In the book, If You Must Speculate, Learn the Rules , Frank J. Williams wrote:

The market is most dangerous when it looks best; it is most inviting when it looks worst.

We all know the roller coaster ride for REITs in 2013. At the beginning of the year, REIT stocks began to soar as investors were hungry for durable sources of income and then on May 22nd the momentum faded as the Federal Reserve released minutes from its policy meeting. That news brought shockwaves to REIT-dom as the Fed suggested it was going to curb its bond-buying activities later in the year.

Now with just a few days remaining in the year, the Fed recently announced it would begin the initial taper to its bond buying program. Of course, the biggest news is that the Fed said it would continue to keep interest rates low throughout 2014. Conclusively, the Fed made it clear that 'Taper' and 'Rising Rates' are not synonymous and that should smooth short-term concerns for many REIT investors.

As some of you know, I launched a REIT newsletter business back in May, just a few days before May 22nd. Although I have been overwhelmed with positive feedback, I must admit that the last few months have been bitter sweet. Many investors, including myself, bought REIT positions the last half of 2013 and the agony of getting in too early was somewhat muted by the thrill of buying into an increased "margin of safety."

As we all have watched REIT nest eggs decline in value - except for a few outliers like Gramercy Property (GPT) - the true test for value investors has been to stay focused and try not to predict short-term stock market movements. In doing so, I have been more focused on asset allocation and trying to ride out the bumps brought on by speculative interest rate forecasting.

As a long-term investor, I have attempted to invest in targeted REIT stocks that demonstrate both a quantifiable "margin of safety" and a sustainable earnings history. Accordingly, I look for consistent profit margins - DIVIDENDS - that have been paid over long periods of time and before I hit the BUY button I always ask myself "is this REIT risky because of its price or because of the business model - or both?"

As I review my 2013 "score card," it's not hard to spot my biggest loser. In fact, when I review my list of REIT holdings (acquired in 2013) the biggest loser - Digital Realty (DLR) - sticks out like a sore thumb. So why not unload it you may ask? Fellow Seeking Alpha columnist Morgan Myrmo believes you should; as he explained in a recent article:

DLR may be a short-term trade opportunity but also appears to be a dangerous investment at this time.

Nibbling and Monitoring Closely

As any value investor knows, risk is more often the price you pay than the stock itself. As I have researched Digital Realty over the course of a few months, I have not seen anything "dangerous" other than the price. In an article I wrote earlier this week, fellow Seeking Alpha contributor Chuck Carnevale explained:

As a buy and hold investor, I rarely recommend selling unless overvaluation is extreme.

In order to gain a full perspective for my reasoning to hold shares in Digital Realty, I must first provide a historical time line of my articles and other relevant news items.

February 11, 2013 - My first article on Digital Realty. I recommended a BUY price of $65.40.

May 13, 2013 - I wrote about Highfields Capital short (18 million shares) on May 8, 2013

May 22, 2013 - The Fed mentioned tapering

June 7, 2013 - I wrote an article recommending shares at $61.79

July 26, 2013 - Q2-13 Earnings Release and accounting changes mentioned

September 23, 2013 - I wrote article highlighting hiring of John Stewart as VP of Investor Relations

October 6, 2013 - I wrote an article on DLR and I disclosed ownership at $52.50

October 30, 2013 - Q3-13 Earnings Release and Straight-Line Rent Expense Adjustment related to 111 8th Avenue in New York

November 14, 2013 - I wrote an article and shares closed at $46.38

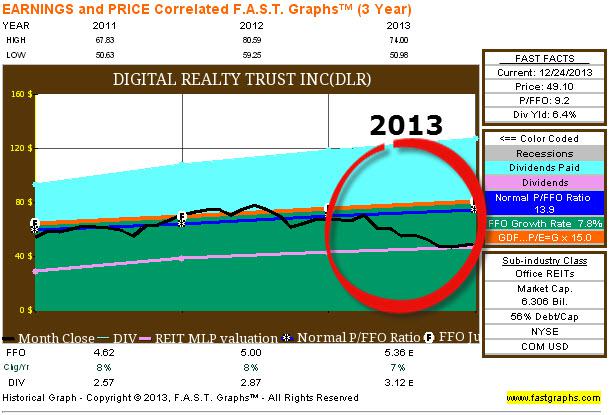

The chart below summarizes most of the drama that occurred over the last year or so. As you can see, the shares fell from $65.40 (when I recommended) in February to a recent close of $49.10, a year-to-date Total Return of -23.5%.

(click to enlarge)

Over the course of the last few weeks, I have been cautiously dollar cost averaging shares of Digital Realty and my weighted average cost to date is around $48.16 or around 2% below the current share price (of $49.10).

(click to enlarge)

I know that I'll hear from a few readers voicing opinions about my BUY recommendation back in February. I can't hide from the fact that I mistimed all of the dramatic events that followed my initial BUY. I will say that I tried to assess the risks associated with Digital in February and in hindsight I don't think anyone could have predicted a short from Highfields or a Fed-induced taper tantrum. Even the two botched earnings calls weren't rehearsed and that leads me to ponder whether or not Digital shares can fall more in 2014.

Yet, I don't see any signs that lead me to believe that Digital Realty is a "dangerous" investment today. Arguably, there is much less risk in the stock price today than there was back in February. I regret the fact that some investors may have followed my advice then and I just hope that they either bailed early or had limited exposure during the 8 month long sell-off. Like me, I know some of you have continued to dollar cost average shares while also paying special attention to the quarterly calls and insider trading activities.

Why Am I Staying In It?

Simply said, "I'm in it to win it" and I'm not selling Digital Realty in 2014. As noted above, I consider Equity REITs today to be trading in fair valuation ranges and I'm hoping to see less drama regarding interest rates and REITs over the next few months. In my opinion, the market has already priced the potential risks - giving investors a better and more attractive playing field. The biggest risk for Digital Realty appears to be the price that an investor is paying, not the business model or the fundamentals. Let's take a closer look…

As a "first mover" and dominant player in the Data Storage Sector, Digital Realty owns 130 properties, including twelve properties held as investments in unconsolidated joint ventures, comprising approximately 24.0 million square feet, including 2.8 million square feet of space held for development. Digital's portfolio is located in 33 markets throughout North America, Europe, Asia and Australia. Here is a snapshot of the company's unmatched portfolio of Interconnected US Data Centers:

(click to enlarge)

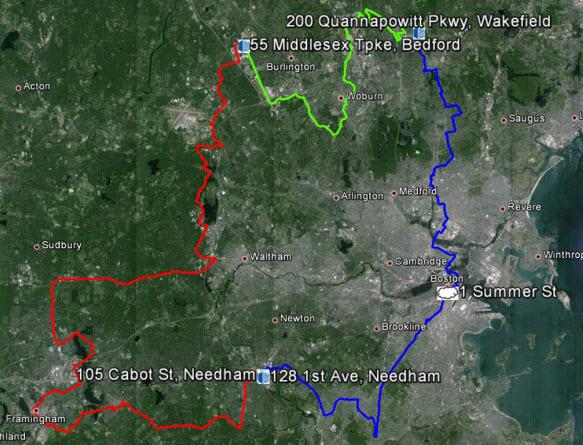

By locating in many "gateway" markets across the US (and abroad) Digital has built a strong competitive advantage around configuring dark fiber strands that form highly secure internet connectivity. For example, in Boston, Digital has built a circle around key towns like Wakefield, Bedford, and Needham.

(click to enlarge)

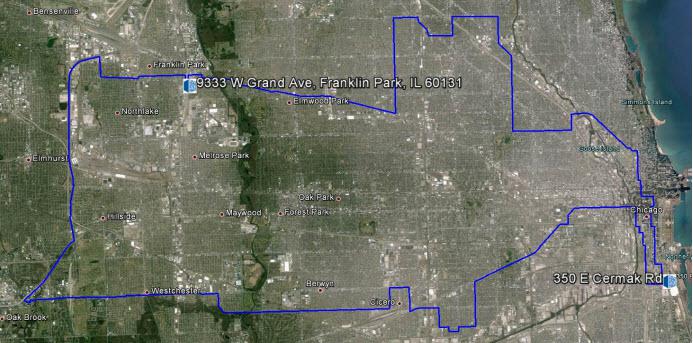

Likewise in Chicago, Digital has built an all-encompassing fiber strand network that connects to strategic data centers in and around the Windy City.

(click to enlarge)

Digital has also expanded its global portfolio in Europe and Asia Pacific and the overall portfolio should surpass $10 billion in 2014.

(click to enlarge)

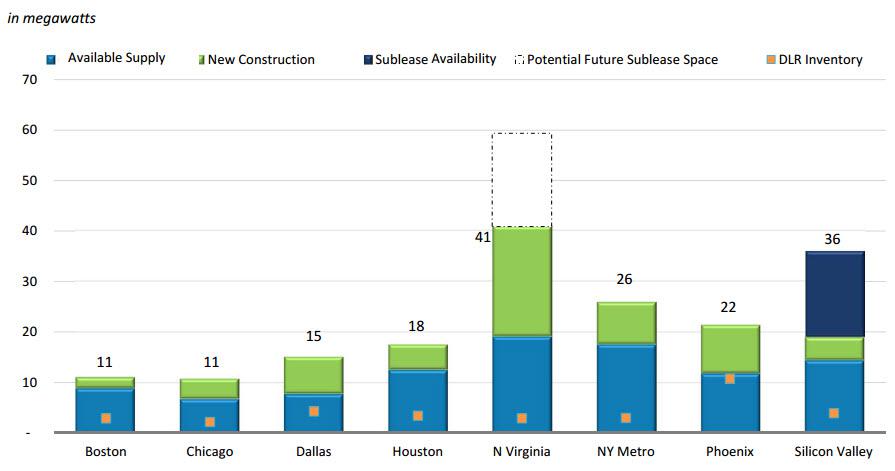

One of the key issues related to the Data Sector REITs today is supply and demand. Simply put, will there be growth (demand) in the Internet, cloud computing, and corporate outsourcing? The biggest pressure facing the data sector today is whether or not supply will outpace the demand growth. Before, investors were giving the Data REITs the benefit of the doubt and pricing in a lot of growth upfront; however, the more recent trend has been in less trust and more to verify. As illustrated in a chart (below), Data Center supply is generally in check across most major markets.

(click to enlarge)

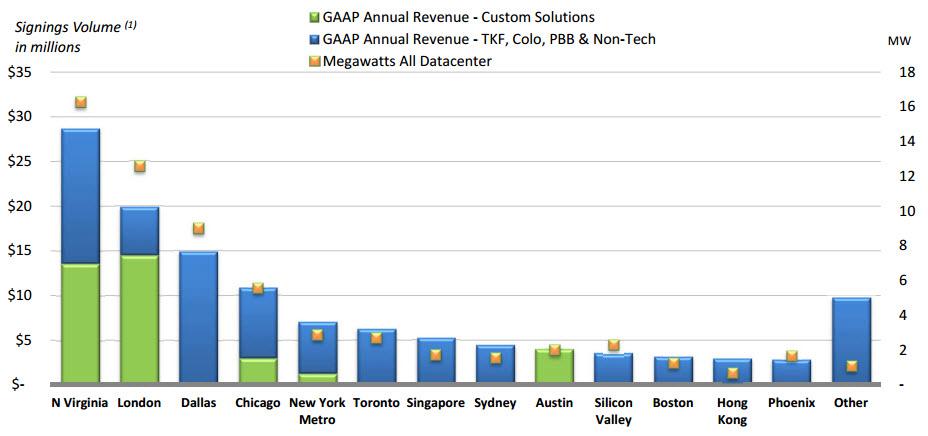

As a leader in data storage, the chart below illustrates the strong customer demand driving Digital Realty's development activity. Note: Northern Virginia, London, and Dallas led the growth in lease signings in 2013.

(click to enlarge)

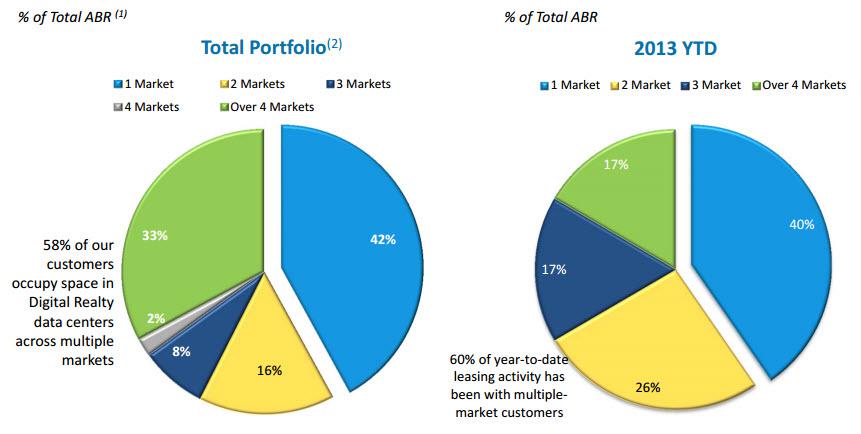

Over half of Digital's customers take space in more than one market:

(click to enlarge)

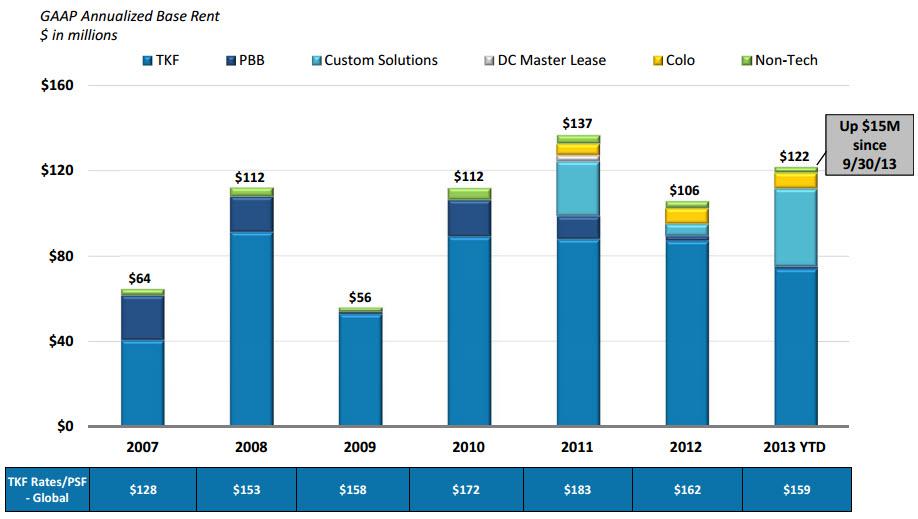

Also, as evidence of growth, Digital has already surpassed the lease activity that company generated in 2012 - up $15 million (since September 30, 2013).

(click to enlarge)

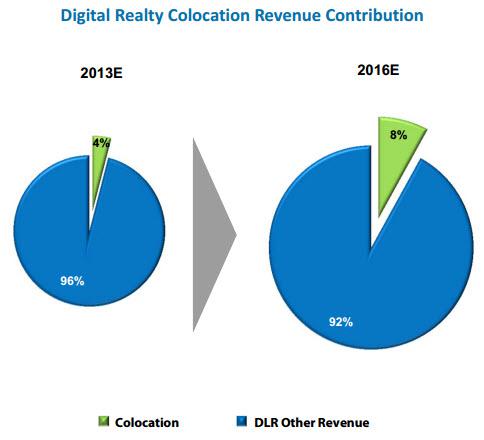

As part of Digital's growing business model, earnings (or Funds from Operations) could see incremental growth of around $0.30 per share (in FFO) as a result of the recognized collocation revenue. Here is a snapshot that illustrates the potential of the increased demand (in collocation):

(click to enlarge)

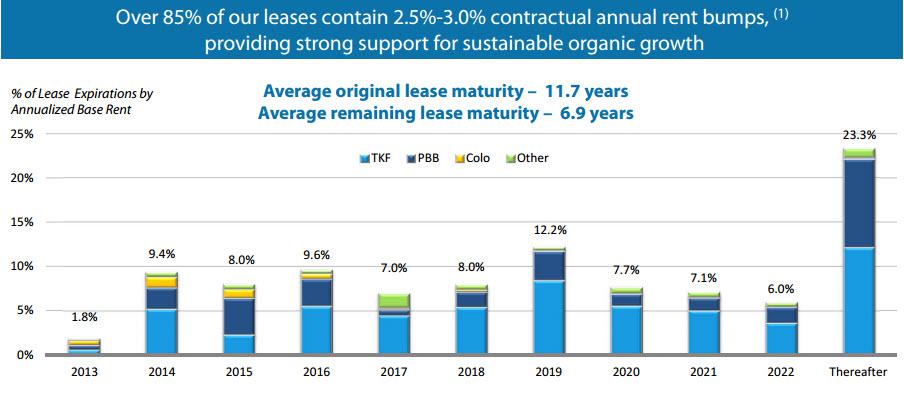

Digital has a well-balanced portfolio of tenants and over 85% of the leases contain 2.5% to 3% contractual annual rent bumps, providing strong support for sustainable organic growth.

(click to enlarge)

The average original lease maturity is 11.7 years and the average remaining lease maturity is 6.9 years.

(click to enlarge)

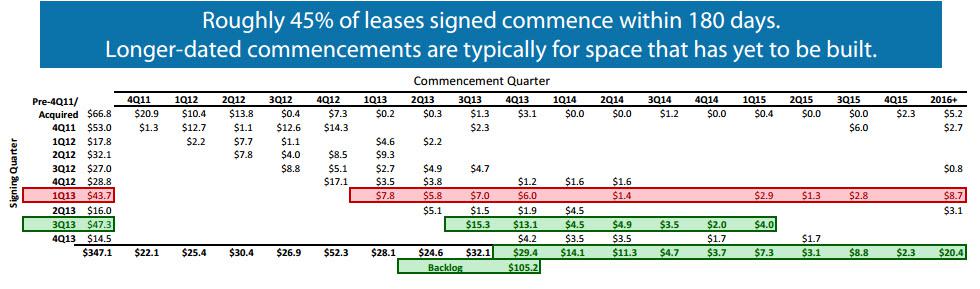

Digital has recently introduced its "Backlog Waterfall" spreadsheet. As the chart below illustrates, roughly 45% of leases signed commenced within 180 days. This (new) chart provides more transparency as it relates to lease signings and when rents are recognized. As you can see, in Q1-13, Digital had a longer backlog of revenue and in the third quarter, the company has tightened up the commencements considerably.

(click to enlarge)

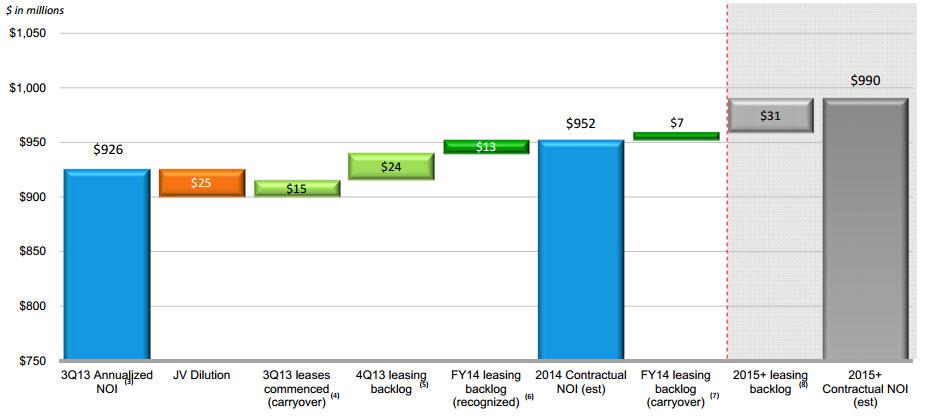

During 2015 Digital's Net Operating Income should approach $1 billion.

(click to enlarge)

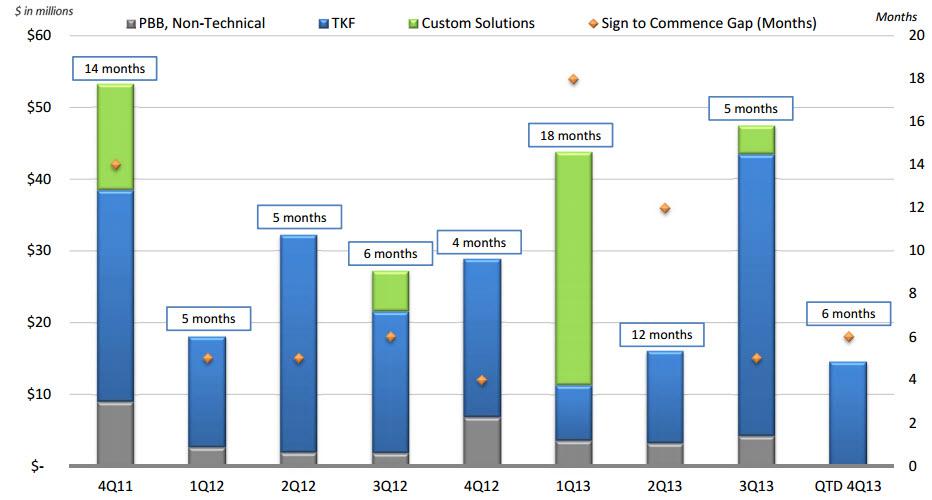

Historically, Digital has been a large developer of build-to-suit projects. In fact, having the ability to source ground up customized deals has been a big differentiator for Digital's growth model. However, in Q4-11 and Q1-13 several larger projects contributed to the lag between signings and commencements. Due to the customization of the larger projects, these delays appeared to be isolated and the other projects produced more predictable commencements.

(click to enlarge)

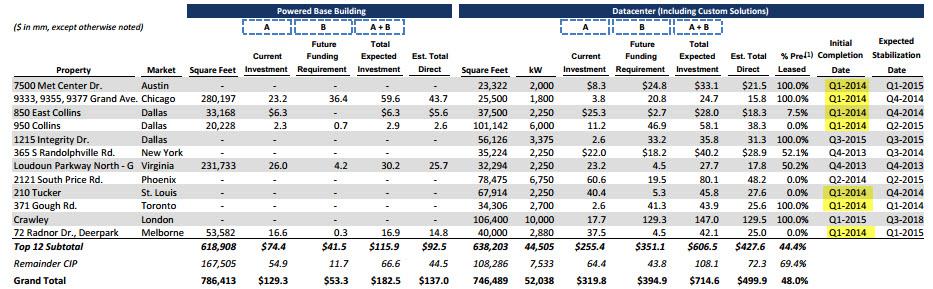

In order to better educate (and provide greater transparency) on Digital's development deals, the company has recently introduced a construction in progress exhibit (see below). This provides greater transparency of deal flow in an effort to educate investors on deal flow and the risk and reward elements associated with development projects. Here are the top 12 largest development projects:

(click to enlarge)

To fund the pipeline of growth, Digital expects it will have between $1.3 billion and $830 million in liquidity and the company stated that it "would need no common equity (raised) and it doesn't intend to (in 2014)."

Have the Fundamentals Changed Since January 2013?

The shorter answer is NO. Digital maintains a fortress balance sheet and as illustrated below the company has a healthy Net Debt/ LQA Adjusted EBITDA multiple:

In addition, Digital maintains sound interest coverage of 4.6x.

Also, Fixed Charge Coverage appears to be in line with other investment grade rated peers.

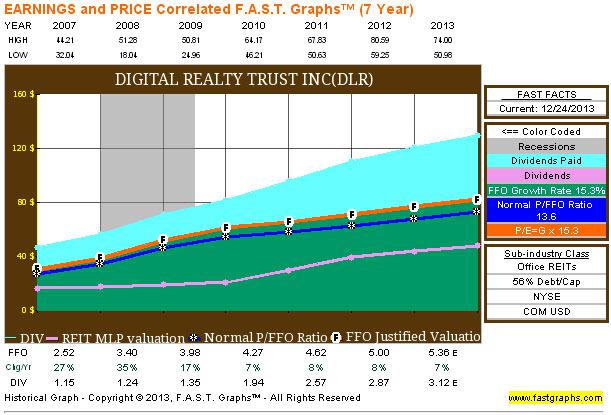

Ben Graham once remarked that earnings are the principal factor driving stock prices. To get a picture of Digital's earnings history, let's take a look at the FAST Graph (below) with no price line. In other words, this chart provides us with a clear picture of Digital's dividend history and share price history (combined being the total return).

(click to enlarge)

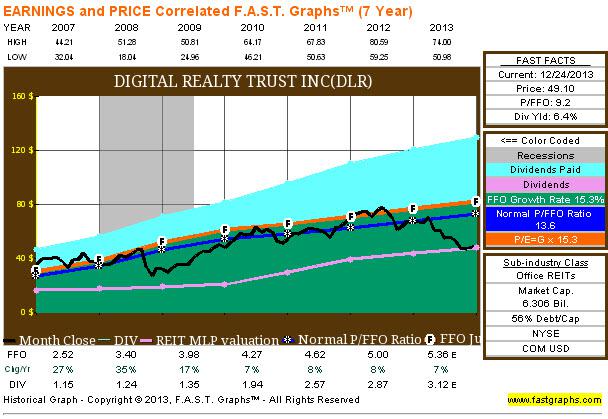

Nothing wrong with that picture. I see no danger whatsoever. So let's add back in the price line (black line) and see how Mr. Market is feeling…

(click to enlarge)

Wow! Mr. Market has fallen out of favor with Digital and 2013 has been a bitter pill for investors to swallow.

(click to enlarge)

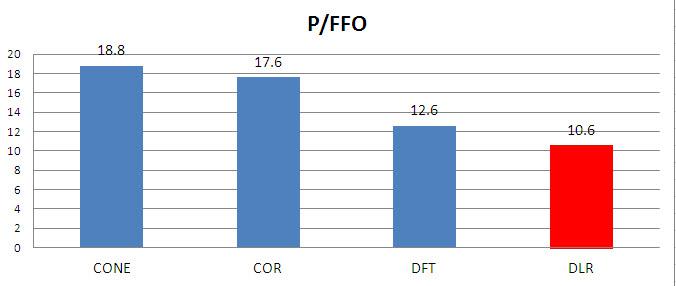

Will 2014 be any better? Let's examine the Price to Funds from Operations (P/FFO) multiple for Digital and the peer group. As you can see below, Digital is trading at 10.6x, well below the average peer multiple of 16.3x.

(click to enlarge)

In a broader peer group, Digital is still trading at a substantial discount when comparing 2014 estimated Price to Adjusted Funds from Operations (P/AFFO) multiples:

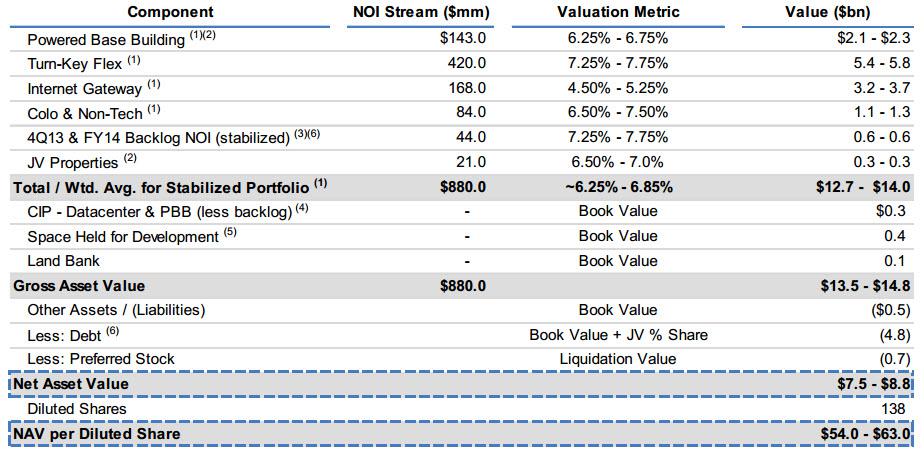

Considering Digital's Net Asset Value (NAV) metrics, the company is trading around 20% below mid-line estimates. Using conservative valuation methods, Digital's intrinsic value is at $60 (midpoint) at the stock is trading at $49.10 today.

(click to enlarge)

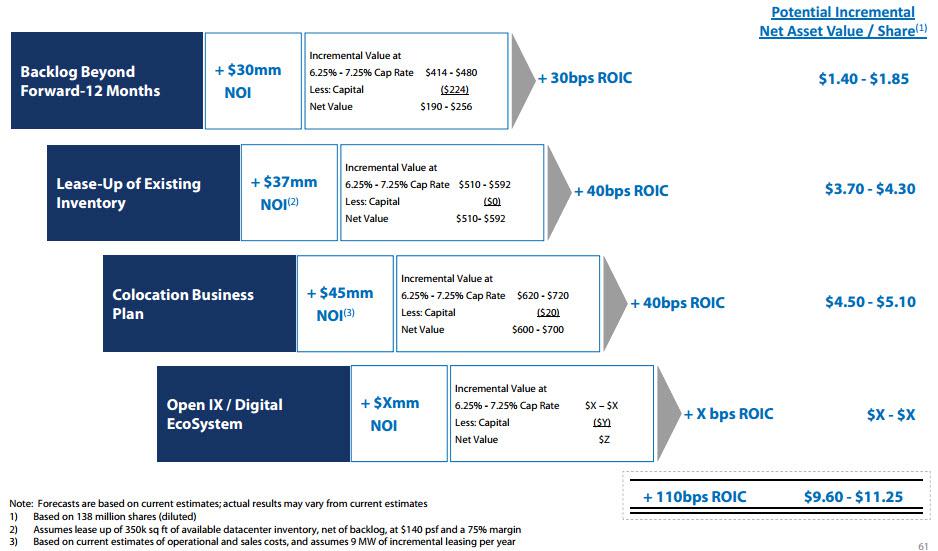

Also, when considering the potential upside embedded within Digital's portfolio there is significant potential incremental value - possibly as much as $10.00 more per share.

(click to enlarge)

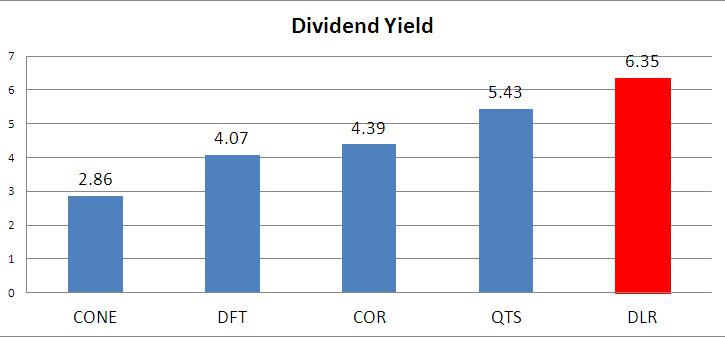

Of course, for most investors, Digital represents a very attractive dividend yield. The company is now trading at a substantial discount and that is reflected in the above average yield of 6.35% - well above the more expensive peers.

(click to enlarge)

Driving the earnings train for Digital is the highly coveted Funds from Operations per share. As evidenced below, Digital has continued to maintain an attractive earnings history with NO CHANGE IN FUNDAMENTALS.

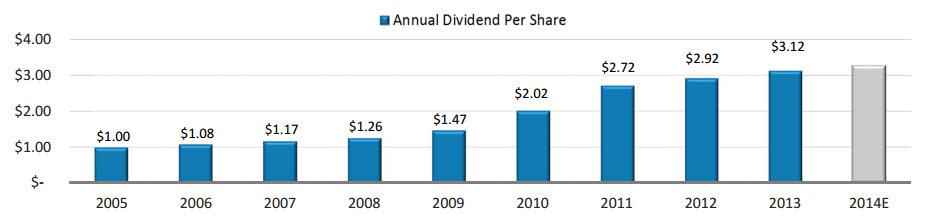

Digital has committed to provide shareholders with a secure and growing dividend stream and the company expects to increase the dividend between 5% to 6% in 2014 (source: Investor Presentation). The AFFO payout as of Q3-13 was 84.7% and the company targets the AFFO payout ratio of <90%.

(click to enlarge)

Now I Will Consider the Logic

Over the course of 2013, I have spent a considerable amount of time in an effort to educate myself and my readers on data center applications. Some of the obvious and easy ways to research the sector is by viewing YouTube videos like this ONE or this ONE. There are also a number of other articles on Digital Realty and the peer group all over the internet (including Seeking Alpha).

But wait. Where are all of these articles and videos stored? To me, that is the key question for Digital Realty. This cloud landlord is very closely aligned to the rapidly changing internet and the biggest question is whether the demand for data storage will increase or decrease. And if the demand does increase over the next 3, 5, or 10 years, will the demand for servers become larger or smaller?

Let's be honest. Digital has been a volatile stock and I think anyone would agree that my use of the word "sleep well at night" isn't appropriate. The risk/reward profile for this REIT is much higher and of course that leads me to the opportunity, that is, the chance to own a high quality REIT at a discount. I'm not selling. As inspired by Ben Graham (and others) I must buy stocks when they are cheap as that is the best way to grow my net worth - stocks of good companies on sale reap the highest returns.

Senior management and directors are usually the first to know when the operations are improving and if they buy the shares on the open market it's a good sign that things are getting better. Moreover, consistent purchases by insiders are even a better indicator that the train is back on track.

(click to enlarge)

So in summary, I don't see the danger in keeping my shares in Digital Realty. I'm not concerned if there is added volatility as I would respond by further dollar cost averaging. At some point, I must limit my exposure to the stock as well as the Data Sector. We all know that 2013 was not a great year for Digital Realty; however, I liken the current opportunity to my long-term perspective and a thought provoking quote from Christopher H. Browne in The Little Book of Value Investing :

Long-term, value investing is like flying from New York to Los Angeles. While you may encounter some air turbulence over Kansas, if your plane is in good shape, there's no reason to bail out. You will eventually reach your destination safely.

(click to enlarge)

Check out my monthly newsletter (The Intelligent REIT Investor ).

Source: SNL Financial, Yahoo Finance, FAST Graphs, and DLR Investor Presentation.

Other REITs mentioned: (COR), (DFT), (CONE), and (QTS).

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long O, ARCP, VTR, HTA, HCN, UMH, DLR, ROIC, STAG, CBL, GPT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire