This article is a follow up to "The Risk Averse BDC Portfolio" from Q3 with updated allocations and investments for a BDC portfolio with an annual dividend yield of 7.5% and relatively safer than most BDC investments. This is for investors who want less volatility and more consistent BDCs with lower than average yields but without the potential for dividend cuts. All of these companies have a history of dividend growth and/or special dividends with a safer portfolio mix. It is for investors who do not want to 'babysit' their investments and are not using them as a major source of income. Many of the lower risk BDCs have higher multiples contributing to lower average yields, but during market corrections, they tend to outperform the others with less volatility and still pay a healthy dividend with long term capital appreciation.

In my article, "A BDC Investment Philosophy And 4 Portfolios," I discussed what BDCs are and why I see them as good investments as well as different approaches to investing, taking into account various investor needs. Out of the 25 BDCs that I follow, I selected the best BDCs for each portfolio type along with recommended weightings. The five different portfolios that I cover are:

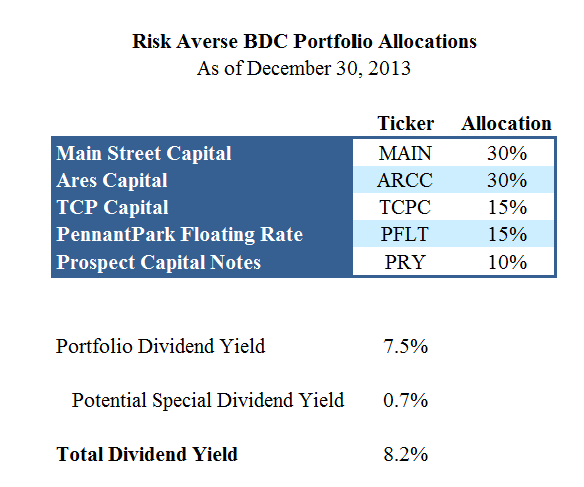

Currently, the five investments for a lower risk BDC mix are Main Street Capital (MAIN), Ares Capital (ARCC), PennantPark Floating Rate Capital (PFLT), Prospect Capital Senior Notes (PRY) and TCP Capital (TCPC). The following allocations are used for the remainder of the information in this article, and all metrics are weighted accordingly.

(click to enlarge)

Other BDCs Considered

While trying to come up with a lower risk BDC mix there were other companies that I considered. Solar Senior Capital (SUNS) is one of the safest BDCs with the exception of its inability to fully cover dividends. Many of the 'safer' BDCs have been falling short of covering distributions due to their continued investments in higher quality loans that are experiencing yield compression from competition. Another factor is the use of leverage and SUNS has very little debt but could potentially grow the portfolio in the coming quarters. Fifth Street Finance (FSC) is another less risky BDC but has also experienced lower yields and uses lower amounts of debt as discussed in "FSC: Time To Buy Or To Sell? Part 1" which is why it recently reduced dividends. Another consideration was Golub Capital BDC (GBDC) but I did not include it for a few reasons, mostly due to pricing and lack of dividend growth since 2010 as well as recently missing its EPS projections and just falling short of covering for reasons discussed in "GBDC: Why It Missed Projected EPS".

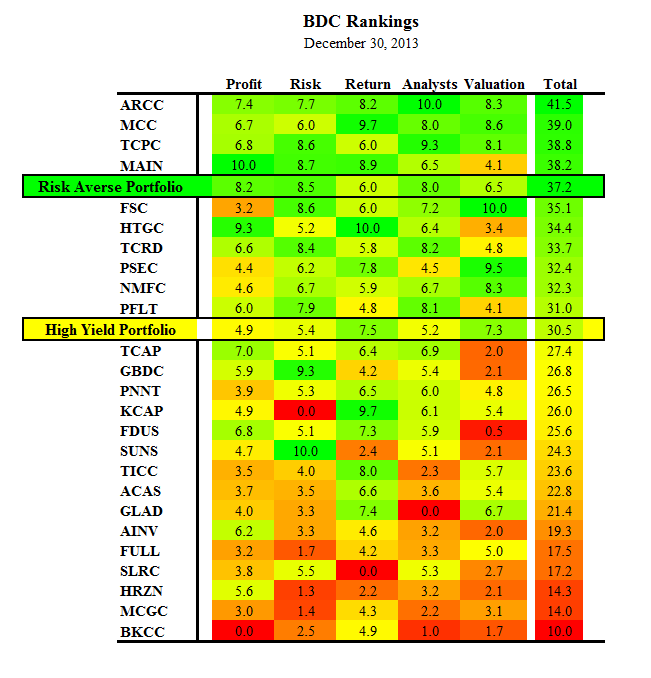

BDC Rankings

These are the five general criteria I use to evaluate BDCs followed by my most recent BDC ranking table. I have included the Risk Averse and High-Yield portfolios as a group in the table indicating how a portfolio with my recommended weighting would compare to the other BDCs.

- Profitability (dividend coverage, fees, NAV and EPS growth)

- Risk (portfolio quality and vintage, rate sensitivity, diversification, volatility)

- Return (sustainable, consistent, growing)

- Analyst Opinions (outlook, price targets)

- Valuation (NAV, P/E, growth rates, total return)

(click to enlarge)

Compared to the recently revised "High-Yield Portfolio" this portfolio has lower return but with better than average risk relative to other BDC investments.

Prospect Capital Senior Notes Due 2022

On May 1, 2012, Prospect Capital (PSEC) issued $100 million in senior unsecured notes due 2022 with an annual interest rate of 6.95% paid quarterly. These notes trade under the symbol "PRY" with a current yield of 6.7% and are an unsecured obligation with a Kroll rating of BBB+ and an earliest call date of May 15, 2015.

Recently these notes have been trading in a price range between $25.00 and $26.50 but currently at $25.80 with an effective yield of 6.7%. As far as I know there have been no defaults by a BDC on these sorts of 'baby bonds' and investors would be paid back before shareholders but after secured debts in a liquidation scenario. One of the key risks to investing in notes is rising interest rates which is why PRY has come off its recent highs, but I believe with a price near its issue value of $25.00 there is less downside as rates begin to rise.

Profit

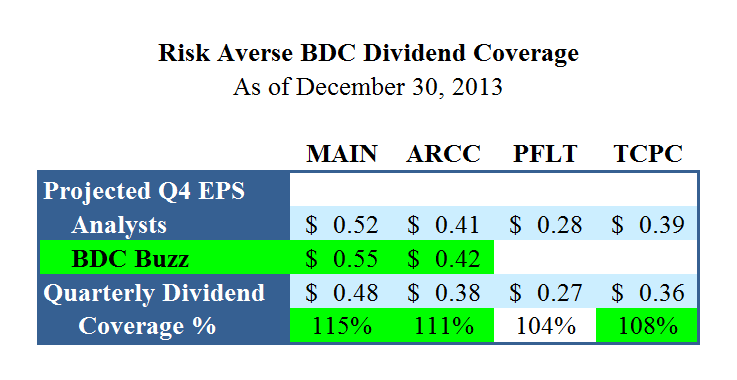

When evaluating BDCs, it is important to understand if the dividends are sustainable, ideally through net investment income ("NII") and special dividends covered by spillover taxable income or realized capital gains. As discussed earlier, the BDCs with less risk often have lower yielding investments and leverage. However I believe these companies have a good balance of both and will be able to not only cover dividends but grow them in the near future. Both MAIN and PFLT have excellent histories of increasing dividends almost every quarter. The table below shows projected EPS and the current dividend for the calendar Q4 2013 for each BDC, with my personal projections for MAIN and ARCC as discussed in "MAIN: The Best BDC?" and "ARCC: December 2013 Report".

(click to enlarge)

Later this week I will be reviewing the latest TCPC offering and the impacts to its projected earnings and net asset value ("NAV") per share to determine the potential for dividend growth and updated pricing.

Risk

In a series of articles, I took an in-depth look at the relative risk levels of each BDC. Specifically, I looked at portfolio credit quality, investment asset classes, diversification, non-accrual rates, portfolio yield, leverage, interest rate sensitivity, volatility ratios, market capitalization, insider ownership and trends, institutional ownership and trends, and management/operational history for each BDC. The following table shows the most recent relative risk ranking with a weighted average rank of 8.5 for the this portfolio (a rank of 10 implies the least amount of risk). As discussed earlier I chose not to include SUNS and FSC due to dividend coverage issues and GBDC because of pricing and lack of dividend growth.

Payout

Obviously, this portfolio has lower than average dividend yield at 7.5% but both MAIN and PFLT have continually increased regular dividends. ARCC, TCPC and MAIN all pay special dividends and I consider this to be a prudent manner of distributing income to shareholders. Some BDCs rely on onetime income or capital gains to cover regular dividends but have a history of cutting dividends which has a direct impact on share prices as investors start to sell. These are usually the higher yield and higher risk BDCs.

Valuation

Ideally, each BDC would be priced along a valuation curve with investors paying a premium for favorable risk-to-reward ratios. Below is a table using my relative risk ranking to categorize each BDC into valuation levels and appropriate multiples of NAV, LTM EPS and 2013 EPS, but does not include the NAV multiple for American Capital (ACAS) due to it being an outlier in many respects:

(click to enlarge)

As you can see, I consider the BDCs in this portfolio in a category that deserves higher multiples with MAIN having the highest, but with much higher than average NAV per share growth.

Summary

This is a solid portfolio for investors that want a low maintenance BDC portfolio with lower yields compared to the other BDC portfolios but higher than the average equity investment. The tax treatment of the distributions for this portfolio is more favorable than other BDCs but changes every year. In my weekly newsletter I track the performance of the 25 BDCs that I follow that are currently trending higher as seen in the chart below:

(click to enlarge)

Investors should only use this information as a starting point for due diligence. See the following for more information:

Disclosure: I am long MAIN, TCPC, ARCC, FDUS, TCRD, PSEC, NMFC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire