The Dow 30 is an index comprised of 30 of the best companies in the United States. The Dow index is widely quoted by all major news organizations when they refer to how Wall Street is performing. There is a tremendous amount of prestige involved in being included in the index, almost as a sign of you have made it to the top of the heap. The Dow has always been fertile ground for investment ideas for me due to the nature of its components. I tend to favor large established companies with a long track record that makes them easy to predict. The above definition tends to apply to most of the companies in the Dow 30 index.

IBM in my view should be the best performer in the Dow 30 in 2014. The article below will delve into my reasoning behind my bullishness towards IBM. The article will consist of three main reasons behind my bullish thesis with data gleamed from publicly available data released by the company itself.

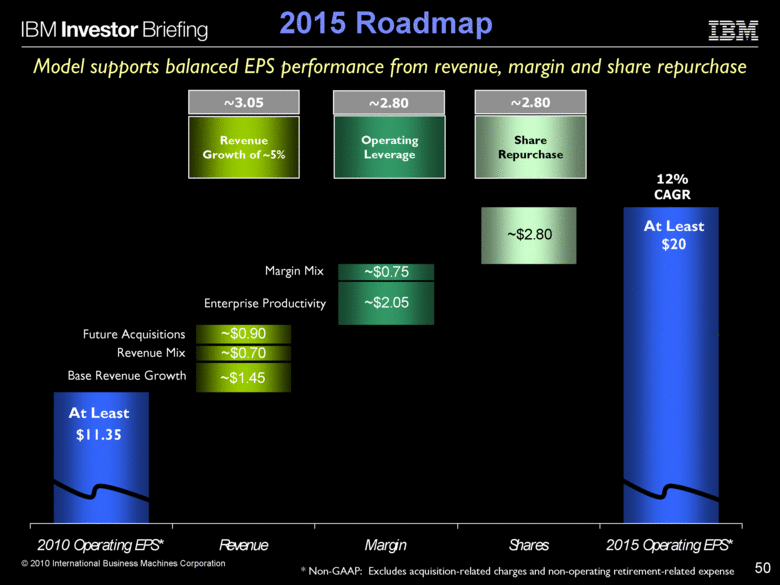

(click to enlarge) |

File taken from page 50 of the May 2010 8-K

The primary reason for my bullish stance towards IBM revolves around IBM's consistent ability to grow earnings. I would like to draw the reader's attention to the company's proclamation for earnings growth into year 2015 as shown above. Notice how IBM is projecting 12% CAGR for a mature company with a market cap of over $100 billion dollars. Let's see how IBM is progressing towards its goal. The following quote should neatly sum up IBM's path towards it 2015 roadmap, "And so with this improved operational performance, continued momentum in our growth initiatives, and the flexibility in the financial model, we are maintaining our view of at least $16.25 of operating EPS in 2013, and remain confident in our ability to achieve at least $20 in 2015."

IBM would need to continue to grow earnings at a 10.94% CAGR to achieve its $20 target in 2015 which is below the growth rate predicted in 2010. In my view the goal is very achievable which should lead to further share gains.

The secondary reason for my bullish stance towards IBM revolves around their consistent and methodical repurchasing of their common shares outstanding. When the 2015 roadmap was announced, IBM had 1,228 million shares outstanding. They have managed to pare that number down significantly with 1,101.8 million shares outstanding as of the third quarter 2013. IBM recently announced an increase in their repurchase activity raising the funds available by $15 billion. IBM has over $20 billion available to repurchase its outstanding shares. The funds available for repurchase would shrink the company's market cap by roughly 10% which would provide a significant tailwind to its earnings.

The final reason for my bullish take on IBM revolves around their ability to increase their margins. While researching this article I found the following tidbit on page 45 of its most recent 10-Q,

"Diluted earnings per share of $3.68 increased 10.5 percent versus the prior year. In the third quarter, the company repurchased10.5 million shares of its common stock."

Operating (non-GAAP) diluted earnings per share of $3.99 increased $0.37 or 10.2 percent versus the third quarter of 2012 driven by the following factors:

Revenue decrease at actual rates: | $ (0.15) | |

Margin expansion: | $ 0.35 | |

Common stock repurchases: | $ 0.17 |

The company generated $3,760 million in cash flow provided by operating activities, a decrease of $754 million compared to the third quarter of 2012, driven primarily by higher workforce rebalancing payments ($340 million), changes in sales cycle working capital ($156 million) and a decline in operational performance in the third quarter of 2013 versus 2012. Net cash used in investing activities of $2,548 million increased $1,548 million primarily due to increased spending for acquisitions ($2,041 million) and less cash received from divestitures ($339 million), partially offset by increased cash from net sales of marketable securities and other investments ($909 million). Net cash used in financing activities of $827 million decreased $1,679 million compared to the prior year, primarily due to decreased cash used for common stock repurchases ($1,068 million) and higher net cash proceeds from total debt ($791 million)."

I was impressed by IBM's ability to eke out a consistently higher margin as they continue to shift away from hardware and emphasis software. Below the chart is a discussion detailing the purchase of new companies and the increased use of debt to repurchase shares. I am heartened to see IBM's continued purchase of competitors to round out the gaps in its lineup. I don't view the increase in leverage to be problematic at this point as interest rates are extremely accommodative.

Chart courtesy of Stockta.com

With the above background in mind, what would be a fair estimate for IBM in 2014? IBM is having trouble growing its revenue which in my opinion should equate to a less than market multiple. Using operating earnings as my guide, I believe a 13 multiple on $18 in expected operating earnings is fair. This would equate to a gain of roughly 30% from current levels with dividends included. I view the shares as, at a minimum, very stable at their current quotation making the risk reward for purchasing IBM quite attractive. On a technical note, IBM recently overtook its 50 day moving average breaking out of a pronounced downturn. A further move above $190 would allow the company to cross over its 200 day moving average setting up a "bullish cross" which is generally a favorable trading pattern. I would like to thank you for reading the above article and I look forward to your comments.

Disclosure: I am long IBM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire