Walter Energy (WLT) is the leading met coal producer in the U.S. and produces premium quality met coal. As WLT is mainly engaged in met coal operations, its earnings are highly sensitive to met coal prices. Met coal prices in recent times have stayed weak, and I believe oversupplied met coal markets will limit a met coal price recovery in the near term. Last week, the met coal quarterly benchmark price for 1Q2014 settled at $143/ton, its lowest level since 2009. As met coal markets remain oversupplied, I am downgrading WLT from 'buy' to 'hold'. Also, WLT has experienced price appreciation of approximately 50% in the ongoing second half of 2013, which limits any stock price appreciation in the near term.

Lower Met Coal Price and oversupplied Markets

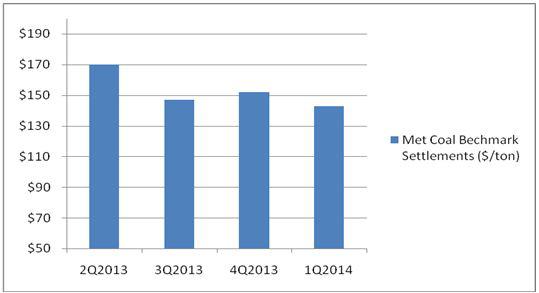

Last week, the 1Q2014 met coal benchmark price settled at $143/ton, down from $152/ton for 4Q2013. The 1Q2014 benchmark price remains the lowest since fiscal year 2009's annual settlement price of $129/ton, indicating that met coal markets remain oversupplied. Also, due to excess supply, the met coal spot price continues to drop; last week, the met coal spot price was down $1 to $137/ton. I believe that oversupplied met coal markets will limit any met coal price recovery in the near term. The following chart shows the recent met coal benchmark price trend.

(click to enlarge)

To address the concerns of oversupplied met coal markets, coal producers need to cut supply, delay the completions of new coal mines and coal demand needs to strengthen; however, supply cuts remain the most important driver for a recovery in coal markets. Having said that, supply cuts do not appear to be forthcoming in the U.S. in the near term, and it is expected that at minimum, met coal production in 2014 will at least equal the 2013 production levels. WLT, Alpha Natural Resources (ANR) and Teck Resources Limited (TCK) are likely to maintain their 2013 met coal production levels in 2014, whereas Arch Coal's (ACI) met coal production in expected to increase in 2014 year-on-year, as it is planning to ramp up its production at the new Leer mine in 2014. Therefore, I believe met coal markets will remain oversupplied in the near term, which will limit a met coal price recovery.

Financial Flexibility

WLT's mine 4 and mine 7 are cash positive in the current depressed coal market conditions, as these mines have cash costs of approximately $115/ton and $105/ton, respectively. Also, both these mines in Alabama have lower transportation costs, as they are closer to ports. WLT's has Canadian mines, which are unprofitable in the current tough market conditions, and has a highly debt-loaded balance sheet; WLT currently has a debt-to-equity of 335%. Despite the fact that WLT has reduced its operational costs in recent times, share price performance remains dependent on met coal pricing and capital structure headwinds. I believe that in order to strengthen its balance sheet and improve its financial flexibility, WLT can issue equity, which might portend well for the stock price. Also, any equity issuance would help the company improve its capital structure and navigate through the ongoing industry downturn.

Conclusion

I believe met coal prices are expected to remain weak in the near term, as met coal markets remain oversupplied. Also, supply cuts remain the most important factor for a recovery in met coal prices. Moreover, I believe WLT should consider equity issuance as an option to strengthen its balance sheet and survive the prevalent difficult times. Furthermore, due to depressed coal market conditions, coal stocks continue to trade at depressed valuations, which I believe is justified; WLT is currently trading at a P/S of 0.5x and P/B of 1.1x.

Due to excess met coal supply and weak met coal prices, I am downgrading WLT from 'buy' to 'hold', and recommend investors to keep a check on met coal supply in the market, as it could have a notable impact on the stock price as we move forward.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire