Walgreen Company (WAG) is the largest drug retailer in the United States. The company operates about 8,600 stores (including medical centers, pharmacies etc.) in the US, D.C. as well as Guam and Puerto Rico and has a history of increasing revenues per drug store. In fiscal year 2013 the company achieved revenues of $72.2 billion with net earnings of $2.45 billion. Despite revenue growth and a focus on shareholder remuneration I believe Walgreens is too expensive to warrant an investment.

Historical performance

Walgreen shares have shot up 57% over the last twelve month while CVS Caremark (CVS) gained about 47%.

(click to enlarge)

If we define the peer group wider and include Rite Aid (RAD) and GNC Holdings (GNC) for comparison purposes, the picture looks a bit different. Shareholders who purchased Rite Aid five years ago are now looking at an out-of-this-world-return of 1,424%. GNC returned 246%, CVS 142% and Walgreens125%. Walgreens, in fact, has the worst five-year return of all drug store companies.

(click to enlarge)

Intrinsic value estimate

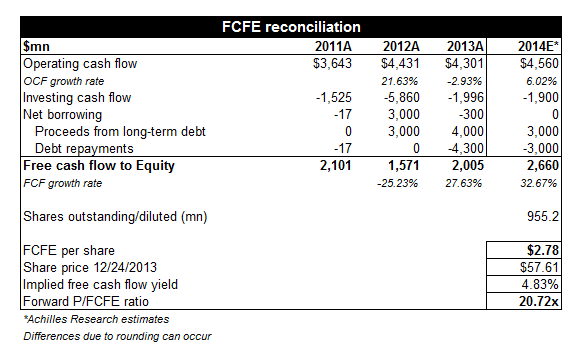

Drug stores produce relatively stable operating cash flows even though free cash flows can be quite volatile depending on the use of cash for investing activities. Walgreens' 2012 investing cash flow, for instance, was heavily skewed by a $4 billion cash outflow for its investment in Alliance Boots.

I have compiled Walgreens' cash flows for the last three full fiscal years from its most recent 10-K filing with the SEC. I estimate that Walgreens can achieve about $4.6 billion in operating cash flow while investing cash flow will mean revert to a normalized level of around $1.9 billion. With a zero net effect of additional borrowings, Walgreens could earn about $2.66 billion in free cash flow to equity or $2.78 in FCFE per share in fiscal year 2014.

As a result, Walgreens would trade at about 21x forward FCFE which clearly is a premium multiple. My FCFE valuation for CVS has revealed a similar picture with a P/FCFE ratio of nearly 18x at the time of valuation.

(click to enlarge)

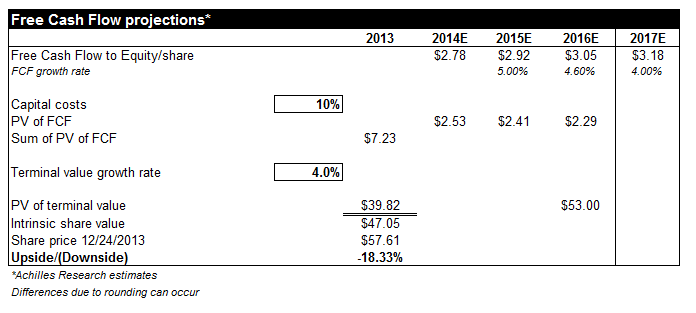

Applying a cash flow discount model (equity cost of capital of 10%, terminal growth rate 4%) yields an intrinsic value per share of $47.05. The high P/FCFE ratio from above already hinted at Walgreens' overvaluation and the discounted cash flow model implies about 18% downside potential for shares of Walgreens given the assumptions depicted below.

(click to enlarge)

Market valuation

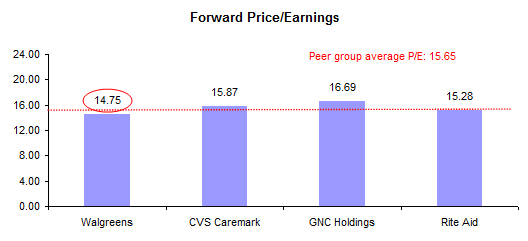

Walgreens and CVS Caremark are the closest competitors in terms of scale of operations, revenues and market capitalizations. Walgreens trades at 14.75 times forward earnings which compares to 15.87x forward earnings for CVS. The other two companies in the peer group achieve fairly similar valuations. Overall, the dispersion of valuations for drug store companies is relatively low.

(click to enlarge)

In terms of dividend yields, Walgreens offers investors the highest yield of all drug stores. With a cash flow yield of 2.19% the company pays noticeably more than its nearest competitor CVS which exhibits a yield of 1.28%. Generally, I would have hoped that drug retailers adopted a more generous dividend policy because of their relatively low-risk cash flow profile. Dividend investors are probably well advised not to purchase either of the drug store companies for its cash flow yield as the majority of gains are likely to come from capital gains.

(click to enlarge)

The comparison table below summarizes all market-related valuation metrics for drug retailers:

(click to enlarge)

Conclusion

The free cash flow model from above, based on my estimates for Walgreens' 2014 operating- and free cash flows, suggests that the drug retailer is overvalued and currently has about 18% downside potential to its intrinsic value of around $47 per share. My related article about CVS Caremark also indicated that drug retailers are likely overvalued since their shares posted healthy gains over the last couple of years.

The market valuation based on earnings also shows that all companies in the sector are valued similarly with a low dispersion of multiples. I think that a multiple of 15 is not cheap and indicates that a company is about fairly valued unless of course the company has outstanding growth perspectives such as Apple (AAPL). A P/E ratio of 15 implies an earnings yield of 6.7% and an investment at this level is not a bargain for value-oriented investors. Given the current valuations in the sector, based on both earnings and free cash flows, I would suggest investors look for better priced opportunities in other sectors of the stock market (e.g. financial- or energy).

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire