In a recent article, I present a favorable outlook on NXP Semiconductors (NXPI) that primarily draws upon a story in The Wall Street Journal; and Credit Suisse's and Sterne, Agee & Leach's rating of the stock. There are additional things to potentially like about the company, such as its efforts to do business in China, a place where, broadly speaking, American tech firms have been faced with obstacles.

A December 2nd story in Financial Times goes into detail about NXP's joint venture with the state-owned Datang Telecom (SSE: 600198) in the Chinese automobile market. Per a Press Release, it is "The first true automotive semiconductor company in China." NXP is focusing on research and marketing, and the newspaper remarks that intellectual property theft there creates a "Competitive environment." It also says that

Unlike carmakers, which have to enter China with a local partner, component companies are free to operate alone. NXP has partnered up anyway, giving Datang a 51 per cent controlling stake. This arrangement will enable the venture to take advantage of tax benefits, subsidies available to Chinese entities and preferential access to local carmakers, many of which are owned by the government.

The reasons cited are all sensible.

Additionally, the agreement also seems to help obviate explicit difficulties that a list of domestic firms, including Cisco Systems, Inc. (CSCO), Starbucks Corporation (SBUX), and Qualcomm Inc. (QCOM) are having in The People's Republic. Other businesses such as International Business Machines (IBM) and Hewlett-Packard (HPQ) are enduring sluggish results there; though problems with regulators that the others incur are not specified as reasons for IBM or HPQ troubles.

NXP currently has an 11% share of the Chinese market for semiconductors, according to Financial Times. Per its March 1st Form 20-F, the company has ownership of facilities in Jinlin, Guangdong; and also Hong Kong where closure is foreseen in 2013.

In a December 18th company Report, Sterne Agee reiterates a Buy rating and assigns a $50 price target. Specific reasoning involves NXP's partnership with China Unicom Pay ("CUP"), "The only domestic bankcard organization in China operating under approval of the People's Bank of China," for EMV cards.

We believe NXPI's partnership with CUP, where it has a significant market share (70%+) potentially supplying the secure element with ~$0.25-$0.50 in content in China and the ROW, should be a multi-year secure card tailwind. In the 2013 Nilson report, CUP, a China bankcard network operating under the PBOC (Peoples' Bank of China) and at least 14 other major China banks is the largest debit-credit card supplier in the world with ~3.5B cards today growing to ~5.3B cards by 2017; and supplying to the fastest growing region, Asia-Pacific…with transactions growing 109% to 2016. Also in September 2013, NXPI noted aggressive migration by the PBOC to contact-less cards with transaction times of "less than 300ms."

NXP is also involved in Near Field Communications ("NFC") technologies, which enable contactless transactions. Security has been a consistent consideration regarding NFC and payment processing. Although the PCOB's migration to contactless cards could potentially signify another boon to the company.

One consideration is an existing overhang, or equity ownership of Private Equity ("P-E") investors who are to liquidate their shares. Just under 15% of the stock is now held by P-E firms after they unloaded 9.7% in a recent secondary offering. Similar downward pressure on the share price is nearly inevitable in the future.

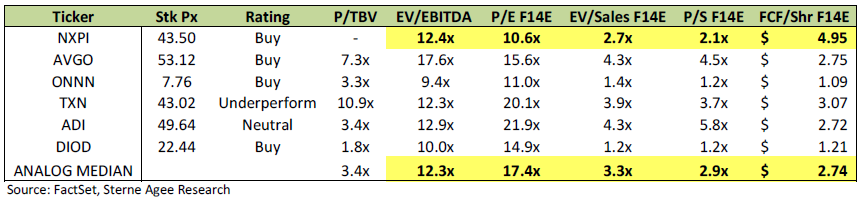

However, a table shows compelling peer valuations, as classified under analog products. Avago Technologies Limited (AVGO) is another stock that has been highly regarded and outperforming; and projections have been updated since its $6.6 billion acquisition of LSI Semiconductors (LSI). It is a considerable transaction that can result in many future possibilities.

(click to enlarge)

NXP is a foreign company with global operations and therefore has risks that should not be overlooked; however, its product line is fairly diverse and may offer value.

To summarize, Avago has just made a considerable acquisition, and some issues are being sorted out. In consideration of Chinese operations, a wait and see approach can also be sensible for Qualcomm and Cisco. However, NXP's increasing and diversified presence there appears to be well planned.

Disclosure: I am long NXPI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire