With yet another dividend cut, American Capital Agency (AGNC) actually did something surprising. The stock didn't hit new lows, and in fact it ended higher two days later. As a fundamental investor, over time the learning curve has led to more focus on how stocks handle bad news. The fascinating situation with American Capital Agency has been the extreme weakness of the stock over the last year. With the drop from over $35 to below $20, the recent trading suggests the dividend cuts might finally be built into the stock.

American Capital Agency is a mortgage real estate investment trust, or mREIT, that focuses on investing in a levered portfolio of agency backed mortgage securities.

With the mREITs sector plunging, most investors appear to suggest a collapse will occur at any interest rate increases. Recent history plus the aggressive buybacks of the company provide solid conclusions of an investment that might provide considerable value trading below the $25.27 net asset value (NAV), as of Sept. 30.

Rising Interest Rates

While rising interest rates typically provide a headwind for the mREITs including American Capital Agency, this isn't always the case. Back in 2009, the stock rose in price while interest rates were rising.

As the above five-year chart highlights, the stock moved in higher correlation with the dividends, than it did the volatile interest rates. The dividends also highlight that the direction of the rates aren't as significant as the ability to predict the direction. The ability to hedge positions and adjust leverage has a significant impact on the ability of the mREITs to generate income for dividend payouts.

Though the Fed has started the process of tapering the bond purchases including MBS, the ZIRP policy should remain intact for years. In this scenario, it is very possible that the 10-Year Treasury will remain at or below 3% for 2014. Remember that both Germany and Japan have 10-Year rates significantly below the current US rate. No guarantee exists that the 10-Year will rise any further especially until the Fed raises the Fed funds rate.

Huge Buybacks

American Capital Agency has made huge buybacks at below NAV over the last year. For investors selling the stock, it brings up an interesting dichotomy. The managers are experts in the field of MBSs and inherently know the risk of rising interest rates, yet they see the stock as extremely undervalued. Knowing all the risks and the crucifying this stock will receive if these buybacks are fundamentally flawed, it should make investors take notice. The company technically is buying MBSs below market value by purchasing the stock below the NAV. This move provides shareholders more value over directly buying an MBS.

During Q313, American Capital bought approximately 28.2 million shares, or an astonishing 7% of the company's outstanding shares. The average purchase price of $20.82 costs around $586 million. In total, the company has spent around $934 million to repurchase 43.0 million shares. With a market cap of $7.7 billion, American Capital has repurchased roughly 12% of the current market value. Remember, this is in addition to paying a dividend that still yields over 13%.

Growth Potential

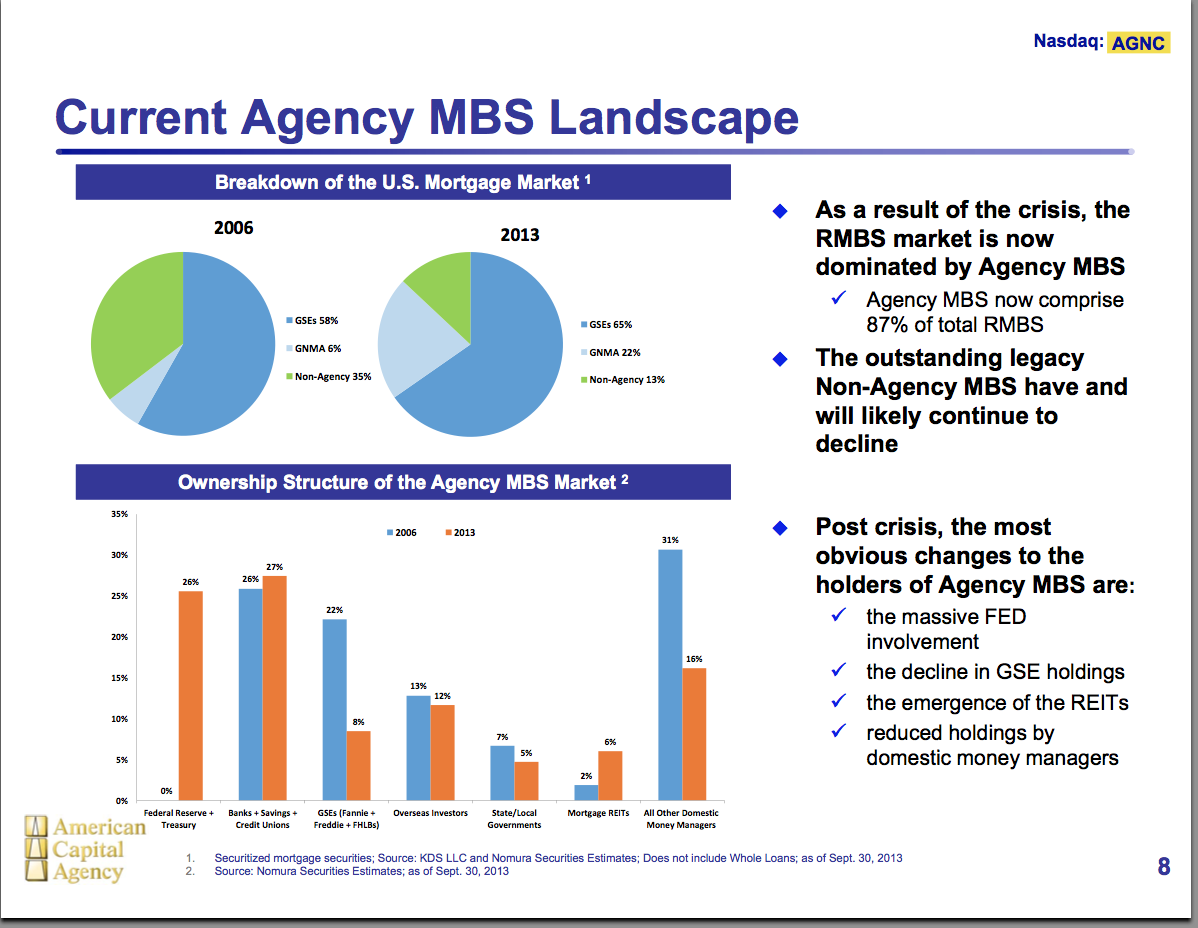

Outside of the short-term issues with rising interest rates, the mREIT sector should benefit from a fundamental shift in the MBS market over the next couple of years. The Fed tapering will provide a void in the market that already lacks private capital. Firms such as American Capital Agency hope to fill the void for the Fed that will over time reduce the ownership position that now accounts for 26% of the market. All of the mREITs combined only account for roughly 6% of the market. See the slide below:

(click to enlarge)

Substantial changes are likely to occur once the Fed completely leaves the MBS market, but for now it is only reducing the monthly purchases from $85 billion to $75 billion worth of mortgages. It does leave a slight void in the monthly purchases, but it does eliminate a competitor that absent will allow American Capital to purchase securities at more attractive prices.

Conclusion

While the market is smart to fear a sharp rise in long-term interest rates due to Fed tapering, a move might not hurt American Capital Agency as much as feared. The wider yield curve would actually allow American Capital to leverage up the portfolio to increase core earnings going forward.

The recent trading action suggests that the bad news might be in the market for now. It isn't an all clear signal for investors, but a good start to building stability to provide an entry point in the near future.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in AGNC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire