I find it highly unlikely that DISH Network (DISH) will be able to thwart Sprint's buyout of T-Mobile (TMUS) as Sprint (S) is far more heavily capitalized than DISH Network. DISH Network knows that its TV channel and internet subscription business is stagnating, so it's hoping to generate significant EPS growth through a takeover of T-Mobile.

The real concern that I have for a rumored DISH Network buyout of T-Mobile is that it would literally be stringing along two weak companies into an even weaker competitor. While it's true that the Department of Justice would have an easier time approving a DISH Network and T-Mobile merger, it would not improve the competitive landscape of the telecom industry whatsoever. I will try to illustrate this throughout the course of this article.

Dish Network Has No Equity

Dish Network only has $701 million in shareholder equity, and somehow they're going to pull off a $25-$30 billion acquisition of T-Mobile? This would only further worsen its financial position, and quite frankly it's too high a risk.

Source: Ycharts

The company has a similar amount of assets and liabilities meaning that in basic accounting lingo there's hardly any owner's equity. This implies that if DISH Network were to bother raising capital it begs me to wonder where it will come from, and at what interest rate. The company doesn't produce a whole lot of income from its operations, and was only able to replenish the cash on the balance sheet from a $4.3 billion debt issuance in fiscal year 2012. Going into 2013, the company issued an additional $7.4 billion in long-term debt, but reduced the debt with debt repayment of $5.2 billion after it was outbid by SoftBank for Sprint.

Currently, Dish Network has around $10.3 billion in cash and cash equivalents, but that's nowhere near enough to buy out T-Mobile. However, to make the deal work, DISH Network could technically attempt both a partial stock swap in order to retain enough cash on the balance sheet to avoid an abnormally high debt to asset ratio. Even so, that would mean that Dish Network would attempt to issue $15 to $20 billion in shares through a share swap. It could attempt to borrow an additional $10 billion in order to appease T-Mobile shareholders with a larger sum of cash, but following the buyout, the amount of cash on the balance sheet would be exceptionally low relative to total liabilities. Therefore, Dish Network's buyout of T-Mobile from purely a financial standpoint would heavily impair its long-term financial stability and would probably result in the company getting a severe junk bond rating from major credit rating agencies.

After a downgrade interest costs will go up. With a higher cost of interest, how in the heck will DISH Network pull off a 4G LTE Network build out? Oh yeah, it won't, it just blew through a ton of cash to buy out T-Mobile. Give it enough years and DISH Network will have to write down the value of its intangibles resulting in a humongous loss of shareholder equity, because it attempted to invest into a business it shouldn't have. This is because cell towers exhibit accelerated depreciation, plus the value of T-Mobile shares would most likely fall following a DISH Network acquisition, resulting in goodwill impairment. I don't think any Chief Financial Officer would attempt such an M&A, and any T-Mobile shareholder that approves a bid from DISH Network is in my opinion foolish.

SoftBank/Sprint credit profile and interest arbitrage

By now, I'm pretty sure you're well aware of the fact that I prefer a Sprint and T-Mobile merger. I have dedicated a whole entire article to this point, and believe that it's going to be accretive to Sprint, while a short-term catalyst for T-Mobile (read my previous article for further background information). I make this assessment, because SoftBank has far more flexibility with financing as it has a stronger balance sheet.

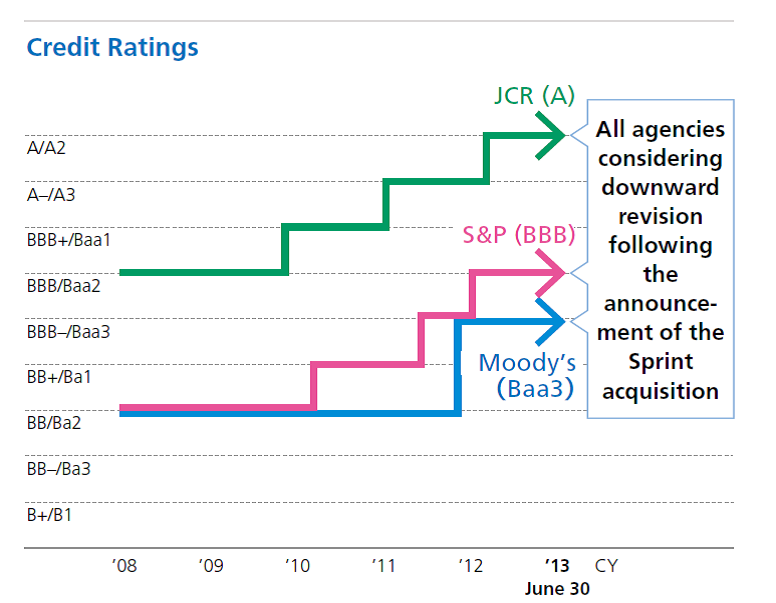

(click to enlarge)

Source: SoftBank

The above graphic illustrates the credit rating of SoftBank leading up to its acquisition of Sprint (I provide the above graphic to help illustrate the rating changes). Following the buyout, S&P issued a downgrade on debt from BBB to BB+ (two notches down). Moody's also instituted a downgrade on SoftBank's credit rating from Baa3 to Ba1 (one notch down). Some would consider this to be a junk bond rating, but there are plenty of investment banks willing to double down on these type of investment securities if the risk to reward is reasonable.

In this specific instance we're dealing with a telecom, which isn't bad. I've seen junk bonds trade on movie rental companies like Blockbuster and Movie Gallery for pennies on the dollar (interest rates were around 18% to 25%). I guess the current bond holders in SoftBank are agitated as the market value of pre-existing bond notes have probably gone down, but at least they'll still collect reasonable interest rates at maturity based on the below graphic.

(click to enlarge)

Source: SoftBank

Currently SoftBank's credit rating is reasonable enough to pursue another LBO. I presented a table of how much it pays on interest, but based on the data it looks like cost of interest will be around 6% to 8% for the long-term. Given the foreign exchange currency effects and inflation risk, now would be the most practical time to borrow money.

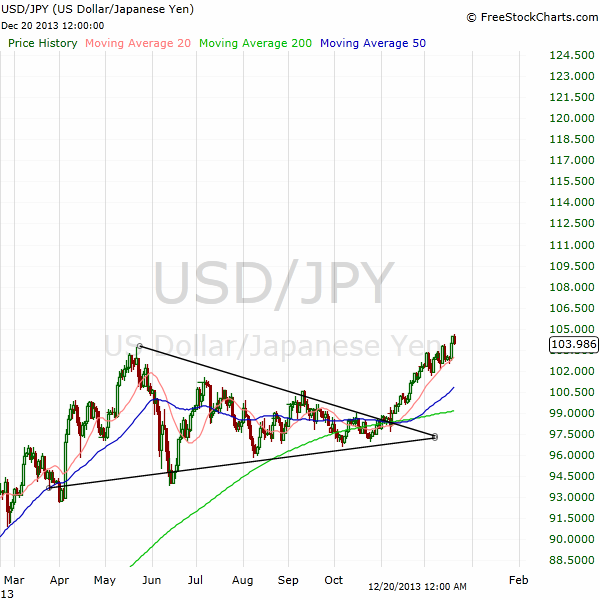

(click to enlarge)

Source: FreeStockCharts

Currently, the USD/JPY currency pair is in a very clear up-trend. I make this important point, because it means that the Japanese Yen is devaluing against the US Dollar, because the Japanese central bank is stepping up its bond buying program whereas the Federal Reserve has initiated a taper. The effect is that Japanese interest rates should go up in an environment of currency devaluation. If the cost of interest is expected to go up, companies will generally borrow money in order to avoid the cost of issuing interest bearing notes at an even higher interest rate.

However, the macro environment could be beneficial to SoftBank. If it borrows currency in Yen and uses the currency to buy out T-Mobile, while injecting a significant amount of cash into its CAPEX, T-Mobile's strategy will further scale. Further out into the future, Sprint and T-Mobile will most likely consolidate, therefore generating enough cash efficiencies to generate significantly more profit (this is even after higher CAPEX). This would imply that Sprint and T-Mobile could return the cash from operations back to SoftBank (the parent company). By the time Sprint returns cash to its parent company, the value of the dollar would have substantially appreciated in relation to the Japanese Yen. Assuming that is the case, we could imagine SoftBank paying down debt at a 6%-8% interest rate with dollars that have appreciated anywhere from 10-30% over the next five years. If that's the case, SoftBank may end up paying zero cost on interest, due to interest rate arbitrage. Global finance is sort of neat, especially if you're in the right position to take advantage of it.

Let's examine the balance sheet a little more.

(click to enlarge)

Source: SoftBank

Currently SoftBank has $35.6 billion in interest bearing debt (using current FX rates), for both the short-term and long-term. This is only assuming the interest bearing debt, and excludes all other liabilities. SoftBank has $13.83 billion in short-term cash and equivalents. SoftBank has $22 billion in shareholder equity. When considering SoftBank already has $13.83 billion in dry powder, plus an addition $22 billion in equity to borrow against, the company is sufficiently well positioned to borrow cash and initiate a buyout of T-Mobile. SoftBank can implement a stock swap in order to reduce the amount of burden the financial transaction will have against the balance sheet, and instead use the dry powder on CAPEX.

In the event SoftBank pulls off a buyout of T-Mobile, the goodwill account on the balance sheet would increase, liabilities would increase, and the cash balance would decrease. This would result in owner's equity remaining the same, but would result in another credit downgrade. The debt to asset ratio will increase, but short-term solvency shouldn't be too significant of a problem. SoftBank would have to rely more heavily on cash flow for network build-out. Therefore CAPEX would drop, but that's okay as the CAPEX from its Japanese segment should be winding down as the network build out in Japan is nearing completion.

When combining the net income from SoftBank's ($2.5 billion) and T-Mobile's most recent quarterly report (-$36 million), the company has around $2.47 billion in income to cover interest expenses per quarter. Normally, most would want to use Free Cash Flow, but because depreciation is a cost that has to be built into the assumption (cell towers rapidly depreciate), I would much rather use net income as a way to measure how much cash is available to pay for financing. This is because rapid depreciation might as well be treated as a current expense.

A $20 billion loan would cost $1.6 billion in annual interest (8% interest rate) expense, and would be expensed quarterly for around $400 million. This would mean that after paying interest, SoftBank would still have $2 billion in net income to work with. A LBO would have less of a negative impact on the financial statement of SoftBank than it would for DISH Network.

Conclusion

While both companies would have to use a bit of creativity to take T-Mobile private, I lean in favor of SoftBank. The cost of interest can be better absorbed with Sprint buying out T-Mobile as cost efficiencies alone should be able to cover the quarterly interest expense at an 8% interest rate. The interest rate arbitrage from currencies would result in SoftBank buying out T-Mobile for an even lower cost of interest. Following that, SoftBank has enough shareholder equity, plus dry capital to successful execute a buyout at a $30 billion market cap (this is a value that's 50% higher than where rumors of a buyout began). However, if it has to, it can also use a share swap to better manage cash flow. As it stands, the burden of interest could be covered by operations with very minimal impact to CAPEX, but when the balloon on the long-term note pops (maturity), the company would need to accumulate cash, which may cut into future CAPEX. However, this impact should be absorbed by SoftBank reducing network build out in Japan, while it continues network build out in North America. This way it can lower CAPEX without hurting its long-term business strategy.

Once a formal announcement has been made, investor presentations will soon be released detailing the full benefits of a buyout from the competing parties (DISH Network and Sprint/SoftBank). In this specific case, I'm already heavily certain, but not 100% certain SoftBank will win. However, once a formal announcement has been made I will provide an update on how I feel about the LBO between the two counterparties, and I will make an even more conclusive argument. Thank you for reading.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire