Ever since the May 9, 2012 announcement by Hilltop Holdings (HTH) that it was acquiring PlainsCapital Corporation, investors were eagerly counting down the days towards when the deal would close last year. Hilltop Holdings' share price jumped by nearly 23% on May 9 when Hilltop and PlainsCapital announced the deal announced and it increased by another 133% on top of that increase over the following 19 months. Although PlainsCapital was a private company, it still filed public financial reports with the SEC. That works out well for investors because they can see how PlainsCapital has performed. I can see that the market was very excited about this deal as HTH's 133% total return since the announcement on May 9 before the market opened greatly exceeded the 38% total return of the SPDR Financials ETF (XLF) during this period.

Source: Hilltop Holdings Q3 2013 10-Q

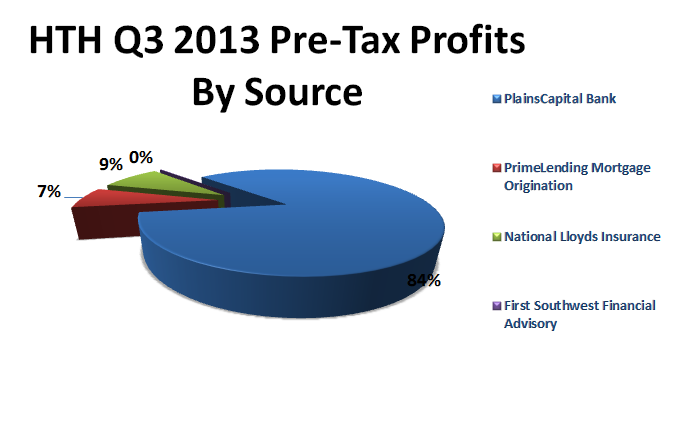

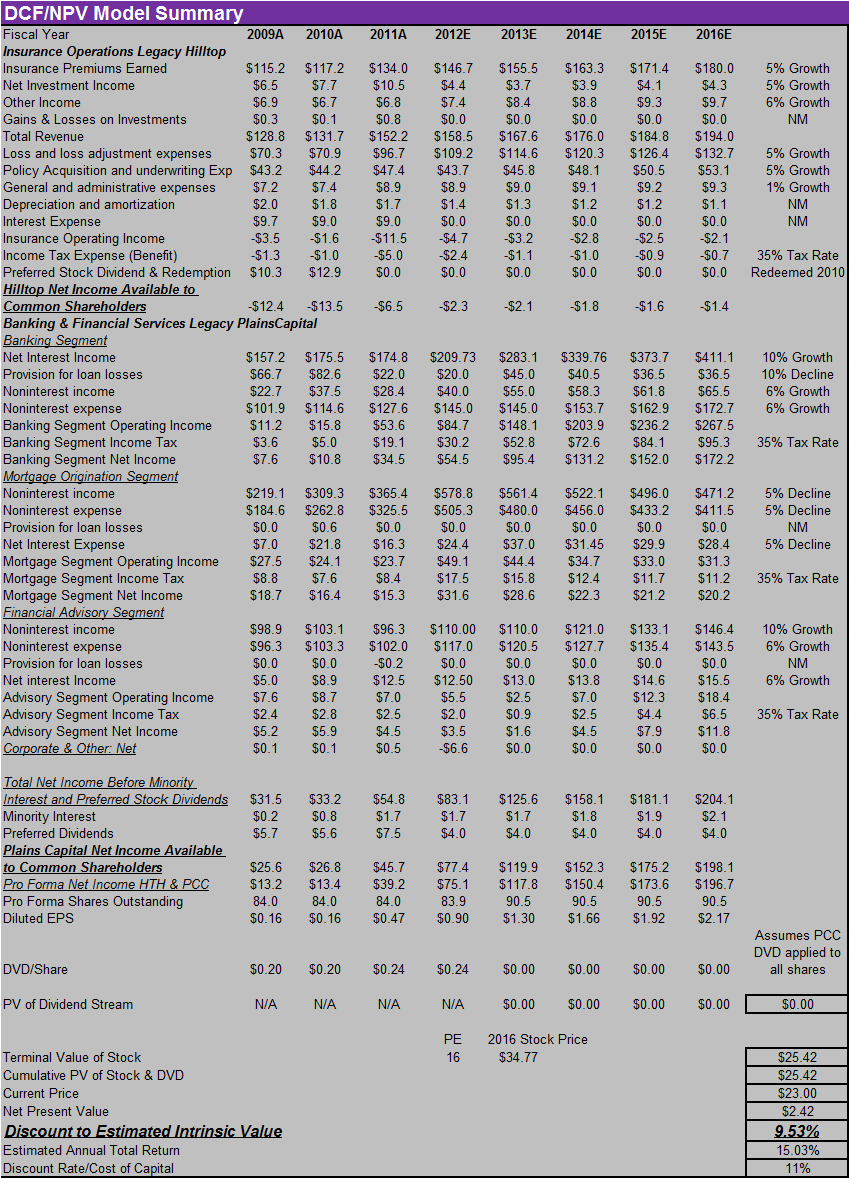

Hilltop Holdings' Key Business Segments:

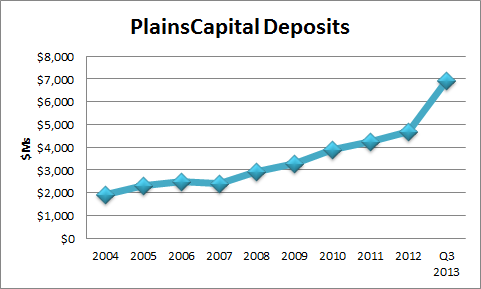

Hilltop Holdings' Banking Segment includes the operations of PlainsCapital Bank, which offers a variety of personal and business banking products and services. PlainsCapital Bank was a legacy subsidiary of PlainsCapital Corporation before its acquisition by Hilltop Holdings.

PlainsCapital Bank enjoyed solid deposit and revenue growth from 2009 to 2012 and improving credit trends helped it generate strong pre-tax profit growth during this period. In 2013, PlainsCapital Bank had strong revenue growth and positive operating leverage enabled it to generate 60%+ pre-tax profit growth year-over-year in Q3 2013 and YTD 2013. PlainsCapital Bank generated an efficiency ratio of 41.04% for Q3 2013 and 40.32% for YTD 2013. I believe that this is a combination of good expense management and the fact that this only includes the impact of the PlainsCapital Bank operations whereas the efficiency ratios of many other mid-cap and large-cap banks include the impact of high expense to revenue businesses such as investment banking, investment management and mortgage lending. As of Q3 2013, PlainsCapital Bank exceeded all regulatory capital requirements with a total capital to risk weighted assets ratio of 13.36%, Tier 1 capital to risk weighted assets ratio of 12.76% and a Tier 1 capital to average assets, or leverage, ratio of 11.05%. PlainsCapital Bank generated a Net Interest Margin of 5.16% in YTD 2013 and Hilltop Holdings generated a consolidated corporate-wide net interest margin of 4.38% during this period.

Sources: PlainsCapital's 2009-11 Annual Reports , Hilltop 2012 Annual Report and Morningstar Direct

Near the end of Q3 2013, Hilltop announced that PlainsCapital Bank acquired substantially all of the liabilities, including all of the deposits, and acquired substantially all of the assets of Edinburg, Texas-based First National Bank from the Federal Deposit Insurance Corporation and reopened acquired branches of FNB under the PlainsCapital Bank brand name. FNB had $2.6B in assets and $2.4B in deposits however, that bank's loan portfolio suffered from numerous non-performing loans. According to independent banking analyst Kenneth Thomas, FNB had $267M in non-performing loans as of the end of Q2 2013 and its Tier 1 leverage ratio was 1.96%. I agree with the FDIC's determination that FNB was significantly undercapitalized and it is no wonder why banking-tracking firm SNL Financial LLC added First National to its list of undercapitalized banks in June. When PlainsCapital took over FNB in September, it had to markdown the value of FNB's loan book by $337.6M. I guess that is why the FDIC gave Hilltop/PlainsCapital $45M as an initial cash payment, which is subject to future adjustment and settlement.

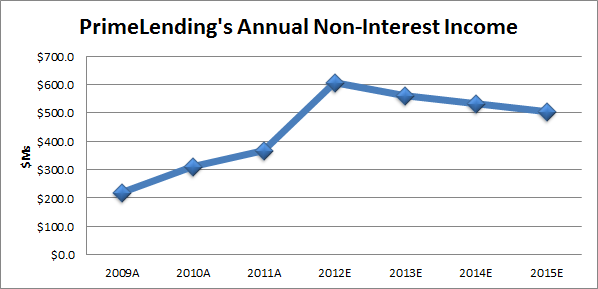

Hilltop Holdings' Mortgage Origination Segment includes the operations of PrimeLending, which offers a variety of loan products from offices in 42 states and generates revenue predominantly from fees charged on the origination of loans and from selling these loans in the secondary market. PrimeLending was a legacy subsidiary of PlainsCapital Corporation before its acquisition by Hilltop Holdings.

PrimeLending enjoyed explosive revenue and profit growth from 2009 to 2012 but its revenue plateaued in 2013. Q3 2013 non-interest revenue declined by 29.5% year-over-year and YTD 2013 revenue declined by 30bp year-over-year. Non-interest revenue declined due to declines in home mortgage originations as well as gains on the sales of loans and origination fees. Although its non-interest expenses declined by 19% in Q3 2013 versus Q3 2012, its expenses increased by 4.7% in YTD 2013 versus YTD 2012 due to severance payments associated with the layoffs of 10% of its non-origination staff. PrimeLending's pre-tax profits declined by 42.35% year-over-year in YTD 2013 versus the YTD 2012 period. With interest rates expected to rise further, I believe that PrimeLending's revenues will decline by at least 5% annually over the next couple of years. Although PrimeLending accounts for the largest share of Hilltop's revenues, it has low margins due to the incentive-based commission compensation structure for its origination employees. PrimeLending initiated additional headcount reductions in Q4 2013 and is engaging in other operating cost reduction initiatives to stabilize its profits because that the mortgage market has peaked. I expect to see PrimeLending begin realizing the benefits of these measures during Q4 2013.

Sources: PlainsCapital's 2009-11 Annual Reports , Hilltop 2012 Annual Report and My Estimates

Hilltop Holdings' Insurance Segment is composed of National Lloyds Corporation, formerly known as NLASCO, Inc. National Lloyds provides fire and homeowners insurance to low value dwellings and manufactured homes primarily in Texas and other areas of the southern United States. National Lloyds Company was a legacy subsidiary of Hilltop Holdings before Hilltop acquired PlainsCapital Corporation.

National Lloyds generated steady year-over-year revenue growth of 6.1% in Q3 2013 and 6.4% in YTD 2013. Pre-tax income was $4.3M during the quarter compared with a pre-tax loss of $6M in Q3 2012. The segment's improved results in Q3 2013 and YTD 2013 versus the prior year's comparable periods were due to the incremental revenue growth and reduced losses and loss adjustment expenses year-over-year. NLC's direct written premiums increased by 8.8% year-over-year in Q3 2013 versus Q3 2012 and 5.9% in YTD 2013 versus YTD 2012. Revenue growth in its core homeowners, fire and mobile home markets more than offset the non-renewal of a commercial product line. Two of the three Q2 2013 storms NLC endured have exceeded its $8M reinsurance retention so its reinsurers will assume any additional losses incurred by NLC.

Sources: Hilltop 2011-12 Annual Reports and My Estimates

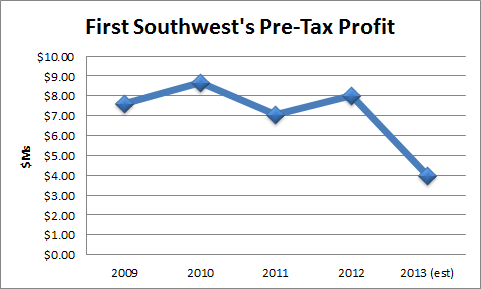

Hilltop Holdings' Financial Advisory Segment generates a majority of its revenues from fees and commissions earned from investment advisory and securities brokerage services at First Southwest Company. First Southwest was a legacy subsidiary of PlainsCapital Corporation before its acquisition by Hilltop Holdings.

First Southwest's revenue was flat year-over-year in Q3 2013 and YTD 2013 versus the prior year's comparable periods. First Southwest was not the only brokerage firm that faced headwinds from the soft fixed income trading markets. Hilltop owns equity warrants representing 17% of SWS Group's outstanding shares and it faced the same issues that First Southwest faced regarding reduced sales of fixed income securities to institutional customers. First Southwest's pre-tax profits declined by $2M year-over-year in Q3 2013 versus Q3 2012 and $3M year-over-year in YTD 2013 versus YTD 2012 due to higher non-interest expenses in general and employee compensation expenses in particular.

Although this is Hilltop's smallest segment, it is disappointing to see pedestrian performance from this business since I expected more out of First Southwest due to the high margin investment banking, brokerage and advisory operations of this business. PlainsCapital sold its 60% controlling ownership in Hester Capital Management for its book value in July 2012. If Hilltop can't find a way to generate significant growth in its First Southwest financial advisory business, it should either acquire a similarly sized regional brokerage competitor (like SWS Group) and merge the two organizations together in order to enjoy economies of scale or sell First Southwest to a larger competitor.

Sources: PlainsCapital's 2009-11 Annual Reports , Hilltop 2012 Annual Report and My Estimates

Hilltop Holdings' Investment in SWS Group:

Hilltop invested $50M in a loan and equity warrant in SWS Group (SWS) in 2011, which is the parent of Dallas area brokerage firm Southwest Securities. Hilltop led a $100M strategic investment in SWS in order to help it shore up its capital due to losses. Hilltop and Oak Hill each lent SWS $50M at 8% for 5 years and received 8.7M SWS share warrants that it can exercise at $5.75/share. Regardless of how SWS's share price performs, I am not expecting Hilltop to exercise the warrants until it sees demonstrated improvements in SWS's revenue trends.

Source: Hilltop's Q3 2013 10-Q Report and SWS Group's Q1 2014 10-Q Report

Regulatory Developments:

On Tuesday December 10, the Federal Reserve and Federal Deposit Insurance Corporation both voted unanimously to adopt the Volcker Rule, which would bar banks from proprietary trading and limit their ability to invest in hedge funds and private equity funds. In July, the Federal Reserve approved a final rule that will substantially amend the risk-based capital rules applicable to Hilltop and the Bank. The final rule implements the "Basel III" regulatory capital reforms and changes required by the Dodd-Frank Act. The final rule includes new minimum risk-based capital and leverage ratios, which will be effective for Hilltop and PlainsCapital Bank on January 1, 2015, and refines the definition of what constitutes "capital" for purposes of calculating these ratios. Hilltop has $177M in unrestricted cash and cash equivalents as of Q3 2013 that it can uses to acquire other banks or return to shareholders.

The new minimum capital requirements will be: (I) a new common equity Tier 1 capital ratio of 4.5%; (ii) a Tier 1 to risk-based assets capital ratio of 6% (increased from 4%); (III) a total capital ratio of 8% (unchanged from current rules); and (iv) a Tier 1 leverage ratio of 4%. The final rule also establishes a "capital conservation buffer" of 2.5% above the new regulatory minimum capital ratios and will result in the following minimum ratios: a common equity Tier 1 capital ratio of 7.0%; (ii) a Tier 1 to risk-based assets capital ratio of 8.5%; and a total capital ratio of 10.5%. The new capital conservation buffer requirement would be phased in beginning in January 2016 at 0.625% of risk-weighted assets and would increase each year until fully implemented in January 2019. PlainsCapital Bank's Tier 1 capital to average assets is 11.05%, its Tier 1 capital to risk-weighted assets is 12.76%, its total capital to risk-weighted assets is 13.36% and this exceeds the new standards.

In addition, the Federal Reserve Board published an interim final rule in September 2013 that clarifies how companies should incorporate the Basel III regulatory capital reforms into their capital and business projections during the next cycle of capital plan submissions and stress tests. For companies and their subsidiary banks with between $10.0B and $50.0B in total consolidated assets, the initial capital planning and stress testing cycle began on October 1, 2013 and continues through the fourth quarter of 2015, which overlaps with the implementation of the Basel III capital reforms beginning on January 1, 2015. At September 30, 2013, Hilltop and PlainsCapital Bank had approximately $9.1B and $8.6B, respectively, in total consolidated assets. Accordingly, Hilltop and the Bank are not subject to this capital planning and stress testing cycle. If PlainsCapital Bank grows to have more than $10.0B in assets through additional acquisitions or organic growth, it may become subject to future capital planning and stress testing cycles, which would likely increase its cost of regulatory compliance.

Large Shareholders

Gerald J Ford is the sole general partner of Diamond A Financial, LP and Diamond A Financial owns 15M shares of Hilltop Holdings, which it has held since 2008. This represented nearly 27% of Hilltop's shares before its acquisition of PlainsCapital and 18% of its shares after the deal closed. Other notable shareholders include the following firms:

- Burgundy Asset Management (4.74M shares, 5.64% of Hilltop)

- Ranger Investment Management (1.84M shares, 2.2% of Hilltop)

- Royce & Associates (795K shares, 0.95% of Hilltop)

- Bandera Partners (788K shares, 0.94% of Hilltop)

- Highfields Capital Management (624K shares, 0.74% of Hilltop)

- Hodges Capital Management (455K shares, 0.54% of Hilltop)

Risks to Hilltop Holdings include the following:

- Increased severity of weather-related events impacting its insurance division

- Continued weakness in the fixed income and mortgage markets impacts its First Southwest investment banking division and its PrimeLending mortgage unit

- Economic weakness resulting in loan loss headwinds

In conclusion, I was pleased with the pro forma performance of PlainsCapital during the first nine months that Hilltop Holdings. I was encouraged that Hilltop chose to acquire PlainsCapital last year because PlainsCapital continues to show strong growth and operational improvements. Investors were waiting a long time for Gerald and Jeremy Ford to execute a strategic deal. I thought that the SWS Loan and Warrant package in 2011 was a good start towards putting its cash pile to work. I am also looking to see if the Ford Family will use the rest of Hilltop's excess cash in adding another bank or financial services company. Finally, I believe that if the National Lloyds insurance business continues to generate underwriting losses, I believe that the Ford Family should be more proactive in improving it or selling it to another firm who can manage it better.

VALUATION ANALYSIS

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

This entry passed through the Full-Text RSS service — if this is your content and you're reading it on someone else's site, please read the FAQ at fivefilters.org/content-only/faq.php#publishers.

Aucun commentaire:

Enregistrer un commentaire