ATT: SA EDITORS If possible, please add this article to your SUNDAY, 12/22/13 "Dividends & Income-Dividend Ideas" e-mail alert. Many thanks!

Looking for interesting dividend ideas for 2014? You read the article title right - this week's focus stock has achieved 24 straight quarterly dividend hikes, and also has forecast another hike in the first quarter of 2014.

Like many of the stocks in our recent articles, Spectra Energy Partners LP (SEP) has done a good job of rewarding its unitholders with a steady stream of rising dividends. SEP has grown its quarterly distributions from $.30 in late 2007 up to its recent $.51625 November payment.

In addition, CEO Ebel stated on the company's earnings release, "Spectra Energy Partners is well suited to fund expansion, fuel growth and reward investors with an estimated 9% annual distribution growth rate through 2015, starting with an expected three cents per unit increase in the quarterly distribution paid in the first quarter 2014." (Source: SEP website)

The table above uses the most recent quarterly distribution of $.51625 to calculate SEP's forward dividend yield, but if you add CEO Ebel's $0.03 increase to that figure, it pushes SEP's forward dividend yield up to 5.15%. We've added SEP to the Energy section of our High Dividend Stocks By Sector Tables.

SEP grew its cash available for distribution by 18% in Q3 2013 vs. Q3 2012. Year to date, this figure has grown by 26%. CEO Ebel attributed the increases in both earnings and cash available for distribution to SEP's August 2013 acquisition of 50% of the Express-Platte Pipeline System, and the October 2012 acquisition of a 38.76% interest of Maritimes and Northeast Pipeline.

Options: Although SEP has options, we haven't yet listed them in our Covered Calls Table or our Cash Secured Puts Table as its call and put yields aren't that attractive at present.

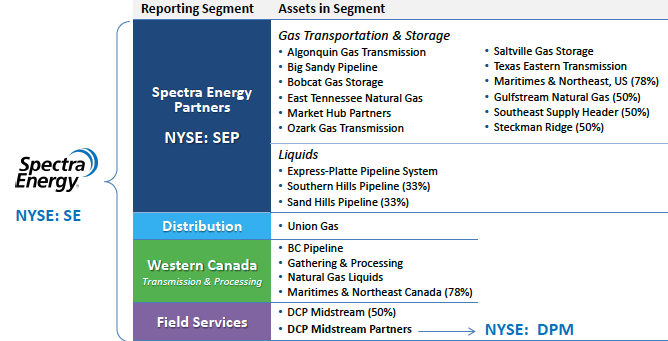

Profile: SEP is a Houston-based, master limited partnership, formed by Spectra Energy Corp (NY: SESE). SEP is one of the largest fee-based MLPs in North America and owns interests in pipelines and storage facilities that connect growing supply areas to high-demand markets for natural gas, natural gas liquids and crude oil. These assets include more than 17,000 miles of transmission and gathering pipelines, approximately 150 billion cubic feet of natural gas storage, and approximately 4.8 million barrels of crude oil storage. SE manages its business in two reportable segments: Gas Transportation and Storage and Liquids.

(click to enlarge)

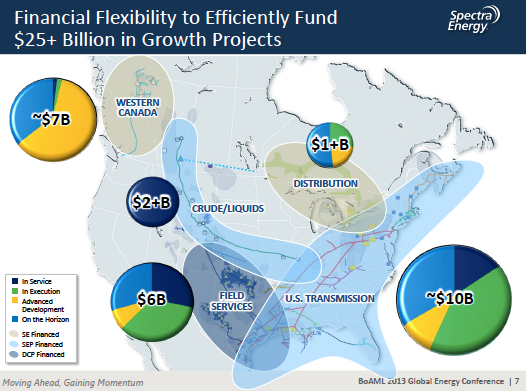

SEP's parent company, Spectra Energy, has over $25 billion in growth projects in various stages. The light blue areas in the map below highlight SEP's regions of operation. Its 2013 50% acquisition of the Express-Platte pipeline system, which transports crude/liquids from Alberta, Canada, to refining markets in the Rockies area, and the Platte pipeline, which interconnects with the Express pipeline in Casper, Wyoming, transports crude oil predominantly from the Bakken shale and western Canada to refineries in the Midwest, and has already been accretive to earnings.

SEP should continue to benefit from asset dropdowns from SE. A recent SEP press release announced that, "On November 1, 2013, Spectra Energy Partners completed the acquisition of Spectra Energy's remaining U.S. transmission, storage and liquids assets. With over 17,000 miles of pipelines, Spectra Energy Partners will be a key participant in the expanding North American natural gas, crude oil and NGL markets, with approximately $8 billion in organic growth opportunities by the end of the decade." (Source: SEP website)

(click to enlarge)

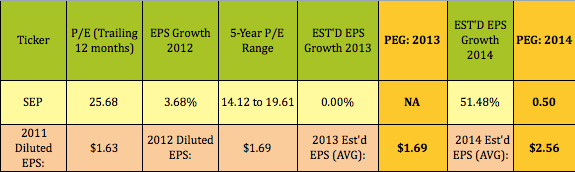

Undervalued Future Earnings: Check out the big difference in SEP's flat 2013 EPS forecast, vs. analysts' average forecast for over 51% growth in 2014. Based on its trailing P/E, this makes look SEP look undervalued on a 2014 PEG basis:

(click to enlarge)

SEP's new 2013 liquids business has made a major impact on its earnings. The Liquids segment's EBIT contributions for the first nine months of 2013 were 17.89%, but grew to over 26% in the third quarter:

Additional Valuations: To be sure, SEP doesn't look undervalued across the board - its trailing P/E and Price/Sales ratios are higher than industry averages. However, its forward P/E is much lower, thanks to the big earnings growth expected in 2014, and it looks cheaper on a Price/Tangible Book basis:

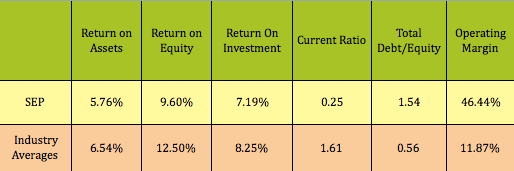

Financials: SEP's ROA and ROI ratios are close to, but below industry averages, but its ROE ratio is lower, and its debt load is higher. However, it has a much higher Operating Margin. ROE should improve in 2014, if it doesn't issue more shares, and if its EPS forecasts come through:

(click to enlarge)

Disclosure: Author had no positions at the time of this writing.

Disclaimer: This article was written for informational purposes only.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in SEP over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire