The week ahead for real estate relative stocks is a busy one. Several important housing sector reports could influence the swing of things. Last week was a relatively good one for stocks generally and especially for homebuilders. This week, the focus shifts to the broader real estate market, and I think there is a greater likelihood for the group to decline than to rise. That's mainly due to the likelihood for continued creep in mortgage rates.

(click to enlarge)

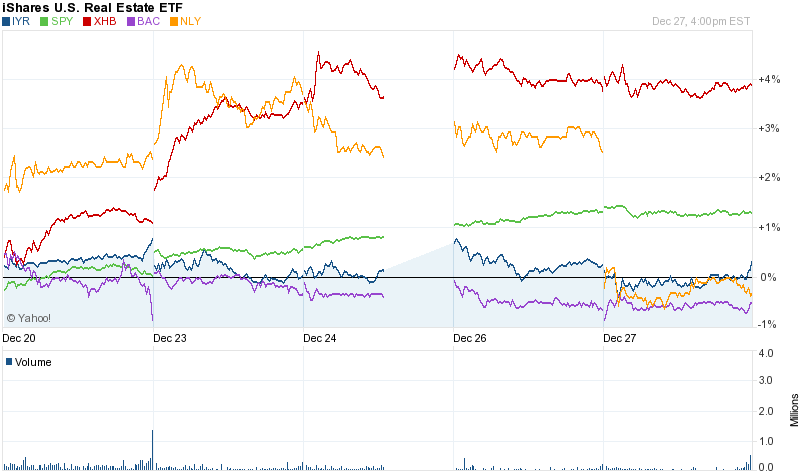

Last Week

Real estate relative stocks had a relatively poor week last week against the performance of the SPDR S&P 500 (SPY), which was up more than a percentage point. As you can see in the chart above, homebuilder shares excelled, evident by the outperformance of the SPDR S&P Homebuilders ETF (XHB). However, housing finance leader Bank of America (BAC), mortgage market player Annaly Capital (NLY) and the broader real estate group, represented here by the iShares US Real Estate (IYR), significantly underperformed.

Last week's catalyst for the strong homebuilder rise was reported new home sales. In November, new home sales ran at an annual pace of 464K, which was above the economists' consensus expectation for 450K. Also notable, September was revised sharply higher to 474K, from 350K. The news led the shares of builders like PulteGroup (PHM) upward 7.8% on the week and the SPDR Homebuilders ETF up by 2.6%.

Still, the broader real estate stock sector languished in subpar performance. The reason for that was more than likely the continued creep in long-term interest rates and mortgage rates. The 30-year treasury yield rose by 12 basis points from December 20th to December 27th. For the reported period ending December 20, 30-year conventional fixed rate mortgage rates rose to 4.64% from the week before, but that was just a 2 basis point increase. Still, the rising trend is not our friend, and mortgage applications declined 6.3% in the period.

Rising mortgage rates and interest rates generally is bad news for Annaly Capital and other mortgage REITS. In our article, The Annaly Capital Paradox , we discussed NLY's rise around the Fed taper announcement, and how measured Fed action kept rates from jumping on the initial release and offered hope for the battered mortgage REITs. However, the creep in long-term rates has continued and pressure upon NLY and fellow mREITs persists. Still, that is not why the stock fell on December 27th; rather it was on the ex-dividend date and its impact on the security value.

Bank of America's share drift better reflects the risk that rising mortgage rates are seemingly posing on the real estate market. BofA is the nation's most important mortgage lender, and despite benefiting from an expending rate spread, if housing activity is burdened by any significant increase in mortgage rates, BofA's business will be affected.

This Week

This week's industry news includes reports of Pending Home Sales, the S&P Case Shiller Home Price Index, Construction Spending and the regular mortgage market data. We'll also receive reports on consumer and investor sentiment, which matter for this market.

Pending Home Sales reports on the existing home market, which is much larger than the hotter new home market. Economists see positive correction in this data point in November, because of October's extraordinary impact from the government shutdown. Thus, economists expect the Pending Home Sales Index might increase by 1.5%, versus the 0.6% decrease in October. Rising home prices and creeping mortgage rates continue to weigh on the existing home market, so a disappointing report is possible here, and it would weigh on all real estate relative securities.

The S&P Case Shiller Home Price Index is scheduled for Tuesday release. The 20-city seasonally adjusted index increased by 1.0% at last report, and is expected to increase by another 1.0% in this one for the month of October. Home prices are up 13.3% year-over-year and are beginning to matter in the housing affordability equation.

The economy matters far more, though, and so keep your eye also on the consumer confidence index, due on the same day. Economists are looking for a sharp spike in this latest checkup, to a mark of 76.8, from 70.4 in November. The Investor Sentiment Index gets a check as well, after having fallen in November to 91.3, from 95.5. The mood of Americans matters here, as it reflects economic direction. It's the reason the Fed taper is not hurting the broader stock market as seen in the stable rise of the SPY. Good news here also helps these real estate relative stocks.

Construction spending is due for report this week on Thursday. Construction spending fervor has dulled as the months have progressed, at least as measured on a year-to-year basis. October's activity was measured up 0.8%, but benefited greatly from public sector spending. Private construction was down 0.5% in October, and down 0.6% for residential construction. Non-residential private construction was also down 0.5% from September. Much of this could have been on concern about the Fed taper and also on rising interest rates, and perhaps also reflects how higher prices are being digested by a less than perfect economic recovery; I'm referring to the less than perfect labor market recovery. Economists are looking for a 1.0% increase in construction spending for November, which might reflect the absence and resolution of the government shutdown issue. If we get there, or near there in my view, real estate relative stocks should rise.

In conclusion, the mixed bag of industry relative economic reports offers significant uncertainty about how the real estate relative stocks might fare this week. However, if the rising rate trend continues, it likely weighs heavier than real estate relative economic data. I expect this reality makes for a greater likelihood for real estate stock decline this week than rise.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire