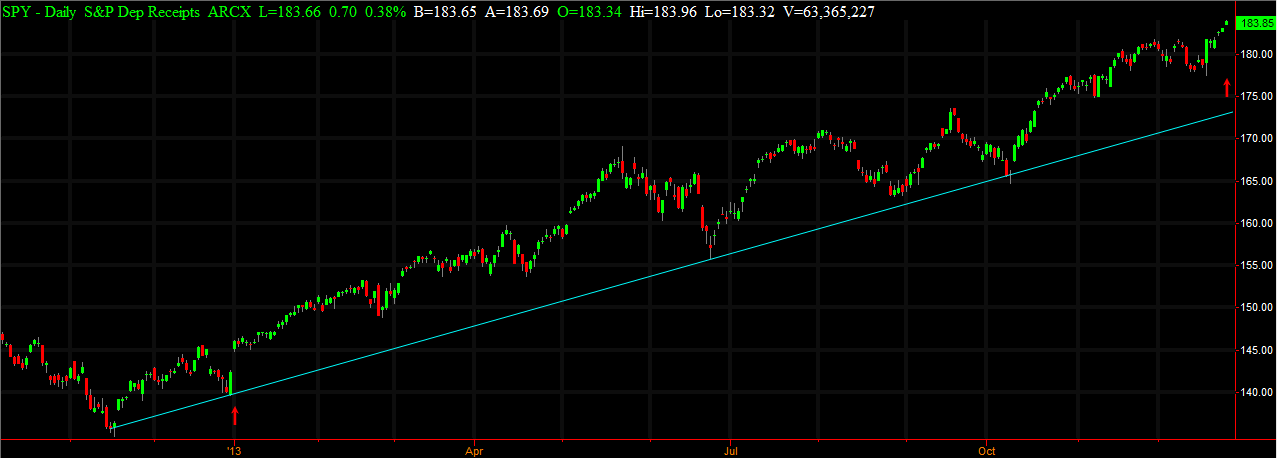

As of now, the U.S. is the world's fastest-growing 'emerging' market - S&P Depository Receipts (SPY) have increased by 22.3% since January 1, 2013 and S&P futures have increased by 26.5% over the same timeframe. Unemployment has steadily decreased from 8% to 7%. The Fed has been feeding banks $80 billion per month for a year (not for free, but by buying bonds, mind you), and has kept the real interest rate at 0%, allowing the lowest rate loans in the history of interest rates and steadily increasing US bank reserves, thus increasing the stability of the credit and loan industry. The Fed has also committed to keep interest rates low for the forseeable future.

(click to enlarge)

The only possible barrier on the horizon is inflation. Oddly enough, we need inflation in order to facilitate investment. If inflation falls below 0%, it is cheaper for businesses to just hold money and watch it appreciate in value. It's a form of investment in itself. The PCE, or Personal Consumption Expenditures index (the Fed's preferred measurement of inflation), is currently at 1.1%. Despite the Fed's decision to "taper" quantitative easing on December 18th, it was only a $5 billion taper (out of $80 billion), and it was partially in response to the positive jobs report. The Fed is playing it smart this year. That means they will still pump $75 billion into banks' reserves, thus continuing to increase the feasibility of large business loans, which help drive market growth. The deadly combination of improving jobs data paired with a renewed commitment to increase banks' reserves and maintain low interest rates only drives the market one direction: up.

The last time rampant deflation occurred was during the Great Depression, to the tune of a negative 10% rate. Banks and individuals decided to hold onto money because its value increased by 10% each year the rate remained the same - it was safer than investing, and a 10% deflation return manages to outpace annualized 8% returns on the stock market. Stocks plummeted, not only because of decreased investment, but decreased purchases of all goods and services. If the price went down 10% in a year, there was no reason to buy an item unless it was immediately essential.

Luckily, the Fed has prevented this from happening after the crash of 2007/2008 by keeping loan rates extremely low. Recently, the central bank has turned to quantitative easing (similar to printing money at a calculated rate in order to buy U.S. bonds from banks), pumping $80 billion into the market every month of 2013. According to basic supply and demand theory, the more money in circulation, the lower the buying power of the dollar, and the higher the PCE. Despite mid-year dollar value increases, the dollar has fallen to within .2% of its value at the beginning of the year. This is especially significant because an increasing market typically increases the value of the connected currency. However the PCE has fallen from 1.6% in January to 1.1% in November. Similarly, the Consumer Price Index (CPI, another measure of inflation - see here for the differences between the two) has decreased from 1.9% to 1.7%.

The question of what will happen to the dollar and PCE now that the Fed is decreasing its anti-deflation investments to $75 billion per month remains unanswered, but the fact that it is still pumping money into the market should keep the dollar, at a minimum, in check. I see deflation as the only potential barrier to a roaring market in 2014, and it is currently not a tangible issue. The market has gone up for six days in a row, and if it increases to seven days, that would be technical trend confirmation to the upside. A similar movement happened in March 2013, 2,000 points lower than the level the Dow Jones Industrials (DIA) are trading at right now.

I believe now is a good time to increase your investments to the long side during market pullbacks, such as the one we saw in early December. Re-evaluate your positions when you hear the jobs report on Friday, January 10th, and the CPI report on Friday, January 16th. These will influence the Fed's decision on further tapering, which it announces after its meeting on January 28-29th. Fed decisions have been the greatest single influence on long-term market outlook for 12 months now. The PCE is announced on January 31st.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire