In October 2010 Elon Musk inaugurated Tesla's newly acquired automotive manufacturing plant in Fremont California. By then, nobody thought we would have to wait so little to begin envisioning a full capacity utilization of the factory. Production of half a million electric vehicles a year by a single company seemed then and seems even today to many car manufacturers nothing more than an elusive dream. But there are reasons to believe that Tesla´s CEO might be able to surprise us again. Let´s now try to figure out how all this story comes about.

In an exclusive interview with plugincars.com on November 1, 2011, Musk already anticipated that Tesla´s ultimate goal of producing half a million cars a year will take six years, "seven at the very latest" because, he said, Tesla plans "to use the whole factory."

What happened next is a series of events that appear to have paved the way for what can be considered as one of the most successful business tales of recent times.

First, on June 22, 2012, Tesla delivered the world´s first premium electric sedan to customers about one month earlier than previously announced.

Second, by December 31, 2012, it had already sold 2,400 model S cars in the U.S. market which was approximately 50% below its original target but still regarded as a real accomplishment.

Third, on May 15, 2013 it launched offerings of 2,703,027 shares of common stock and $450 million aggregate principal amount of convertible senior notes due 2018 in concurrent underwritten registered public offerings.

Fourth, on May 22, 2013 Tesla repaid the entire loan obtained from the Department of Energy in 2010 more than nine years in advance "using a portion of the approximately $1 billion in funds raised" in the offerings of common stock and convertible senior notes taken place a week earlier.

Fifth, on October 30, 2013, Tesla reached an agreement with Panasonic to update and expand their 2011 arrangement for supply of nearly 2 billion Li-ion battery cells over the course of four years to be used to power both the Model S and Model X, "a performance utility vehicle that is scheduled to go into production by the end of 2014."

Sixth, less than a week later, on November 05, 2013, Elon Musk was on the news again to say that he was considering building a giga-scale Li-ion battery plant, which would be "something comparable to all lithium ion production in the world, in one factory." According to him, "if we were to produce 500,000 [cars], we need cell capacity commensurate with that" and "that might be more, or at least on par with, all lithium ion production in the world today."

Seventh, by November 30, 2013, Tesla had sold 17,700 Model S cars, almost 89% of its original target, taking into account only the first 11 months of the year (See hybridcars.com's January - November 2013 Dashboard).

Eighth, in an interview with AutoBild that took place earlier this month, Franz Von Holzhausen, Tesla's Design Chief also anticipated that the motor company "might actually unveil the Model E at the Detroit Auto Show in 2015," albeit this information was later on qualified by Tesla on the account that an unveiling was not confirmed at the Detroit Show and that the timeline for customer delivery of the car had not changed. Notice, however, that on October 23, 2013, while talking to a crowd of prospective customers in Germany, Tesla's CEO had already anticipated that by the first quarter of 2015 they would reveal a prototype of the third-generation car, also known as Model E, which is consistent with his previous timeline for customer delivery of the cheaper Tesla starting by 2017 at the latest.

And ninth, on December 16, 2013 Tesla launched its website in China announcing that it will start delivering Model Ses in the first quarter of 2014.

Given this extraordinary record in fulfillment of previous promises for such a remarkable electric vehicle start-up, in what follows I will attempt to go deep into the reasons why a number of car makers might be afraid of Tesla.

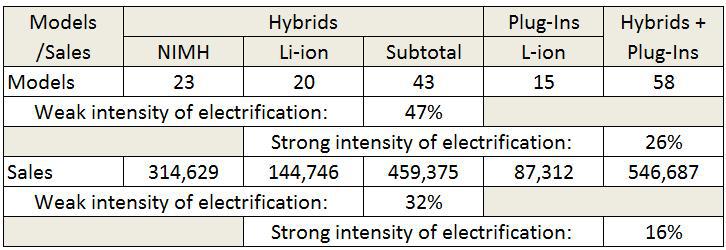

To begin with, there is no single major automaker without some degree of electrification nowadays, although as of November 30, 2013 sales of both hybrid electric vehicles (HEVs) and plug-in electric vehicles (PEVs) accounted for only 3.62% of all cars sold in the U.S. market. I would call this "relative electrification" in the automotive industry.

In recent times "going electric" has turned out to be a major source of reputation and prestige among car makers. As it is well known, HEVs use both Nickel Metal Hydride (NiMH) and Lithium-ion (Li-ion) batteries; by contrast, PEVs utilize Li-ion batteries only. We could therefore think of two measures (one weak and another strong) of the "intensity of electrification." The weak one would be stated in terms of the percentage of hybrid models and sales using Li-ion batteries of all hybrids, whereas the strong one could be established in terms of the percentage of plug-ins models and sales of all EVs. As shown in Table 1, between January and November 2013, the weak measure of the intensity of electrification was between 32% (for sales) and 47% (for models), while the strong measure of the intensity of electrification was in the range of 16% (sales) and 26% (models).

Table 1

United States: Measures of the intensity of electrification in the automotive industry

(January-November, 2013)

(click to enlarge)

Sources: hybridcars.com and rmi.org.

The previous analysis can be extended to the firm-level where in a nutshell a car maker would be relatively electrified as measured by the percentage of its hybrid and plug-in models and sales and intensely electrified the more plug-in vehicles it produces and sells in a given geographical location and in a determined period of time. It then follows that since plug-in vehicles - that happen to be the most advanced electric vehicles - use lithium, the more lithium car makers utilize, the more intensely electrified they are. Hence lithium appears to have in fact become a key factor in the transition to electric propulsion in the U.S. automotive industry today. This seems quite astonishing considering that only about three and half years ago not too many agreed that Li-ion batteries could be used for conventional hybrids and just three years ago the first plug-in electric vehicles (i.e. GM's Volt and Nissan's Leaf) were launched to the U.S. market, not without confusion over what they really meant. In this context, Tesla Motors' attainment of the highest possible mark (100%) in both relative electrification and strong intensity of electrification represents a major achievement. But what else does this mean?

It means not only that Tesla Motors is the greenest car company in the U.S. market which has given it a sense of prestige and status but also the most innovative one because going electric has signified for Tesla to have to innovate a great deal. As I have long argued, the market either rewards or penalizes companies depending on how innovative they are. In addition, green innovations may have led investors to increase their bets on the motor firm. Taken together, all of this explains why Tesla has consistently beaten all major car makers in the stock exchange market during 2013. This can be clearly seen in Figure 1.

Figure 1

Tesla Motors versus All Major Car Makers in the U.S. Market

January-November, 2013

(click to enlarge)

Source: Nasdaq.

In addition, as of now, Tesla is beginning to make a difference both in the lithium and the Li-ion battery markets. During the period of analysis, it would have consumed 2,090 metric tons of lithium carbonate equivalent (LCE) which amounts to 72% of all the lithium required for the production of Li-ion batteries used by all the plug-in vehicles commercialized in the U.S. and 68% of all the lithium required by all the hybrids and plug-ins sold in the same market (See Tables 2 and 3). Assuming a lithium global demand of 168,000 tons for 2013 (See roskill, 2013), Tesla's lithium consumption corresponded to 1.24% of the world's lithium consumption.

Table 2

Lithium Requirement for Li-ion Batteries and Li-ion Energy Storage Capacity

Plug-Ins

(January-November, 2013)

(click to enlarge)

Sources: hybridcars.com and rmi.org.

Similarly, within the same time period, Tesla demanded 1,504.5 MWh of energy storage capacity which amounted to 58% of the energy storage capacity demanded by all plug-in vehicles and 54% of the energy storage capacity required by all hybrids and plug-ins in the U.S. market (See Tables 2 and 3). Assuming a world automotive energy storage capacity of 1,787.5 MWh (See navigant research, 2012), Tesla's demand constituted about 84% of the world energy storage capacity required by the global automotive industry.

Table 3

Lithium Requirement for Li-ion Batteries and Li-ion Energy Storage Capacity

Plug-Ins + Hybrids

(January-November, 2013)

(click to enlarge)

Sources: hybridcars.com and rmi.org.

It is indeed amazing how much Tesla has been able to accomplish with a production of only 17,700 EVs during the first 11 months of the year. Here the two recent announcements regarding Li-ion batteries made by Tesla acquire some perspective. For one thing, the two billion 18650 Li-ion cells ordered to Panasonic to be delivered over the course of the four following years would imply the production of about 285.714 model S cars, which results from dividing 2 billion Li-ion cells by 7,000, the number of cells required by a typical Model S. For another, Tesla's decision to build a giga-scale Li-ion battery factory, which would be "something comparable to all lithium ion production in the world" would entail manufacturing almost 800,000 Li-ion batteries, which results from dividing the world energy storage capacity (23,788 MWh) as estimated by Navigant Research by the energy storage required by all plug-ins sold in 2013 (2,601 MWh) and multiplying by the total number of plug-ins sold in 2013 (87,312) in the U.S. market.

In Table 4 I present a preliminary estimation of Tesla's demand for Li-ion battery and how it could be met over the following 7 years, under the following assumptions:

Model S:

1) Demand continues to grow in 2014 at an annual rate of 50%.

2) In 2015, this rate diminishes somewhat (to about 32%) so as to insure that production of Model S in 2013 is doubled.

3) From then on, demand grows at increasing rates starting from 10% in 2016 and ending at 30% in 2020.

Model X:

1) Demand is almost negligible and symbolic in 2014, the year of the launch of this car.

2) In 2015 the model reaches the level attained by Model S in 2013.

3) In 2016 the demand is doubles that of 2015

4) From then on, demand grows at increasing rates starting from 10% in 2017 and ending at 25% in 2020.

Model E:

1) Demand is symbolic in 2016 following the launch of the model in the second half of the year.

2) In 2017 the demand is quadrupled considering that Model E will be an EV for the masses, much cheaper than the other two models.

3) From then on, demand is doubled each year until 2020.

Under these circumstances, it is clear that beginning 2020 Tesla could fulfill its promise of producing 500,000 electric vehicles at near to full capacity of its plant in Fremont, California.

Notice also in Table 4 that the Panasonic contract will only cover the demand for Models S and X from 2014 to 2017, whereas the Giga factory would have to take care of the demand for Model E in its entirety (2016-2020) as well the demand for Model S and X beginning 2018.

As limited as it might be, the present analysis not only demonstrates the plausibility of Musk´s strategy, but also how dangerous Tesla could become to competition in the following 7 years or so, which explains once again why many car makers could be afraid of this revolutionary EV company.

Table 4

Tesla´s Estimated Demand for Li-ion Batteries

(2014 - 2020)

(click to enlarge)

Source: My own calculations.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire