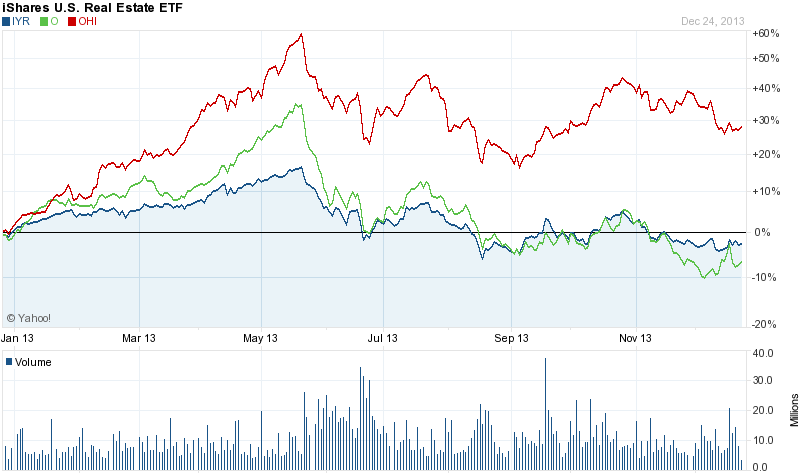

When I wrote my 2013 preview of the REIT sector, little did I know how volatile the space might become. I figured some REITs might be able to provide low double digit total return over the course of the year, thus my generally positive stance. As we all know, before June it looked like I had substantially undershot the group's potential, with commonly followed REIT indices, like VNQ and IYR trading up almost 20% in less than six months. Individual companies like Realty Income (O) and Omega Healthcare (OHI) shot up by as much as 40 and 55 percent, respectively, before the house of cards started to crumble on May 22.

Six months later, the indices have lost their robust gains and are basically flat for the year. Individual issues are mixed, with Realty Income underwater for the year, while others, like Omega having still having gained 25% in value.

(Click to enlarge)

Lesson Learned - Comparative Valuation

I think this year's REIT roller coaster ride has provided several general yet very valuable investment lessons on the importance of dissecting both valuation and growth rate as well as on being disciplined when executing buy/sell decisions. Despite their different milieus of expertise, namely skilled nursing for OHI and diversified single tenant for Realty Income, I think a comparison of their divergence over the past year is worthwhile and instructive for investors.

Entering 2013, Omega traded at roughly 11X FFO while Realty Income traded at roughly a 20 operating multiple, an 80% valuation divergence. Both companies were expected to grow FFO by about 20% in 2013, and it appears that both will perform as anticipated. After this year's split stock performance, OHI stands at about a 12 multiple and Realty Income at about 16X FFO - the divergence thus narrowed to around 30 percent.

With hindsight, clearly OHI posed the better value at the beginning of the year, and its price performance relative to O's has proven that fact. And from a pure quantitative perspective, it continues to look like the better value. But many of you may be thinking, "Wait Adam, Omega Healthcare is a much riskier REIT compared to Realty Income and should be priced at a lower multiple." While I suppose risk is in the eye of the beholder, I would tend to agree with that contention. Omega's credit rating from S&P is BB+, three notches below Realty Income's BBB+ rating. Further, its operators are dependent on medical reimbursements from the government, so its business and cash flows may be perceived as less durable than Realty Income's diversified commercial base.

Yet, even we if all agree that Omega's source of lease income is more insecure than Realty's, how much of an equity discount should we apply to the situation: 10%, 20%, how about 50 percent? Obviously that is somewhat of a rhetorical question, but it should get you thinking as to what safety, or the perception of safety, is worth in the REIT marketplace.

Looking at next year, growth will substantially slow for both. Realty Income has guided to about 6% FFO growth, while OHI analysts are pegging about 8% growth. From a value and growth perspective OHI would appear to have the advantage, but is it really the better buy?

I have learned from interacting with SA income readers that not everyone is concerned with a comparative value proposition or maximizing total return. For some, constructing the safest and most durable of income streams is the biggest investment priority. So when we consider the "best buy" amongst several REIT options, there is more than one way of considering the question and conceivably more than one possible answer.

Consequently, since there is only about a 50 basis point variance in the companies' dividend yields, I would suggest that Omega presents the better buy for total return oriented investors, while Realty Income, even at its premium valuation, presents the better buy for investors concerned with the quality and stability of an income stream and less about growth (or destruction) of capital.

Lesson Learned - Chasing Returns/Taking Profits

Price action in REITs this year certainly substantiated the old adage of "when something seems too good to be true, it usually is." When one considers a mature REIT that pays dividends in this muted real estate pricing and leasing environment, in most cases one is not buying an asset with rip-roaring underlying asset or income appreciation potential. While REIT managers may be able to bring value to the table by buying property at high cap rates, selling at low rates, and negotiating above average contractual lease step ups, REIT growth for now is somewhat predicted on the capital markets, i.e. leverage, stock issuance, and property acquisitions.

Thus, again in most cases, there shouldn't be an expectation that funds from operations (FFO) or the underlying asset base will see dramatic gains. While Realty Income grew FFO 20% in 2013, it did so largely on the basis of a large, accretive acquisition of American Realty Capital Trust (former ticker ARCT) late last year. With the benefits from that merger now vanished, the company sees FFO growth of only 6% next year, more in line with what one might expect from mature, organic REIT operations in this environment.

So when Realty's price rose from $40 to $55 a share earlier this year, well above the rate of appreciation of the average REIT, I'm not sure if it was because of a misguided belief on future growth, yield chasing, a combination of both, or some other motive, but obviously the move was irrational. While many have now gotten sucked into the game of picking a bottom on this stock, myself included, there's no way of accurately knowing when a bottom is in until after the fact.

The point of all this is that one must have keen understanding and reasonable expectations about valuation, growth potential, and income durability of the assets they are buying. While many income investors like to tell me that price drops spell opportunity for buying higher yield, I would caution that every time you watch an asset drop in price, you are in essence sacrificing yield by doing so. By recognizing overvalued assets, capitalizing on them, and reinvesting in undervalued, or more reasonably valued assets, you gain not only portfolio value but potentially increased income over the long haul. I will illustrate:

Let's say at the beginning of the year we owned 1000 shares of O worth roughly $40,000. By May, with the stock around $50, and a forward 2013 P/FFO of 21, we decide the valuation was too high and that we needed to sell off some of our position. While we don't got out totally at the top, we sell half of our stake, 500 shares at $51, a 4.27 yield point, raising $25,500. With the proceeds and the realization that the whole REIT space is running rampant, we look elsewhere to replace the yield with a more attractively valued stock. We come up with ConocoPhillips (COP), selling for $62 a share, a P/E of 11, and yield of 4.25 percent.

So we execute a stock swap and buy 411 shares of COP with our $20,500. The below table summarizes the situation after the sale:

| Stock | shares | Price 6/2013 | Capital | Yield | Annual Income |

| O | 500 | $51 | $25,500 | 4.27% | $1090 |

| COP | 411 | $62 | $25,482 | 4.25% | $1083 |

| Totals | $50,982 | 4.26% | $2173 |

The next table summarizes the situation as of 12/26, assuming we executed no transactions following the initial swap:

| Stock | shares | Price 12/26 | Capital | Yield | Annual Income |

| O | 500 | $38.13 | $19,065 | 5.73% | $1092 |

| COP | 411 | $70.21 | $28,856 | 3.93% | $1134 |

| Totals | $47921 | 4.65% | $2226 |

And the final table shows what would have happened had we not executed the swap, and instead held on to O.

| Stock | shares | Price 12/26 | Capital | Yield | Income |

| O | 1000 | $38.13 | $38,130 | 5.73% | $2184 |

Our income remains unchanged, yet we "saved" over 20%, almost $10,000, of our capital by making the move to swap out of a clearly expensive stock and rotate into one priced at a lower level. Capital that we could potentially again reallocate at a higher yield, perhaps back into O at a 5.73% yield. While most swaps won't necessarily be as successful as the one above, one can get an idea of how a focus on value can be a boon to one's bottom line and income stream.

FRT - Final Exam

Two articles (I,II), one by Tim McAleenan and another by Brad Thomas have taken up whether Federal Realty Trust (FRT), a REIT specializing in shopping centers should be sold. If we look at the quantitative situation, this is a company selling at an FFO multiple of better than 20, yielding a paltry 3.1%, and growing at a mid- to maybe upper-single-digit clip. The valuation seems reminiscent of Realty Income's quantitative vitals earlier in the year. While I'm all about owning quality assets, I'm not about owning quality assets at any price.

Brad sees FRT as a rock star in the REIT universe, and I would concede that the company has a fine property portfolio and a vision for the future. However, this is one performance I'm not going to pay the price to attend, additionally, if I owned FRT, I'd minimally trim my position and move on to greener, cheaper, and/or higher yielding pastures. I wouldn't want to watch another overpriced REIT, rock star or not, just like Realty Income, take my capital when it reverts to a more reasonable valuation mean.

Lesson learned.

Disclaimer: The above should not be considered or construed as individualized or specific investment advice. Do your own research and consult a professional, if necessary, before making investment decisions.

Disclosure: I am long COP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire