.4%. The net result is a 100.7% expected return.

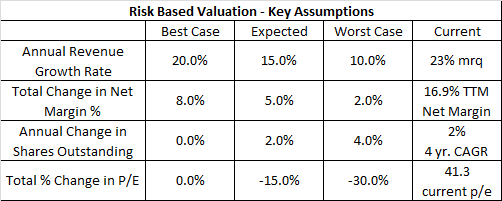

Key assumptions for the risk-based valuation are summarized below:

Best Case Assumptions - Basis

- Revenue: 20% vs. 23% mrq, growth tailwinds in e-commerce, non-cash payments, and mobile

- Margin: +8% over 5 years, margin expansion as fixed costs are spread across more revenues

- Shares Outstanding: 0% growth vs. 2% four year CAGR, cash generation funds growth

- P/E: 0% increase in P/E, P/E remains the same as growth potential stays high

Worst Case Assumptions - Basis

- Revenue: 10% vs. 23% mrq, mobile growth occurs at a lower rate than anticipated

- Margin: +2%, price competition limits margin expansion

- Shares Outstanding: 4% growth vs. 2% four year CAGR, share issuance accelerates

- P/E: 30% decrease, P/E contracts as growth potential declines - harder to grow off of a high base

Expected Case Assumptions are all set at the average of the best and worst case assumptions

Risks to the Investment Thesis

#1: Regulatory action to lower credit / debit card fees.

In July, Wirecard fell by as much as 7.9% when the European Commission considered plans to cap fees on all consumer debit- and credit-card transactions: "Shares of Aschheim, Germany-based Wirecard are trading at a high multiple, since a lot of growth expectations are priced into it," Knut Woller, a Unterschleissheim, Germany-based analyst at Baader Bank AG, said by phone. "Therefore, any question mark behind the growth potential has a negative impact." Even so, the drop isn't justified as "the net effect of the cap on the transfer interchange fee on earnings is nil," as Wirecard collects transaction fees and mostly redirects them to the card issuers, such as Visa (V), Woller said.

#2: Pricing pressure.

Heavy competition could force Wirecard to accept lower pricing in order to win deals. This effect could potentially overwhelm the margin expansion that Wirecard sees from increasing revenue.

#3: New Technologies / Standards.

A new technology or technology standard could emerge for mobile payments. Wirecard could fail to adapt to this technology which would severely limit their growth in the mobile payment market.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire